The "Creators" behind the chips usher in a brand new era! Wall Street senses the scent of a "bull market".

芯片製造商台積電以及其供應商阿斯麥和應用材料等,將迎來新的 “黃金時代”。台積電重返全球上市公司市值前十,其股價今年以來漲幅高達 37%。在 AI 芯片需求激增的背景下,台積電的業績有望同步激增。同時,台積電的供應商們銷售額也將不斷擴大,因為台積電等製造商將擴大 AI 芯片產能,大量採購高端半導體設備。這些供應商包括阿斯麥、應用材料、東京電子和 BE Semiconductor 等。從 2024 年開始,這些 “締造者們” 將在全球佈局 AI 的浪潮中迎來新的 “黃金時代”。

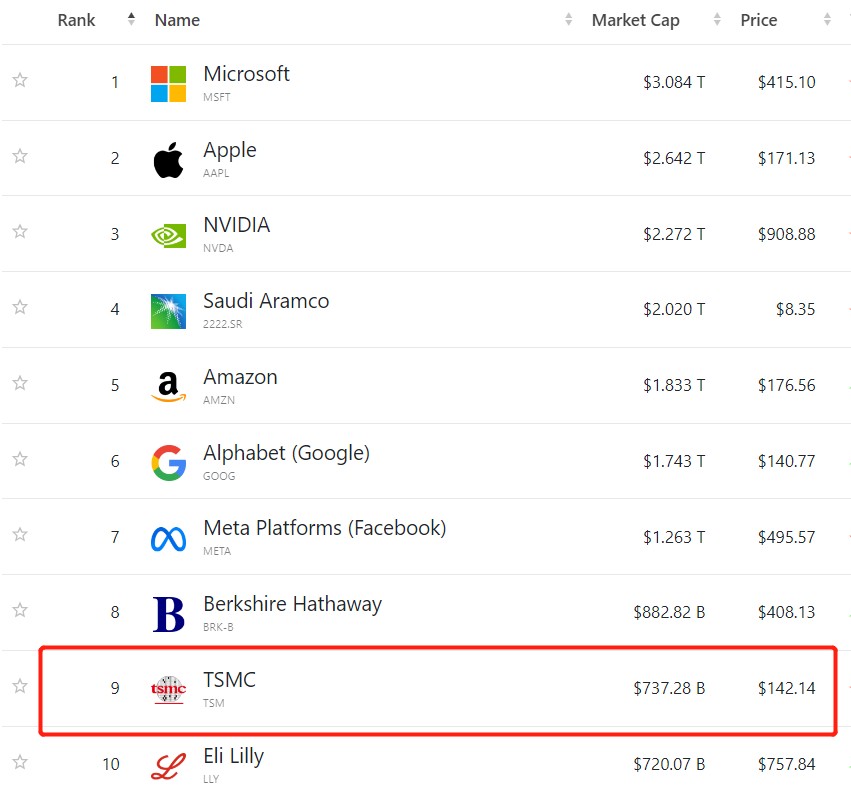

時隔四年之久,有着 “芯片代工之王” 稱號的台積電重返全球上市公司市值前十之列,台積電美股 ADR 今年以來漲幅高達 37%,大幅跑贏費城半導體指數。在當前 AI 芯片需求激增背景下,作為全球 AI 芯片領導者英偉達以及 AMD AI 芯片唯一代工廠,以及微軟和亞馬遜等雲巨頭自研 AI 芯片唯一代工廠的台積電勢必持續受益。手握全球最頂級造芯技藝以及最頂尖 Chiplet 先進封裝,台積電的 “英偉達時刻”——即股價與業績開啓同步激增的時刻,或許已經到來。

與此同時,共同締造 AI 芯片的 “大師們”——即台積電最關鍵半導體設備的供應商們銷售額 2024 年起勢必將不斷擴大,主要因台積電、三星電子以及英特爾等芯片製造商們不斷擴大基於 5nm 及以下先進製程的 AI 芯片產能,以及台積電在美國、日本和德國的大型芯片製造廠有望於今年起陸續完工而大批量採購造芯所需光刻機、刻蝕設備以及薄膜沉積等高端半導體設備。這些半導體設備供應商們主要包括阿斯麥 (ASML)、應用材料、東京電子與 BE Semiconductor 等芯片產業鏈頂級設備商。

