Samsung Electronics issues profit warning, chip stocks under pressure, S&P falls, NVIDIA hits new all-time high, Bitcoin surges and then plunges after ETF drama

标普和道指止步两连阳,纳指收盘微涨、勉强三连阳;特斯拉跌超 2%,领跌蓝筹科技股;芯片股指盘中跌超 1% 后微幅收涨,英伟达收涨 1.7%,盘中曾跌超 1%。中概股指跌超 1%、四连跌,达达跌超 6%,京东跌超 2%。十年期美债收益率重上 4.0%,但盘中转降,继续脱离三周高位。美元指数反弹;离岸人民币盘中跌超 200 点失守 7.18,创近四周新低。比特币盘中上冲 4.79 万美元刷新 21 个月高位,后迅速跳水超 2000 美元。原油反弹,美油一度涨超 3%;美国天然气大涨 7% 创近七个月最大涨幅,六连涨至近两月高位。伦铜八连跌,和黄金均收创近四周新低。更新中

美股失去连日反弹的主要动力科技股支持,主要股指全线低开。

三星电子拉响盈利警报,初步指引预计四季度连续第六个季度营业利润下滑、且超预期同比剧减 35%,市场对三星内存芯片业务持续复苏的期望受创。周一大涨的芯片股指勉强收涨,英伟达股价连日创历史新高,但盘中曾转跌。波音继续拖累道指。在多家航司发现更多波音飞机部件松动后,负责航空安全的美国官员称,对波音飞机的调查范围可能扩大到 737 Max 9 以外机型。

欧债发行量创单日最高纪录之际,周一反弹的欧债国债价格回落。而盘中公布结果显示美国三年期美债标售稳健,助推美债收益率下行。站上 4.0% 的基准十年期美债收益率盘中转降、一度下测 4.0% 关口。有评论称,市场对美联储降息的激进定价与美国经济基本面有韧性之间的不匹配日益加剧,降低了联储宽松的必要性,可能导致全球市场出现股债齐跌的 “反向金发姑娘” 行情。

汇市方面,美元指数有所反弹,但还未逼近上周五所创的三周高位;多种非美货币回落,离岸人民币继上周五之后再度盘中失守 7.18,跌至近四周来低位。周一在比特币现货 ETF 获批乐观情绪推动下大涨的比特币因一则乌龙消息盘中巨震。美国证监会 SEC 在社交媒体发帖宣布比特币 ETF,后又澄清并未批准,是黑客攻击其账号后 “假传圣旨”,比特币先上冲 4.79 万美元,后迅速跳水超过 2000 美元。

大宗商品中,中东危机和利比亚供应受干扰共同助推周一大跌的国际原油反弹,美油一度涨超 3%。巴以冲突外溢风险增加,据央视报道,以色列军方称,黎巴嫩真主党的无人机周二袭击以军北方司令部总部,以北部多个地区当天遭来自黎巴嫩的导弹袭击;以色列媒体称,以军开始向北部地区部分 “待命” 人员发放武器装备。有分析提到,利比亚最大油田 Sharara 最近关闭影响产量约 30 万桶/日,是供应面的又一利好原油因素。此外,一些大型航运公司仍在避开红海水域,德国企业 Hapag-Lloyd 周二称,旗下货船将继续绕道好望角。

而美国天然气进入 2024 年以来保持涨势,周二大涨逾 7%、更胜原油一筹。评论称,最近气价持续走高主要源于,气象预报显示未来两周寒流将席卷美国中部的大部地区,气温低于往年同期正常水平可能大力支持气价上行,因为家庭和企业的取暖需求更强劲。

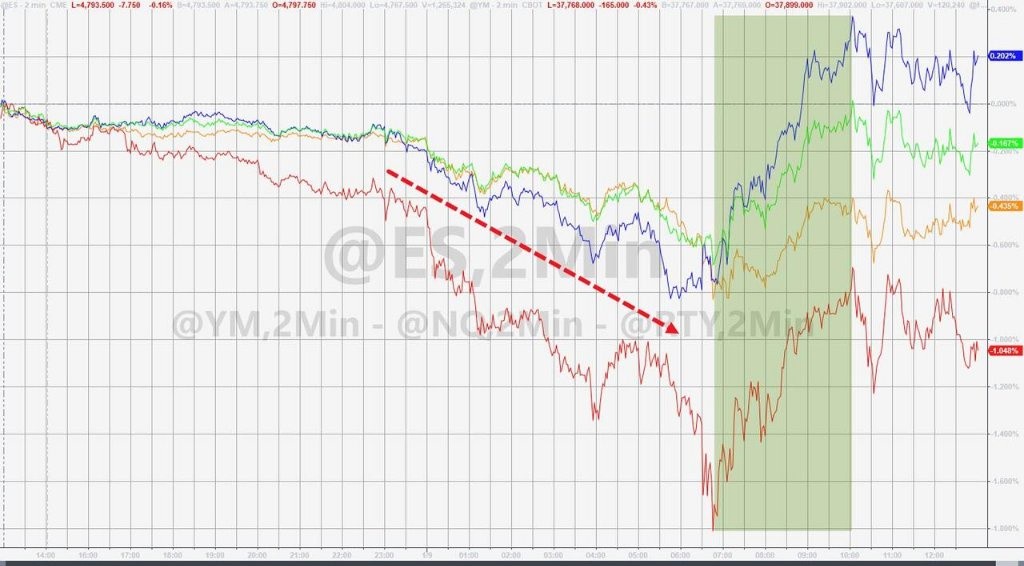

标普道指止步两连阳 特斯拉领跌蓝筹科技股 英伟达曾转跌并跌超 1% 中概股指四连跌

三大美国股指集体低开,早盘齐跌,此后表现不一。道琼斯工业平均指数全天保持跌势,早盘刷新日低时日内跌近 310 点、跌逾 0.8%,标普 500 指数早盘刷新日低时跌约 0.7%,午盘曾短线转跌。纳斯达克综合指数早盘刷新日低时跌近 0.9%,早盘尾声时转涨,午盘不止一次转跌。

最终,道指和标普在连续两个交易日收涨后回落,纳指勉强保住涨势。纳指收涨 0.09%,报 14857.71 点,涨幅远不及周一,周一纳指收涨 2.2%,和标普均创 2023 年 11 月 14 日以来最大涨幅。周一收涨 1.41% 的标普收跌 0.15%,报 4756.5 点。周一涨近 217 点创 12 月 21 日以来最大涨幅的道指收跌 157.85 点,跌幅 0.42%,报 37525.16 点。

价值股为主的小盘股指罗素 2000 收跌 1.05%,周一刚走出连跌六日刷新的 12 月 13 日以来收盘低位,就回落。科技股为重的纳斯达克 100 指数收涨 0.17%,连涨三日,三日刷新的 12 月 29 日以来收盘高位。衡量纳斯达克 100 指数中科技业成份股表现的纳斯达克科技市值加权指数(NDXTMC)收涨 0.6%,连涨三个交易日,但涨幅远不及收涨 2.9% 的周一。

标普 500 各大板块中,周二只有四个未收跌。英伟达所在的 IT 涨近 0.3%,必需消费品涨逾 0.2%,通信服务涨逾 0.1%,医疗微涨。能源收跌逾 1.6%,连续两日领跌,材料也跌超 1%,其他板块跌不足 0.8%。

道指成分股中,唯一能源股雪佛龙收跌 2.5% 领跌,迪士尼也跌逾 2%,面临飞机调查范围扩大后,周一大跌 8% 的波音(BA)早盘曾跌逾 2.5%,后跌幅收窄,收跌约 1%。

龙头科技股盘初曾齐跌,后部分转涨。其中特斯拉表现最差,尽管 Model Y 成为全球最畅销车型,特斯拉股价早盘仍低开低走,一度跌超 3%,收跌约 2.3%,回吐周一止住六连跌的所有涨幅、回落至 11 月 13 日以来收盘低位。

FAANMG 六大科技股中,周一涨超 2% 的苹果早盘曾跌超 1%,收跌逾 0.2%,在周一告别连跌五日刷新的 11 月 6 日以来收盘低位后回落;连涨三日至 2021 年 9 月以来高位的 Facebook 母公司 Meta 收跌逾 0.3%;被花旗因市场对其期望值高及面临一系列风险而下调评级至中性后,周一反弹至 12 月 29 日以来高位的奈飞早盘曾跌超 2%,收跌 0.6%;而对 OpenAI 130 亿美元投资面临欧盟调查的微软早盘曾跌近 1%,收涨近 0.3%,连涨两日、继续刷新 12 月 29 日以来高位;谷歌母公司 Alphabet 盘初转涨,收涨 1.5%,连涨两日至 12 月 26 日以来高位;亚马逊也收涨 1.5%,连涨三日至 12 月 29 日以来高位。

芯片股总体险些未能连涨三日,周一大涨超 3% 的费城半导体指数和半导体行业 ETF SOXX 盘初曾跌超 1%,收盘涨不足 0.1%,两日刷新 12 月 29 日以来收盘高位。个股中,英伟达开盘后很快转跌,曾跌超 1%,早盘转涨后,午盘曾涨至 543.25 美元,日内涨约 4%,收涨 1.7%,报 531.4 美元,连续两日创盘中和收盘历史新高;到收盘,AMD 涨超 2%;而美光科技跌 1.9%,Arm 跌超 1%,英特尔跌 0.8%。

AI 概念股总体回落。到收盘,C3.ai(AI)跌近 1%,早盘 SoundHound.ai(SOUN)跌近 11%,BigBear.ai(BBAI)跌近 7%,Palantir(PLTR)跌超 1%,而 Adobe(ADBE)涨近 1%。

热门中概股总体继续下挫。纳斯达克金龙中国指数(HXC)收跌近 1.4%,连跌四日,刷新 5 月 31 日以来收盘低位。中概 ETF KWEB 和 CQQQ 分别收跌近 1.5% 和约 2%。三家造车新势力继续齐跌,早盘理想汽车跌超 3%,蔚来汽车跌 4% 后跌幅收窄到 3% 以内,小鹏汽车曾跌 1.8%。其他个股中,到收盘,周一暴跌近 46% 的达达跌超 6%,斗鱼跌超 4%,京东、腾讯粉单、B 站跌超 2%,阿里巴巴、百度跌超 1%,网易跌 0.7%,而拼多多早盘转涨后收涨约 2%。

波动较大的个股中,被美国银行将评级从中性降至低配、认为美国国内航空公司前景严峻、且 Geared TurboFan 发动机的问题可能抑制 2024 年公司增长后,捷蓝航空(JBLU)收跌 10.2%;宣布将裁员约 25% 的视频游戏软件开发商 Unity Software(U)收跌约 8%;被 Evercore ISI 将目标价下调 32%、担心四季度业绩将令投资者失望、且华尔街对其 2024 年增长约 15% 的预期太乐观后,锂矿公司美国雅宝(ALB)盘初曾跌 4%,收跌 2.1%。

而媒体称 Elliott Investment Management 持股该司约 10 亿美元后,经营 Tinder 等约会平台的 Match Group(MTCH)盘初曾涨近 12%,收涨 3%;媒体称其接近被惠普分拆的惠与科技收购、交易额约 130 亿美元后,网络通讯设备公司 Juniper Network(JNPR)收涨 21.8%,惠与科技(HPE)收跌 8.9%;被摩根士丹利上调评级至超配、看好其新推出的 AI 平台等产品周期后,网络安全公司 CrowdStrike(CRWD)收涨 4.8%。

欧股方面,欧债收益率回升施压,周一反弹的泛欧股指回落。周二公布的欧元区 11 月失业率意外下行至 6.4%,创历史新低,评论称,低失业率料将不会改变今年内欧洲央行降息的道路,但一系列全球喜忧参半的数据会促使市场降低未来降息的预期。

欧洲斯托克 600 指数又开始靠近上周三刷新的 12 月 13 日以来收盘低位。主要欧洲国家股指齐跌,周一反弹的德法英西股以及连涨三个交易日的意大利股指均回落。

各板块中,矿业股所在的基础资源收跌近 1.4% 领跌,银行跌近 0.9%,而医疗逆市收涨近 0.7%,连涨两日。个股中,被对冲基金 Gotham City Research 质疑其财会造假后,尽管否认,西班牙药企 Grifols 仍重挫 25.9%。

美元指数反弹 比特币盘中上冲 4.79 万美元 后迅速跳水超 2000 美元

追踪美元兑欧元等六种主要货币一篮子汇价的 ICE 美元指数(DXY)在亚市早盘曾接近 102.10 刷新日低,日内跌约 0.1%,欧股盘前转涨后未再转跌,美股早盘曾涨破 102.60,日内涨超 0.4%,尚未逼近上周五触及 103.10 刷新的 12 月 13 日以来盘中高位。

到周二美股收盘时,美元指数处于 102.50 上方,日内涨 0.3%,在周一回落后反弹;追踪美元兑其他十种货币汇率的彭博美元现货指数涨逾 0.3%,在两日回落后反弹至 12 月 20 日以来同时段高位。

非美货币中,周一止住四连阴的日元未能保住反弹势头,盘中转跌,美元兑日元在美股早盘转涨,午盘曾涨破 144.60,日内涨近 0.3%,开始靠近上周五上逼 146.00 刷新的三周高位;欧元兑美元在美股盘中曾下逼 1.0910 刷新日低,日内跌超 0.3%,还未逼近上周五跌破 1.0880 刷新的三周低位;英镑兑美元在美股盘中曾下测 1.2670 刷新日低,跌近 0.5%,未再逼近上周五涨破 1.2770 刷新的一周高位。

离岸人民币(CNH)兑美元在亚市早盘短线转涨时刷新日高至 7.1601,转跌后持续下行,美股午盘曾跌至 7.1881,刷新上周五失守 7.18 后所创的 12 月 13 日以来低位,日内跌 254 点。北京时间 1 月 10 日 5 点 59 分,离岸人民币兑美元报 7.1842 元,较周一纽约尾盘跌 215 点,在周一收平后重回跌势。

美股尾盘传出美国 SEC 批准现货 ETF 的消息后,比特币(BTC)迅速拉升至 4.78 万美元上方,部分平台涨破 4.79 万美元,连续两日刷新 21 个月来盘中高位,后随着 SEC 澄清消息系黑客攻击其社交媒体账号后发帖所致、并未批准 ETF,币价跳水,一度下测 4.51 万美元、较日高回落超过 2700 美元、跌超 5%,后重上 2.57 万美元,最近 24 小时跌超 2%。

欧洲国债收益率回升 十年期美债收益率重上 4.0% 但盘中转降

欧洲国债价格总体回落,收益率重回升势。到债市尾盘,英国 10 年期基准国债收益率收报 2.78%,日内升约 1 个基点,盘中曾接近 3.84%,靠近上周五升破 3.85% 刷新的三周高位;2 年期英债收益率收报 4.19%,大致持平周一同时段水平;基准 10 年期德国国债收益率收报 2.18%,日内升约 5 个基点,盘中曾升至 2.20%,2 年期德债收益率收报 2.59%,日内升约 5 个基点,盘中曾接近 2.63%,均逼近上周五美国就业报告发布后刷新的三周来高位。

美国 10 年期基准国债收益率在欧股盘中曾升破 4.05% 刷新日高,日内升约 2 个基点,美股盘前起持续回落,美股早盘曾短线下破 4.0% 刷新日低,日内降近 4 个基点,继续脱离上周五非农就业报告后上逼 4.10% 刷新的三周来盘中高位,到债市尾盘时约为 4.01%,日内降约 2 个基点,在连升两日后连降两日。

对利率前景更敏感的 2 年期美债收益率在美股盘前曾上测 4.40% 刷新日高,日内升近 2 个基点,美股盘初曾下破 4.35%,日内降约 2 个基点,到债市尾盘时约为 4.36%,日内降约 1 个基点,在连升四日后连降两日。

原油反弹 美国天然气创近七个月最大涨幅及近两月新高

周一大跌的国际原油期货周二总体保持涨势,仅在亚市早盘和欧股盘前曾转跌。美股盘前刷新日高时,美国 WTI 原油逼近 73 美元,日内涨 3.05%,布伦特原油接近 78.20 美元,日内涨 2.7%。

最终,原油虽然收涨,但未抹平周一所有跌幅,还未逼近上周五反弹所创的一周多来收盘高位。周一跌近 4.12% 创 11 月 16 日以来最大收盘跌幅的 WTI 2 月原油期货收涨将近 2.08%,报 72.24 美元/桶。周一收跌 3.35% 创 12 月 12 日以来最大跌幅的布伦特 3 月原油期货收涨 1.93%,报 77.59 美元/桶。

美国汽油和天然气期货齐涨。连跌三日的 NYMEX 2 月汽油期货收涨 2.42%,报 2.0768 美元/加仑,告别周一刷新的 12 月 13 日以来低位;NYMEX 2 月天然气期货收涨近 7.05%,创 2023 年 6 月中以来最大日涨幅,报 3.1900 美元/百万英热单位,刷新 11 月 15 日以来收盘高位,连涨六个交易日。

伦铜八连跌 和黄金均收创近四周新低

伦敦基本金属期货周二多数继续下跌。伦铜连续八个交易日收跌,创近四周新低。伦锡跌超 1%,连跌四日至近五周低位。伦锌、伦铅和伦镍连跌两日,伦锌继续创三周多来新低,伦铅和伦镍逼近各自上周四所创的三周来和 2021 年 4 月以来低位。而伦铝反弹,告别连跌五日所创的三周多来低位。

纽约黄金期货反弹失利,在周二美股盘前曾刷新日高至 2048.6 美元,日内涨超 0.7%,此后回落,美股早盘曾短线转跌,午盘再度转跌。

最终,COMEX 2 月黄金期货收跌 0.5 美元,跌幅 0.02%,报 2033 美元,连续两日,刷新 12 月 13 日以来收盘低位,在上周五大致收平后连跌两日。

现货黄金在美股盘前曾接近 2042 美元刷新日高,日内涨近 0.7%,美股盘中曾靠近 2026 美元短线转跌,美股收盘时处于 2028 美元上方,日内微涨。