Tech giants continue to suppress, Nasdaq falls for the third consecutive day, S&P rebounds narrowly, and NVIDIA surged 9% after earnings report.

美聯儲紀要後,美股指刷新日低,納指收創近三週新低,標普道指尾盤轉漲。英偉達財報前收跌 2.9%,財報帶動芯片股盤後齊漲,收跌 0.8% 的 AMD 盤後漲超 4%。收跌近 7% 的 AI“妖股” 超微(SMCI)盤後漲超 10%。中概股指反彈,收漲近 1%,理想汽車漲超 4%,阿里漲超 3%。法股五日連創歷史新高,滙豐跌超 8%。20 年期美債標售後,美債收益率加速回升。美聯儲紀要後,十年期美債收益率一度逼近兩個多月高位;美元指數短線轉漲,後重回跌勢。離岸人民幣盤中漲破 7.19 創三週新高,一度回落超 200 點,小幅收漲。原油反彈,逼近三個月高位。黃金跌落逾一週高位,美聯儲會議紀要後收窄跌幅。倫銅兩連漲至三週新高。

被高盛譽為“地球上最重要股票”的英偉達在週三美股盤後發佈財報。這一考驗市場對 AI 熱潮信心的重磅財報公佈前,英偉達股價繼續回落,領銜藍籌科技股拖累大盤。

午盤公佈的美聯儲 1 月末會議紀要顯示,聯儲官員擔心過快降息、擔心通脹下降停滯。有 “新美聯儲通訊社” 之稱的記者 Nick Timiraos 此後發文稱,紀要顯示,大多數聯儲官員擔心的是過早降息和價格壓力根深蒂固,而不是高利率保持過久,僅兩人指出長期高利率的風險。

紀要公佈後,主要美股指跌幅擴大,刷新日低,但跌勢並未持續,此後收窄跌幅甚至轉漲,雖然納指跌至近三週來收盤低位,但標普和道指憑藉尾盤轉漲驚險反彈。有評論稱,尾盤美股反彈源於害怕錯過(FOMO)心理引發的買盤,零日期權(0DTE)的資金也助推回漲。盤後英偉達公佈的上財季營收和本財季指引均高於預期,盤後英偉達止跌回漲,股價拉昇,帶動芯片股和 AI 概念股盤後齊漲。

美國財政部週三完成的 20 年期美國國債標售需求極為疲軟,反映需求的 “尾部”、即得標利率高於預發行利率差距為 20 年期美債標售有記錄以來最大,海外投資者獲配比創將近三年來新低。標售結果公佈後,美債價格跌幅擴大,收益率進一步回升,基準十年期美債收益率重上 4.30%,美聯儲紀要公佈後,收益率繼續上行,一度逼近上週所創的兩個多月來高位。

納指收創近三週新低 標普道指尾盤轉漲 英偉達財報帶動芯片股和 AI 概念股盤後齊漲

三大美國股指連續兩日集體低開,此後保持跌勢。道瓊斯工業平均指數盤初曾跌逾 170 點、跌超 0.4%,早盤尾聲時跌幅曾收窄到不足 14 點,午盤跌幅又擴大到 100 點以上。午盤美聯儲紀要公佈後,納斯達克綜合指數跌逾 1.1%,道指跌超 220 點,和標普 500 指數均跌近 0.6%,後低位反彈,尾盤納指跌幅收窄,標普和道指轉漲。

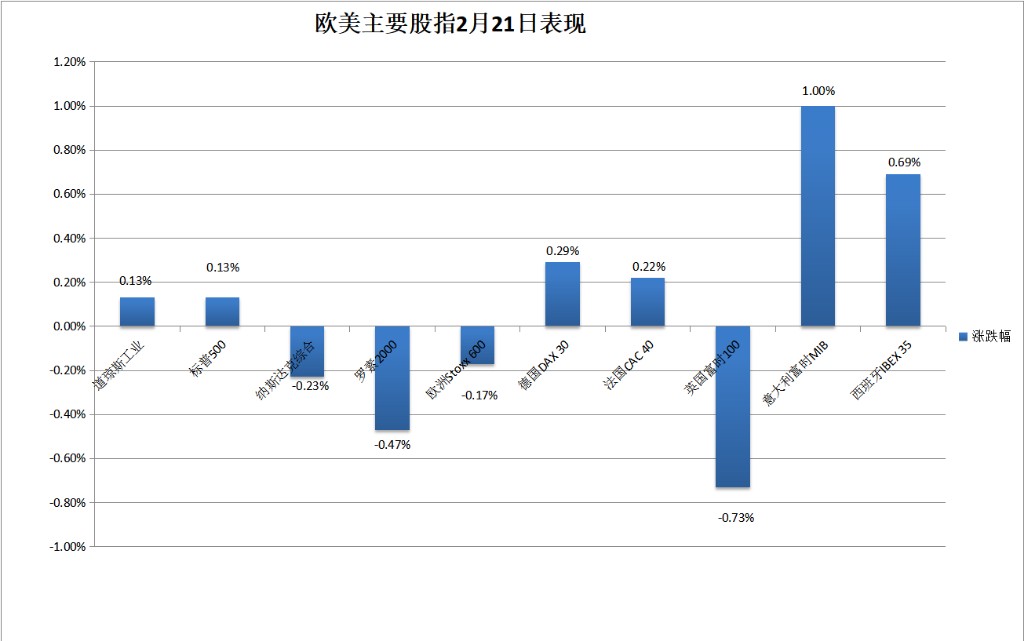

最終,三大指數中僅納指收跌,跌幅 0.23%,報 15580.87 點,連跌三個交易日,刷新 2 月 1 日以來收盤低位。標普收漲 0.13%,報 4981.8 點,未繼續逼近上週二美國 CPI 公佈後刷新的 2 月 5 日以來低位。道指收漲 48.44 點,漲幅 0.13%,報 38612.24 點,和標普均止住兩日連跌。

科技股為重的納斯達克 100 指數收跌 0.38%,連跌三日、兩日刷新 2 月 1 日以來收盤低位。衡量納斯達克 100 指數中科技業成份股表現的納斯達克科技市值加權指數(NDXTMC)盤中跌超 1%,收跌 0.9%,連跌四日至 2 月 1 日以來收盤低位。價值股為主的小盤股指羅素 2000 收跌 0.47%,刷新 2 月 13 日上週二以來收盤低位。

包括微軟、蘋果、英偉達、Alphabet、亞馬遜、Meta、特斯拉在內,七大科技股漲跌互見。特斯拉早盤曾漲逾 2.9%,午盤小幅轉跌,收漲 0.5%,在連跌兩日後,未繼續跌離上週四刷新的 1 月 24 日以來收盤高位。

FAANMG 六大科技股中,微軟、Facebook 母公司 Meta、奈飛早盤均曾跌超 1%,分別收跌近 0.2%、0.7% 和收跌 0.3%,微軟連跌四日,兩日刷新 1 月 31 日以來低位,Meta 和奈飛連跌三日至一週來低位;而連跌六日至 1 月 5 日以來收盤低位的蘋果午盤曾轉跌,收漲 0.4%,早盤曾跌超 1%;週二盤後公佈將於 2 月 26 日被納入道指成分股的亞馬遜早盤曾漲超 1%,收漲 0.9%;谷歌母公司 Alphabet 收漲近 1.2%,繼續脱離上週五刷新的 1 月 8 日以來收盤低位。

芯片股總體連跌四日,尾盤跌幅收窄。費城半導體指數和半導體行業 ETF SOXX 早盤即跌超 1%,收跌逾 0.2%,刷新 2 月 7 日以來收盤低位。個股中,週三盤後公佈財報的英偉達午盤曾跌 4.6%,收跌近 2.9%,在上週三創收盤歷史新高後連跌四個交易日,刷新 2 月 2 日以來收盤低位,盤後公佈財報後,股價跳漲,盤後漲幅曾達 9%;收跌超 2% 的英特爾盤後漲不足 1%,收跌 0.8% 的 AMD 盤後漲超 4%,而盤初跌超 4% 的 Arm 早盤轉漲,收漲超 1%,盤後漲約 6%。