2023 年 ChatGPT 風靡全球,2024 年 Sora 文生視頻大模型重磅問世以及 AI 領域 “賣鏟人” 英偉達連續四個季度無與倫比的業績,或意味着人類社會 2024 年起逐步邁入 AI 時代。而台積電、阿斯麥以及應用材料等共同締造對於人類科技發展最重要的底層硬件——芯片的 “締造者們” 經歷堪稱 “黃金時代” 的 PC 時代與智能手機時代後,從 2024 年開始,或將在全球佈局 AI 的這波浪潮中迎來嶄新的 “黃金時代”。

SIA(美國半導體行業協會) 公佈的最新數據顯示,1 月全球半導體行業銷售額總額高達 476 億美元,與 2023 年 1 月相比增長 15.2%。事實上,半導體行業銷售額自 2023 年末開始因 AI 芯片強勁需求而明顯回升。SIA 統計的 2023 年第四季度銷售額約為 1460 億美元,比 2022 年第四季度銷售額增長 11.6%,相比於 2023 年第三季度銷售額環比增長 8.4%。關於 2024 年半導體行業銷售額預期,SIA 總裁兼首席執行官 John Neuffer 在數據報告預計 2024 年整體銷售額將相比於 2023 年實現兩位數級別增幅。

SEMI(國際半導體產業協會) 在最新公佈的年度硅出貨量預測報告中指出,隨着硅晶圓和整個半導體行業需求復甦和庫存水平正常化,以及硅晶圓需求大幅增加以支持人工智能 (AI)、高性能計算 (HPC)、5G、汽車和工業應用等領域,全球硅晶圓出貨量將在 2024 年全面反彈,2025 年有望更加強勁。SEMI 硅晶圓數據包括硅晶圓製造商發往最終用户的拋光硅晶圓和外延硅晶圓,不包括未拋光或回收的晶圓。這些硅晶圓將被送至台積電等芯片製造商處進行精細加工,通過極其複雜的製造過程在硅晶圓上製成集成電路 (ICs)。

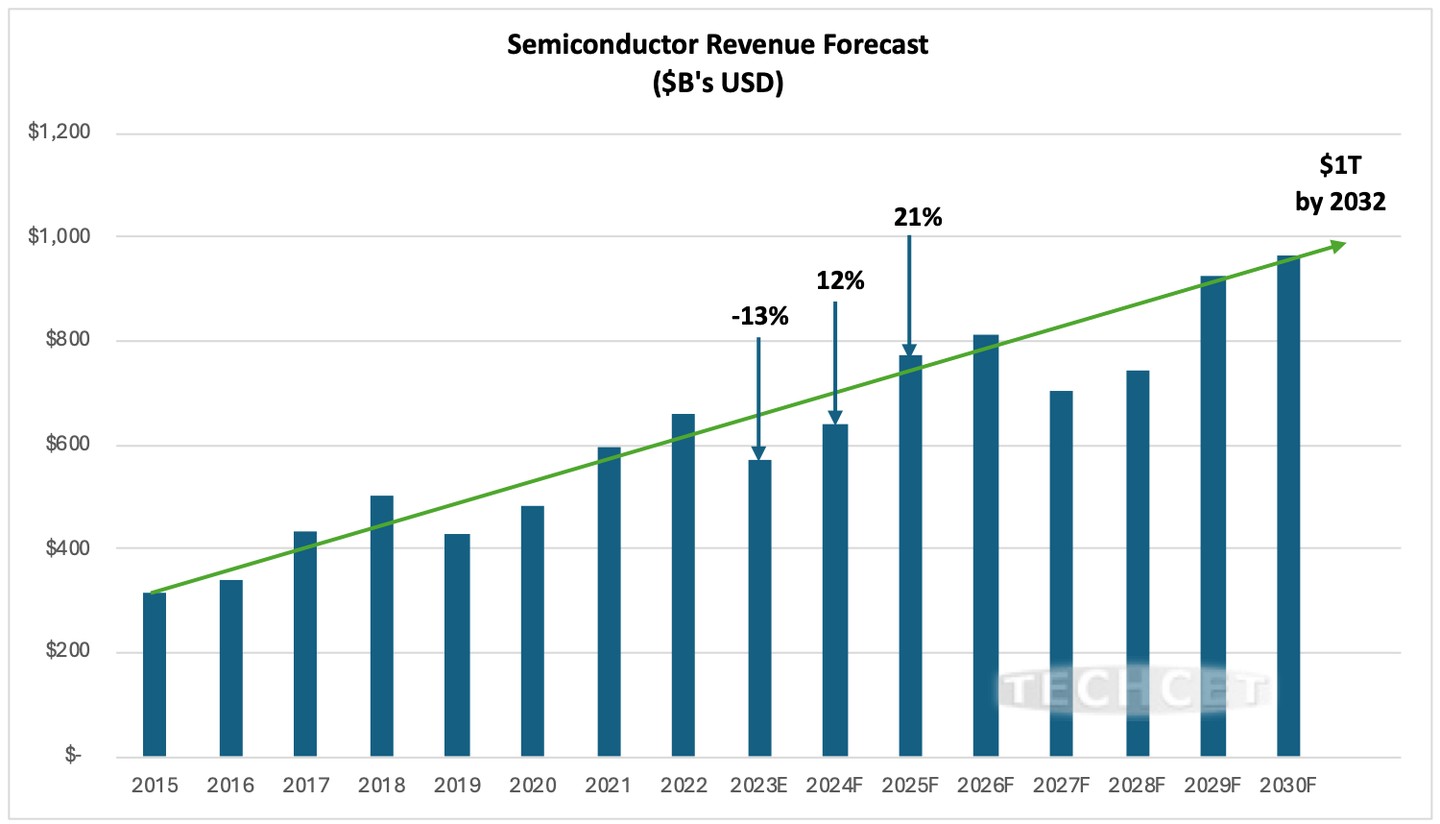

TECHCET 近日發佈重磅預測報告,預計 2024 年 AI 芯片持續強勁的需求將引領全球半導體市場進入新一輪上行週期。TECHCET 預計 2024 年半導體行業銷售額有望大幅增長 12%,隨後 2025 年在 AI 芯片以及更廣泛芯片需求刺激下將出現更猛烈增幅,達到 21%。TECHCET 預計 2031 或 2032 年全球半導體市場規模有望破萬億美元大關。

台積電,坐擁頂級造芯技藝 +chiplet” 封裝神技”

台積電 (TSM.US) 憑藉在芯片製造領域數十年的造芯技術積澱,以及長期處於芯片製造技術改良與創新的全球最前沿 (開創 FinFET 時代,引領 2nm GAA 時代),以領先全球芯片製造商的先進製程以及超高良率長期以來霸佔全球絕大多數芯片代工訂單,尤其是 5nm 及以下先進製程的芯片代工訂單。

目前需求最為旺盛的 AI 訓練/推理端高性能 AI 芯片,比如英偉達 H100、AMD MI300 系列,全線應用於全球各大數據中心的服務器端。而台積電,可謂以一己之力卡着英偉達和 AMD 的脖子。

英偉達 (NVDA.US) 和 AMD(AMD.US) 這兩大 AI 芯片領域最強勢力均集中採用台積電 5nm 製程,後續新推出的 AI 芯片有望採用基於台積電 chiplet 先進封裝的 3nm 搭配 4nm 製程。因此,憑藉着無與倫比的 3nm、4nm 和 5nm 先進製程工藝,台積電對全球 AI 芯片供應規模的影響可謂巨大。台積電高管們預計在未來幾年內,AI 相關芯片的營收年複合增長率將達到 50%,凸顯其在 AI 領域的重要性和營收增長潛力。

台積電當前是英偉達旗下需求無比強勁的 AI 芯片——A100/H100 唯一芯片代工商,而英偉達則是全球 AI 芯片市場的絕對主導者,佔有高達 80%—90% 的市場份額。華爾街大行花旗預計 2024 年的 AI 芯片市場規模將在 750 億美元左右,同時預計 AMD 最新推出的旗艦款 AI 芯片 MI300X 能夠佔據約 10% 份額,而台積電同樣為 AMD 的獨家芯片代工商。這些都顯示出台積電在為頂級芯片公司提供代工服務方面無與倫比的重要性。

當前 AI 芯片供給遠無法滿足需求,在 2 月英偉達業績會議上,CEO 黃仁勳表示,今年剩餘時間,英偉達最新產品將繼續供不應求。黃仁勳強調,儘管供應不斷增長,但需求並沒有顯示出任何程度放緩跡象。

市場預期方面,在 “Advancing AI” 發佈會上,英偉達最強競爭對手 AMD 將截至 2027 年的全球 AI 芯片市場規模預期,從此前預期的 1500 億美元猛然上修至 4000 億美元,而 2023 年 AI 市場規模預期僅僅為 300 億美元左右。

據瞭解,在 AMD MI300 系列中,Instinct MI300A 為數據中心 APU,結合 GPU 核心、Zen 4 CPU 核心、128GB HBM3,共 1460 億個電晶體,利用台積電的 3D chiplet 先進封裝整合 5nm 與 6nm 製程所生產的芯粒 (chiplet)。

AMD Instinct MI300X 這一款 GPU 則基於全新 AMD CDNA 3 架構,擁有最多 8 個 XCD 核心,304 組 CU 單元,8 組 HBM3 核心,共有超 1500 億個晶體管,整合 5nm 以及一部分 6nm 製程芯粒。封裝方面,MI300X 則採用的是 2.5D 硅中介層、3D 混合鍵合集一體的台積電全新 3.5D chiplet 先進封裝。MI300X 顯存容量最大可達 192GB。

此外,有媒體爆料稱,英偉達將於 3 月 18 日召開的 GTC 大會上公佈的全新 AI 芯片——B100,也將採用台積電先進封裝,並且可能將採用集成 CoWoS 以及 3D SoIC 封裝為一體的 chiplet 先進封裝。作為 Hopper 系列的繼任者,B100 被寄予厚望,被業界認為是大語言模型 (LLM) 訓練和推理的最強硬件。一直看漲英偉達的美國銀行分析師 Vivek Arya 預計英偉達即將推出的 B100 定價將比 H100 至少高出 10% 至 30%。

從英偉達與 AMD 這兩大 AI 芯片領導者產品能夠看出,他們所設計的 AI 芯片最終產能,全面依賴於台積電 “Chiplet 先進封裝產能”。

在 “後摩爾時代”(Post-Moore Era),芯片先進製程突破面臨極大難度 (如量子隧穿效應以及開發成本指數級增長),加之逐漸邁入 AI 時代以及萬物互聯趨勢愈發明顯,多種任務帶來的算力需求可能激增,比如深度學習任務、訓練/推理、AI 驅動的圖像渲染、識別等。這些任務對硬件性能要求都非常高,這意味着像 PC 那樣單獨集成的 CPU 或 GPU 已經無法滿足算力需求。

因此,Chiplet 先進封裝應運而生,該技術允許將不同的 “芯片處理單元”,即將不同的 “chiplet 芯粒” 集成在一起,滿足多樣的計算需求,從而更好地優化性能。Chiplet 封裝技術可以使不同的 GPU 模塊,或者 CPU、FPGA、ASIC 芯片等在同一個系統中協同工作,最大化地高效調度各類型芯片算力,以提供更大規模的並行計算能力。

台積電當前憑藉其領先業界的 2.5D/3D 先進封裝吃下市場幾乎所有 5nm 及以下製程高端芯片封裝訂單,並且先進封裝產能遠無法滿足需求,英偉達 H100 供不應求正是受限於台積電 2.5D 級別的 CoWoS 封裝產能。有媒體爆料稱,由於英偉達 H100 以及 B100 訂單數量無比龐大,加之 AMD 訂單同樣火爆,基於台積電 3nm、4nm 以及 5nm 製程的先進封裝產能已全線滿載,並且可能向 Amkor 等封測廠借調產能。

