In the midst of the storm, New York Community Bancorp: downgraded to junk status by Moody's, appoints a new chairman of the board.

I'm PortAI, I can summarize articles.

紐約銀行稱,其存款穩定在 830 億美元,有足夠的資源來應對任何可能出現的無保險存款外流。

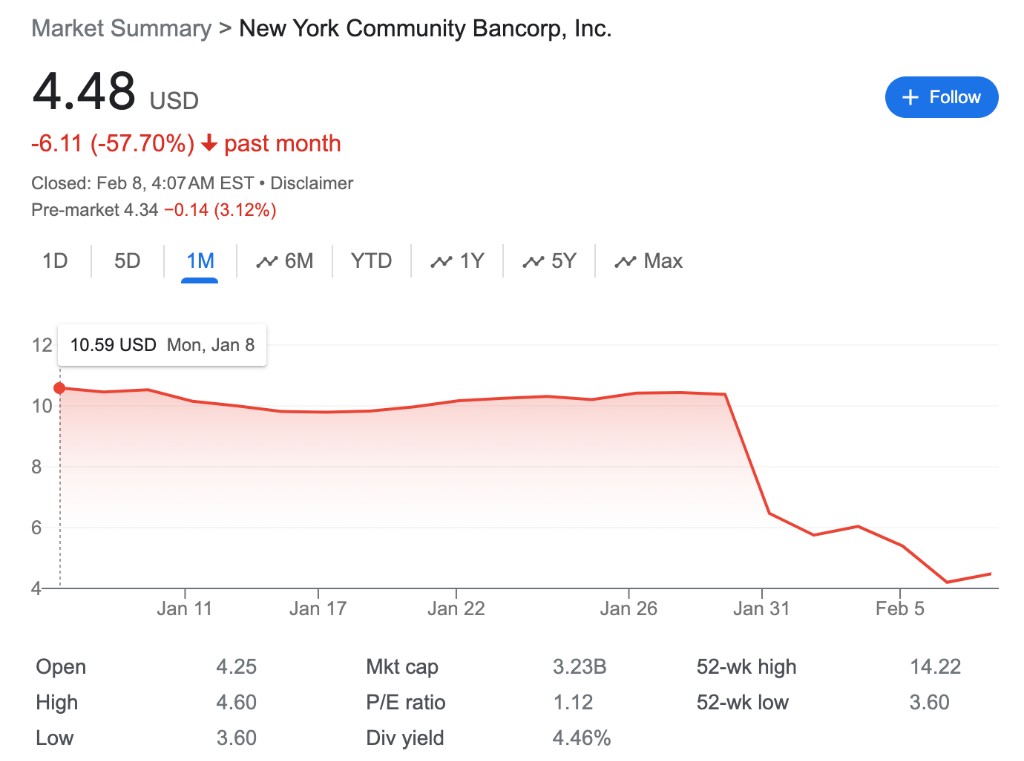

自上週公佈的去年第四季度財報意外虧損以來,紐約社區銀行股價已經蒸發了 50% 以上。

為了消除市場恐慌,當地時間 2 月 7 日週三,紐約社區銀行新任命 Alessandro DiNello 為執行董事長,立即生效。DiNello 將與首席執行官 Thomas Cangemi 合作,全面改善該行的運營。

前一天晚間時候,紐約銀行還在一份聲明中稱,其存款穩定在 830 億美元,有足夠的資源來應對任何可能出現的無保險存款外流。

另據媒體援引知情人士消息,紐約社區銀行目前正在尋求第三方資本,為其旗星銀行(Flagstar Bank)部門持有的住宅抵押貸款組合注入流動性。紐約社區銀行考慮以利率較低時發放的約 50 億美元住房貸款組合為支撐,開展所謂的合成風險轉移,即把這類貸款轉讓給買家來削減風險敞口。此外,它還在探索出售約 10 億美元的休旅車和船舶貸款組合。

而就在週二早些時候,國際評級機構穆迪將紐約社區銀行的信用評級,下調至 “垃圾級”。

穆迪表示,該行正面臨 “財務、風險管理和治理挑戰”,並補充道,如果情況惡化,它可能會進一步下調該銀行的評級。

至於紐約社區銀行危機發生的原因,還是要從那份財報説起。該行上週公佈的第四季度財報顯示,其計提了遠超預期十倍的貸款損失撥備,迫使其虧損高達 2.6 億美元,與市場此前預計的 2.06 億美元淨利潤大相徑庭。此外,該銀行還宣佈將股息削減至每股 5 美分,遠低於市場預期的 17 美分。

更深層的原因則是商業地產危機。在美國高利率環境下,商業地產的風險上升是不爭的事實。而地產行業和銀行業緊密掛鈎,當商業地產出現損失時,銀行的貸款壞賬率就會上升,銀行業也會被捲入漩渦。

Source: 華爾街見聞 The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments