Miniso delivers its strongest performance in history, why did the stock price drop more than 10%? | Insight Research

國內直營佔比未見起色、自研 IP 存在感進一步削弱、海外拓店速度不及預期……都為這個小商品帝國的未來增長路徑蒙上一層不確定性的陰影。

11 月 21 日,名創優品交出截至2023 年 9 月 30 日止的 FY2024Q1 季度財報。堪稱史上最強業績,營收、毛利率、淨利潤等多項數據均取得歷史性的突破。

披露期營收37.91 億/yoy+36.7%。其中海外收入 12.95 億元/yoy+40.8%,國內收入 24.96 億元/yoy+34.7%。海外收入增速超過國內。

毛利率首次突破40%,達 41.8%/+6.1pct;經調整淨利潤 6.4 億/+54%,經調整淨利潤率為 16.9%/+2pct。

這份財報可總結為“3 高 2 快”:毛利高(41.8%)、單店收入高(月營業收入21.1 萬);拓店速度快(全球門店數量突破6000 家),上新快(7 天推出 100 個新品),週轉快(67 天左右完成一次週轉)。

各運營指標的積極表現,標誌着名創優品在運營效率、市場響應速度、創新能力方面都達到了歷史性高度的黃金階段。

然而,業績公佈次日,公司股價卻出現下跌。

在亮眼的財報數據背後,隱藏着市場對增速的擔憂。

國內直營佔比未見起色、自研IP 存在感進一步削弱、海外拓店速度不及預期......都為這個小商品帝國的未來增長路徑蒙上一層不確定性的陰影。

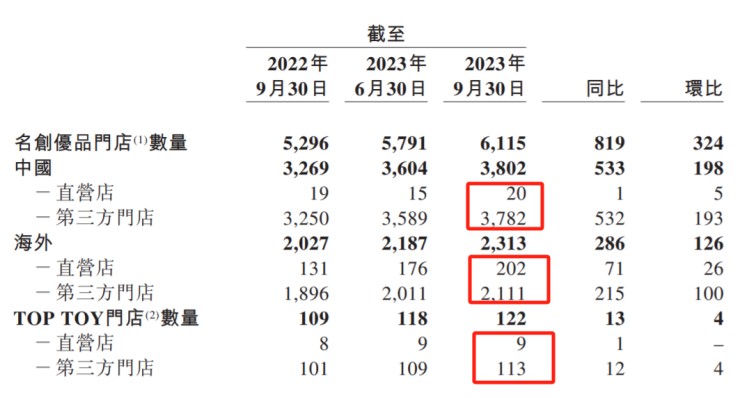

全球門店數量突破 6000 家,直營僅 231 家

跑通一個單店模型,然後快速複製,這就是零售店增長的根本模式。名創優品正處在這個快速複製、飛速成長的階段。

財報期內期間內,名創優品門店數繼續狂飆。國內門店數3802 家,淨增 533 家,環比淨增 198 家,提前一個季度完成全年國內淨增長 350 到 450 家門店的目標,並實現全球門店數量突破6000 家這一重要里程碑。

在名創優品全球6000 多家門店中,只有 231 家門店是直營店,其餘均採用第三方代理模式。

直營模式的佔比過低是名創優品一直以來被詬病的。

(資料來源:名創優品FY24Q1 季報)

雖然代理模式可以有效地將運營風險轉移給代理商,減輕公司自身的管理負擔,但這種策略也意味着必須與代理商共享利潤,從而導致單個門店的利潤率低於直營模式。

因此,許多零售品牌會在重點市場選擇直營模式以保持品牌質量的一致性和控制產品標準,而在追求快速擴張的市場採用代理模式。

名創優品雖然也對外宣稱重視直營市場,將其視為重要的增長驅動力,但最新季度報告中顯示,代理模式仍佔據壓倒性的地位。

根據Q3 的數據,名創優品在國內的直營門店數量為 20 家,相比去年同期僅增加了 5 家,而與此同時,第三方門店的數量增加了 193 家。

如何在維持品牌質量和提升利潤率的同時,實現快速且可持續的市場擴張,仍是其未來發展的關鍵。這也需要名創優品在直營和代理模式之間找到一個更加平衡的組合。

拓店速度、單店收入齊升,名創優品正處於黃金髮展期

令人驚喜的是,名創優品在拓店速度如此之快的情況下,平均單店收入仍實現了同比23.8% 的增長,也帶動了其中國線下門店總收入的同比增長 41.2%。

在電話會中,名創優品詳細闡述了其實現同店持續增長的關鍵因素:

一個是名創優品始終強調的“開大店”。雖然大店的投入是普通門店的2 倍左右,但由於客單價高,人流量大,單店店銷反而更好。

今年以來,名創優品在全球範圍內的多個“超級大店” 如紐約時代廣場旗艦店、廣州北京路旗艦店、贛州城市形象店都獲得了亮眼的業績表現。

在本季度,名創優品繼續擴大其“超級大店” 的網絡,西安大唐不夜城店、武漢楚河漢界萬達店等新開的超級門店對公司整體業績產生了積極的拉動。

嚐到甜頭的名創優品還計劃將 “超級大店” 開到意大利羅馬、法國巴黎、西班牙馬德里等國際大城市。

此外,大美妝、大IP、大玩具等興趣消費也一直是名創優品的重點投入。這類品類的毛利率在60% 左右,溢價空間大,是提升整體毛利的關鍵。

例如,本季度名創優品與芭比、Loopy 等品牌的聯名款產品熱銷出圈,成為業績增長的重要驅動力。在國內銷售額破千萬的產品中,60% 左右來自於興趣消費。

然而,值得關注的是,儘管聯名IP 在短期內對品牌銷量和盈利有顯著提升作用,但 “過分依賴外部 IP” 這一標籤也一直伴隨着名創優品。

公司也意識到了這一點,多次強調將自研IP 視作重要戰略方向。但從本季度數據來看,名創優品自研IP 品牌銷售額佔比在進一步下降。

這也需要名創優品引起更高的警示,要真正打造一個具有持久吸引力的“超級品牌”,名創優品必須要有自己的 “loopy”。

費用方面,隨着名創優品品牌升級、大型門店的開設、廣告開支的增加,以及IP 庫擴大和 IP 產品種類的豐富化,相關的授權費用增加,本季度銷售及分銷開支為人民幣 640.9 百萬元( 87.8百萬美元),同比增長68.1%。

根據公司的財務預測,下一季度銷售費用預計將繼續呈上升趨勢。

隨着名創優品收入規模的擴張,固定成本不變,額外的銷售額將產生更高的利潤率。經營槓桿的釋放對沖費用上升的風險,整體的增長還是可控的。

海外市場有喜有憂

出海是名創優品的另一個故事,也是市場看重的方向。

今年泡泡瑪特、名創優品在中概股中優異的表現,共性便是國貨出海邏輯。產品出海意味着企業目標客羣將新增海外市場,天花板大大提升,在新市場上實現市佔率增長的可能性更加明確。

海外市場也為本季度財報提供了不少亮點。海外業務收入近13 億,在去年同期的高基數之上,同比增長近41%,刷新海外業務三季度銷售的最高歷史記錄。

主要海外市場仍保持GMV高速增長,北美區域同比增長近1.6倍,拉美市場同比增長近60%,歐洲市場同比增長近50%。

特別值得注意的是,名創優品海外直營市場的收入同比增長接近89%,在海外總收入中的佔比從去年同期的34% 上升至約 46%。

這是一個積極的跡象,並且名創優品還表示,“明年最大的機會就是海外直營市場。”

但在拓店速度上,海外市場似乎難以與國內市場相比。

上半年名創優品在海外開店緩慢,儘管在第三季度加快了開店速度,淨增加了126 個門店,但截至 2023 年 9 月 30 日,海外市場的累計淨增門店數為 198 家,這與年初設定的 350 至 450 家的開店目標相比,僅完成了大約一半的任務。要在一個季度內完成剩餘目標難度不小。

在歷史上,許多零售企業在經歷了快速擴張階段(如大規模開設新門店)之後,當期業績好看,但常常面臨新店鋪人流量下滑的問題,造成盈利拖累。市場或許也在擔憂名創優品也遭遇類似情況,高增長難以持續。

儘管名創優品立下豪言明年將在海外市場開出更多門店,但在下行週期下公司的擴張速度與質量如何,也仍是未知數。