AI 概念股總體繼續大跌,但盤後轉漲。今年初以來累漲超 150% 的 “妖股” 超微電腦(SMCI)午盤跌幅曾達 10%,收跌近 6.8%,盤後漲超 10%,收超 3% 的 C3.ai(AI)盤後漲超 5%, 收跌 5.5% 的 SoundHound.ai(SOUN)盤後漲超 8%,收跌超 9% 的 BigBear.ai(BBAI)盤後漲近 9%,收跌近 3% 的 Palantir(PLTR)盤後漲超 5%,收跌 0.6% 的 Adobe(ADBE)盤後漲約 0.5%。

熱門中概股總體反彈。納斯達克金龍中國指數(HXC)盤初曾漲逾 2.2%,收漲近 1%,在週二止步三連漲後重回漲勢。中概 ETF KWEB 和 CQQQ 均收漲超 1%。個股中,收盤時,理想汽車漲超 4%,阿里巴巴漲超 3%,京東、騰訊粉單漲超 2%,百度、小鵬汽車、B 站漲超 1%,蔚來汽車漲近 0.2%,而早盤轉跌的拼多多跌超 1%,網易跌 0.7%,新東方跌超 2%,比特幣礦機巨頭嘉楠科技跌超 12%。

公佈財報的個股中,下調全年營收和計費指引的網絡安全公司 Palo Alto Networks(PANW)收跌 28.4%;四季度營收和一季度指引均遜於預期的醫療保健公司 Teladoc(TDOC)和光伏股 Solaredge Technologies(SEDG)分別收跌 23.7% 和 12.2%;四季度營收高於預期仍連續四個季度下降的連鎖餐廳 Wingstop(WING)收跌 4.4%;而四季度營收和盈利高於預期的網站建設平台 Wix.Com(WIX)收漲近 6%;季度盈利高於預期的豪宅建築商 Toll Brothers(TOL)收漲近 4%。

歐股放慢,泛歐股指在四連漲後連續兩日回落。歐洲斯托克 600 指數繼續跌離週一刷新的 2022 年 1 月 5 日以來收盤高位。主要歐洲國家股指大多上漲,法股連續五個交易日創收盤歷史新高,連續兩日跌離收盤歷史高位的德股反彈,西班牙和意大利西股指分別三連漲和兩連漲,而英股在四連陽後連跌兩日。

各板塊中,銀行收跌近 1.1%,源於公佈四季度虧損 1.5 億美元、持股交行相關減記 30 億美元后,英國最大銀行滙豐股價重挫 8.4%,創 2020 年 4 月以來最大日跌幅;週一和週二領跌的礦業股所在板塊基礎資源跌 0.8%,受累於年度利潤下滑的力拓跌 1.5%,盈利慘淡且大幅削減股息的嘉能可跌 1.1%,和滙豐共同拖累英股在歐洲各國中表現最差;醫療板塊跌逾 0.7%,跌落十個月高位,歐洲最高市值藥企諾和諾德收跌近 1.5%,繼續跌離截至週一連續五日所創的收盤紀錄高位。

美聯儲紀要後 十年期美債收益率一度逼近兩個多月高位

美國 10 年期基準國債收益率在歐股盤中曾下破 4.25% 刷新日低,日內降近 3 個基點,美股早盤抹平降幅轉升,午盤 20 年期美債標售結果公佈後,迅速升破 4.30%,美聯儲紀要公佈後,一度接近 4.33%,逼近上週二升至 4.33% 刷新的 2023 年 12 月 1 日以來高位,日內升約 5 個基點,到債市尾盤時約為 4.32%,日內升逾 4 個基點,在週二大致收平後,重回上週五的反彈勢頭。

對利率前景更敏感的 2 年期美債收益率在歐股盤中曾下破 4.58% 刷新日低,美股早盤轉升,午盤 20 年期美債標售完成後,升破 4.65%,美聯儲紀要公佈後,保持升勢,尾盤曾上測 4.67%,還未逼近上週五接近 4.72% 刷新的去年 12 月 13 日美聯儲議息會議首日以來高位,到債市尾盤時約為 4.67%,日內升約 6 個基點,在週二回落後反彈。

美聯儲紀要後 美元指數短線轉漲 離岸人民幣盤中漲破 7.19 一度回落超 200 點

追蹤美元兑歐元等六種主要貨幣一籃子匯價的 ICE 美元指數(DXY)在亞市早盤曾跌破 104.00 刷新日低,向週二跌破 103.80 刷新的 2 月 9 日以來盤中低位靠近,日內跌逾 0.1%,歐股盤前轉漲後曾漲破 104.20 刷新日高,日內漲逾 0.1%,後幾度轉跌,午盤美聯儲紀要公佈後曾短線轉漲,後很快重回跌勢,尾盤跌破 104.00。

到週三美股收盤時,美元指數略低於 104.00,日內跌不足 0.1%,繼續刷新 2 月 7 日以來同時段低位;追蹤美元兑其他十種貨幣匯率的彭博美元現貨指數微跌,連跌三日。

非美貨幣中,歐元兑美元在美聯儲紀要公佈後曾漲破 1.0820,靠近週二逼近 1.0840 刷新的 2 月 2 日以來高位,日內漲 0.2%;英鎊兑美元在美聯儲紀要公佈後漲破 1.2640 刷新日高,接近週二刷新的一週高位;連續兩日反彈的日元回落,美元兑日元美股午盤曾上測 150.40 刷新日高,美聯儲紀要公佈後曾漲幅擴大、接近日高,美股收盤時處於 150.20 上方。

離岸人民幣(CNH)兑美元在在亞市早盤刷新日低至 7.2070,後很快轉漲,亞市盤中曾漲至 7.1811,刷新 1 月 31 日以來盤中高位,較日低漲 259 點,後持續回吐漲幅,美股午盤曾跌落 7.2020,較日高回落超 200 點。北京時間 2 月 22 日 5 點 59 分,離岸人民幣兑美元報 7.1994 元,較週二紐約尾盤漲 23 點,連漲六個交易日。

比特幣(BTC)在亞市早盤曾漲破 5.24 萬美元刷新日高,後總體回落,歐股盤中曾下測 5.06 萬美元刷新日低,較日高跌超 1000 美元、跌超 3%,美股收盤時處於 5.1 萬美元上方,最近 24 小時跌近 2%,跌離週二衝擊 5.3 萬美元關口刷新的 2021 年 12 月以來高位。

原油反彈 逼近三個月高位

國際原油期貨盤中轉漲。歐股盤前刷新日低時,美國 WTI 原油跌至 76.32 美元,日內跌逾 0.9%,布倫特原油跌至 81.66 美元,日內跌逾 0.8%,美股盤前轉漲後保持漲勢,美股午盤刷新日高時,美油漲至 78.08 美元,日內漲逾 1.3%,布油漲至 83.17 美元,日內漲 1%。

最終,週二回落的原油反彈。週二止步兩連漲的 WTI 4 月原油期貨收漲.13%,報 77.91 美元/桶,靠近上週五刷新的 2023 年 11 月 6 日以來收盤高位;布倫特 4 月原油期貨收漲 0.84%,報 83.03 美元/桶,逼近週一連漲三日、連續兩個交易日刷新的 2023 年 11 月 6 日以來高位。

倫銅兩連漲至三週新高 黃金跌落逾一週高位 美聯儲會議紀要後收窄跌幅

倫敦基本金屬期貨週三多數上漲。倫銅和倫鉛連漲兩日,倫銅收盤漲破 8500 美元,創 1 月末以來新高,倫鉛創兩週新高。四連跌的倫鋁和兩連跌的倫鎳均反彈,倫鋁走出 1 月下旬以來低位,倫鎳創 12 月末以來新高。週二回落的倫鎳逼近週一所創的一週多來高位。而倫錫連跌六個交易日,創近兩週新低。

紐約黃金期貨在亞市盤中刷新日高至 2043.5 美元,日內漲近 0.2%,後多次轉跌,美股早盤轉跌後未能再轉漲,美股午盤美國會議紀要公佈後,先曾下測 2030.90 美元刷新日低,日內跌超 0.4%,後跌幅收窄,曾接近 2038 美元,日內跌不到 0.1%。

到收盤,連續三個交易日收漲的 COMEX 4 月黃金期貨收跌 0.27%,報 2034.3 美元/盎司,跌落週二刷新的 2 月 8 日以來收盤高位。

現貨黃金在歐股盤前曾漲破 2032.30 美元,連續兩日刷新 2 月 13 日上週二以來盤中高位,美聯儲紀要公佈後先刷新日低逼近 2020 美元,後逐步抹平日內降幅。