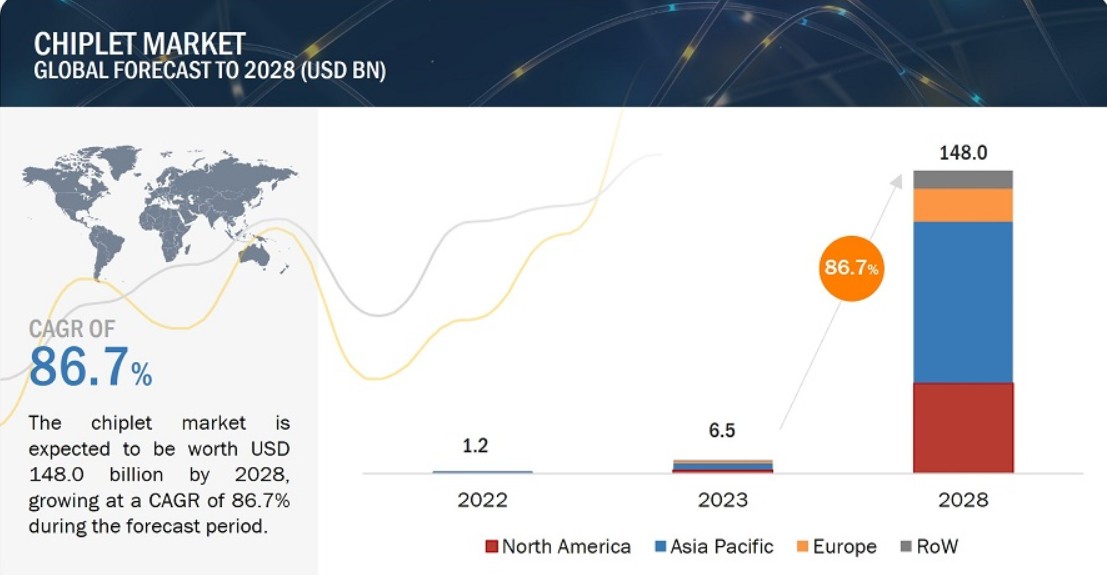

IDC 預計至 2024 下半年,台積電 CoWoS 產能有望大幅增加約 130% 。另一研究機構 Markets And Markets 最新研究顯示,覆蓋 GPU、CPU、FPGA 等芯片的 Chiplet 先進封裝成品、先進封裝技術 (2.5D/3D、SiP、WLCSP、FCBGA 和 Fan-Out 等) 的 Chiplet 市場總額有望於 2028 年達到約 1480 億美元,年複合增速 (CAGR) 高達驚人的 86.7%。根據該機構測算,2023 年 Chiplet 市場總額可能僅為 65 億美元。

“台積電之父” 張忠謀近日在台積電位於日本的第一家芯片製造廠成立的開業儀式上表示,根據他與全球頂級芯片公司高管們的探討,目前全球對包括 AI 芯片在內的芯片產能需求無比龐大。張忠謀表示:“這些頂級芯片公司幾乎都在談論,他們需要我們在全球建立更多的芯片製造廠,需求不是幾萬片或幾十萬片晶圓,而是三座、五座甚至是十座大型的芯片廠。”

台積電股價預期方面,華爾街大行摩根大通近日將台積電台股 12 個月目標價從 770 新台幣上調至 850 新台幣 (最新收盤價為 784 新台幣)。摩根大通預計,在未來三到四年內,台積電將在 AI 相關芯片代工份額中保持超過 90% 份額。摩根大通強調,台積電擁有領先全球的先進封裝技術、頂級製程工藝以及半導體行業最廣泛的 IP 和設計服務生態系統支持,台積電在 Al 芯片領域的護城河似乎比以前的產品週期更寬。

13F 披露數據顯示,高盛、野村以及老虎環球等多家華爾街投資機構第四季度紛紛斥巨資加倉台積電美股 ADR。根據 TipRanks 彙編的華爾街分析師目標價,台積電 ADR 最高的看漲價位高達 185 美元 (最新收盤價為 142.14 美元);知名投資機構 Susquehanna 近日將台積電 ADR 12 個月目標價從 130 美元大幅上調至 160 美元,維持 “跑贏大盤” 評級;滙豐研究近日將台積電 ADR 目標價從 119 美元大幅上調至 164 美元,維持 “買入” 評級。

半導體設備巨頭們,手握 “造芯命脈”

隨着台積電在美國、日本以及德國大型芯片製造廠有望於今年起陸續完工,以及另一芯片製造巨頭三星電子的美國工廠有望 2024 年完成建設,並於 2025 年開始生產 5nm 以下先進製程芯片,台積電與三星 2024 年起可能將大批量採購造芯所需的光刻機、刻蝕設備以及薄膜沉積等高端半導體設備。

更重要的是,正如台積電創始人張忠謀所述,AI 芯片需求旺盛,台積電、三星以及英特爾等芯片製造商將全面擴大產能,加之 SK 海力士以及美光等存儲巨頭擴大 HBM 產能,均需要大批量採購芯片製造與先進封裝所需半導體設備,甚至一些核心設備需要更新換代。畢竟 AI 芯片擁有更高邏輯密度,更復雜電路設計,以及對設備更高的功率和精準度要求,這可能導致在光刻、刻蝕、薄膜沉積、多層互連以及熱管理等環節有更高的技術要求,進而需要定製化製造和測試設備來滿足這些要求。因此阿斯麥、應用材料等半導體設備巨頭們,可謂手握 “造芯命脈”。

在一些分析人士看來,台積電智能手機以及 PC 芯片產能可能僅一小部分能夠轉移至數據中心 AI 芯片生產線。畢竟隨着智能手機和 PC 於 2024 年開啓 “AI 消費電子元年”,AMD、博通以及高通對於 AI 智能手機以及 AI PC 芯片的產能需求將佔據台積電產能。

台積電手機芯片產能長期以來幾乎一半被最大客户蘋果所佔據,並且智能手機需求出現復甦信號。TechInsights 最新統計顯示,2023 年 Q4 全球智能手機出貨量同比反彈 7.1%,達到 3.17 億部,結束連續九個季度的低迷態勢,蘋果以 23% 份額位居全球智能手機市場之首。在 2023 年出貨量下降約 4% 後, Canalys 預計 2024 年全球智能手機市場有望實現温和復甦,預計 2024 年出貨量將增長 4% 達 11.7 億部。

SEMI 在預測報告中強調,2024 年開始 AI 以及 HPC 需求將佔據多數硅晶圓需求,研究機構 Gartner 同樣預計生成式 AI 和 LLM 發展將全面推動數據中心部署基於 AI 芯片的高性能服務器。這也意味着台積電等芯片製造商需要擴大產能製造更多 AI 芯片,且需要更新或大批量採購半導體制造設備,比如更新至精準度更高或複雜度方面技術要求更高的製造設備,以及大量採購 chiplet 先進封裝所需的製造以及檢測設備,2.5D 與 3D 等先進封裝比傳統封裝體系複雜得多,尤其在對齊和組裝方面。因此,2024 年硅晶圓擴張預期意味着打造 AI 芯片所需的半導體設備需求預期也跟隨擴張。

來自荷蘭的阿斯麥 (ASML.US) 是全球最大規模光刻系統製造商,阿斯麥所生產的光刻設備在製造芯片的過程中可謂起着最重要作用。阿斯麥是台積電、三星以及英特爾用於製造高端芯片的最先進製造極紫外 (EUV) 光刻機的唯一供應商。

如果説芯片是現代人類工業的 “掌上明珠”,那麼光刻機就是將這顆 “明珠” 生產出來所必須具備的工具,更重要的是,阿斯麥是全球芯片廠製造最先進製程的芯片,比如 3nm、5nm 以及 7nm 芯片所需 EUV 光刻設備的全球唯一供應商。

對於台積電正在研發的 2nm 及以下節點技術而言,阿斯麥 high-NA EUV 光刻機至關重要。相比於阿斯麥當前生產的標準 EUV 光刻機,主要區別在於使用了更大的數值孔徑,High-NA EUV 技術採用 0.55 NA 鏡頭,能夠實現 8nm 級別的分辨率,而標準的 EUV 技術使用 0.33 NA 的鏡頭。因此,這種新 NA 技術能夠在晶片上打印更小的特徵尺寸,對於 2nm 及以下芯片的製程技術研發至關重要。

在芯片廠,應用材料 (AMAT.US) 的身影可謂無處不在。不同於阿斯麥始終專注於光刻領域,總部位於美國的應用材料提供的高端設備在製造芯片的幾乎每一個步驟中發揮重要作用,其產品涵蓋原子層沉積 (ALD)、化學氣相沉積 (CVD)、物理氣相沉積 (PVD)、快速熱處理 (RTP)、化學機械拋光 (CMP)、晶圓刻蝕、離子注入等重要造芯環節。應用材料在晶圓 Hybrid Bonding、硅通孔 (Through Silicon Via) 這兩大 chiplet 先進封裝環節擁有高精度製造設備和定製化解決方案,對於 2.5D、3D 先進封裝步驟至關重要。

來自荷蘭的 ASM International 提供的設備則在 ALD 領域處於全球領先地位,而製造 AI 芯片過程中,ALD 無疑扮演重要角色,ALD 技術環節對於製造具有高度集成度和更加複雜結構的 AI 芯片來説非常重要。此外,ALD 對於向全環繞柵極 (GAA) 技術的轉變以及對精確閾值電壓調諧的需求也至關重要。

對 chiplet 先進封裝至關重要的 Hybrid Bonding 領域,BE Semiconductor 這家位於荷蘭的半導體設備公司所獨有的 “混合鍵合”(Hybrid Bonding) 先進封裝技術——一種用於連接不同 “芯粒” 並提高其性能的創新高端鍵合技術,從最初的採用階段進入產能擴張階段。高盛預計,到 2027 年,BE Semiconductor“混合鍵合” 先進封裝帶來的營收規模至少超 5 億歐元,而 2022 年僅僅約為 5000 萬歐元,並指出該公司已經收到芯片製造商台積電的產能擴張大訂單。

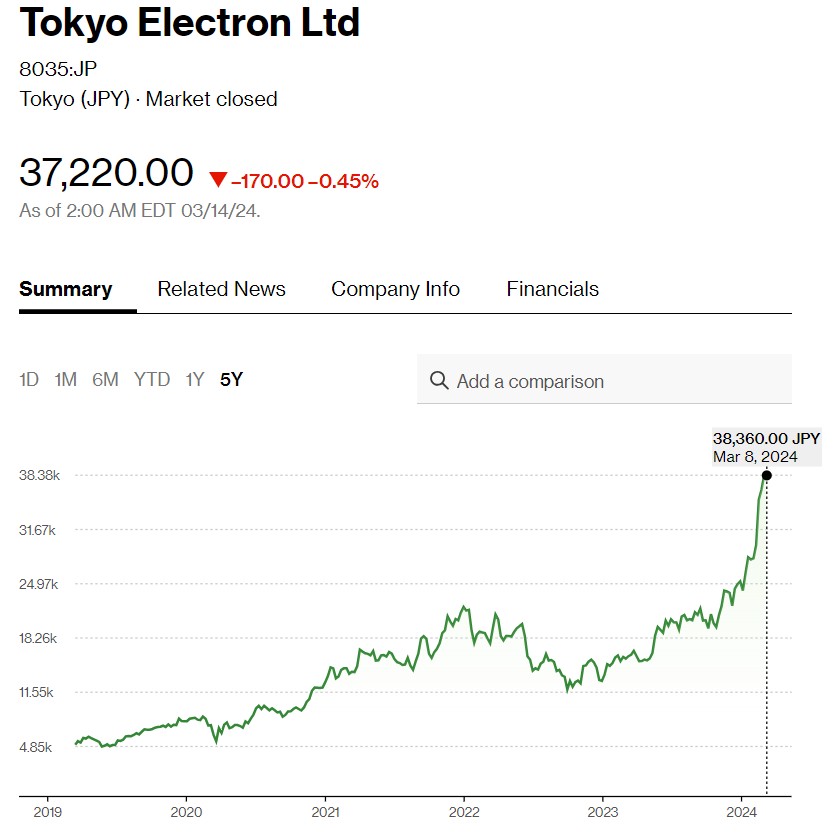

同樣聚焦於芯片製造環節多個步驟的半導體設備公司還包括美國泛林集團與來自日本的東京電子 (Tokyo Electron)。相比於應用材料和泛林,東京電子在塗覆機以及顯影機 (Coater/Developer) 領域具有非常高市佔率。東京電子在 ALD、CVD、PVD、RTP、CMP、刻蝕和離子注入設備等領域為應用材料最強競爭對手。

華爾街資管巨頭們可謂早已提前埋伏這些半導體設備商,在高盛、摩根士丹利以及摩根大通等頂級機構的 13F 持倉中均能看到應用材料等巨頭身影。股價預期方面,半導體設備領導者應用材料可謂獲華爾街高度看漲,儘管應用材料股價 2024 年以來屢創歷史新高,但華爾街投資機構伯恩斯坦 (Sanford C. Bernstein) 近期將應用材料 12 個月目標價從 230 美元進一步上調至 240 美元 (最新收盤為 200.56 美元),瑞銀集團則將應用材料目標價從 185 美元大幅上調至 235 美元。

應用材料競爭對手東京電子也獲華爾街看好,傑富瑞 (Jefferies) 近期將東京電子 12 個月目標價從 30000 日元大幅上調至 42000 日元 (最新收盤為 37220 日元),東京電子今年以來股價屢創新高,當前徘徊於歷史最高位附近。傑富瑞還看漲受益於 AI 浪潮的 ALD 領域領軍者 ASM International ,予以 740 歐元目標價 (最新收盤為 566 歐元)。

專注於 “混合鍵合” 領域的BE Semiconductor,可謂歐洲股市圍繞 AI 投資熱潮的最大受益者之一,其股價在 2023 年狂飆 140%,今年則屢創新高。高盛預計 BE Semiconductor 在 2024 年仍有上行空間,主要因市場對該公司先進封裝設備需求將非常強勁。高盛分析團隊預計未來 12 個月該股有望上漲至 170 歐元 (最新收盤為 141 歐元)。根據 TipRanks 彙編的華爾街分析師目標價,BE Semiconductor 最高看漲價位高達 200 歐元。

中國力爭解決半導體設備這一 “卡脖子難題”

近幾年,美國對於中國芯片產業鏈的制裁不斷升級,且集中於半導體設備、原材料以及芯片製造環節。因此,為實現芯片製造領域全方位國產化,芯片製造所需的各種高端半導體設備這一基本上處於 “從 0 到 1” 的初步發展領域,乃各級政府資金以及民間資金最核心聚焦領域。

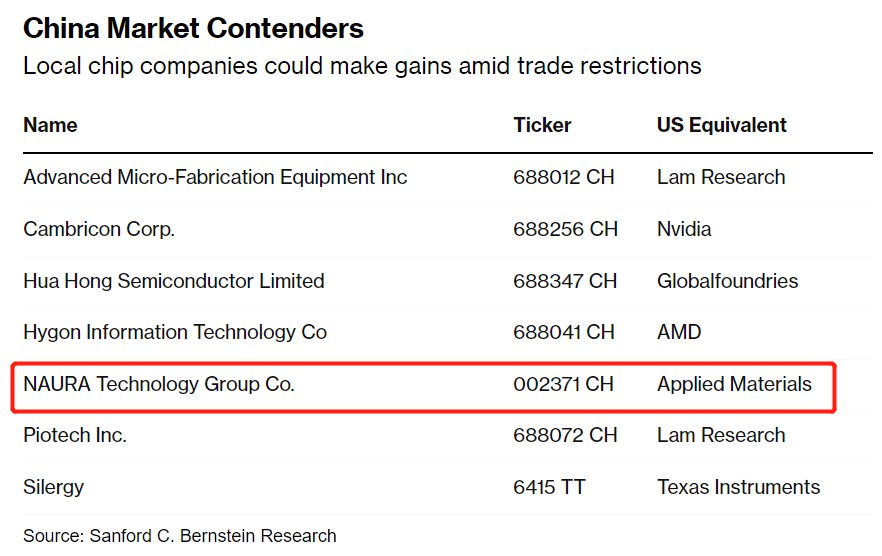

來自巴克萊銀行 (Barclays) 和伯恩斯坦公司 (Sanford C. Bernstein) 的分析師們表示,Naura Technology Group(北方華創) 等半導體設備公司的名字有一天可能將與應用材料以及泛林集團 (LAM Research) 等美國半導體設備同行一樣聞名全球。其中,伯恩斯坦分析師們將北方華創直接對標半導體設備巨頭應用材料 (Applied Materials)。

這些華爾街分析師的理由很簡單:美國限制中國獲取尖端半導體設備技術的努力將促進國內半導體設備領域蓬勃發展,併為本土企業創造巨大機遇,對這些企業的投資可能將在未來幾年獲得回報。

作為對於美國商務部對應用材料以及阿斯麥等最尖端半導體設備全面禁止流入中國以及禁止英偉達高端 AI 芯片進入中國市場的回應,中國已經投入了超過 1000 億美元的龐大資金,努力創建能夠填補空白的國內供貨商。伯恩斯坦的分析師近期在一份研究報告中寫道:“美國的制裁是一把雙刃劍,雖然可能會壓制中國在尖端半導體設備領域的發展,但也將迫使中國迅速發展自身供應鏈,努力實現自給自足。”

巴克萊的分析師們則表示,中國到 2025 年實現國產芯片自給率達到 70% 的計劃存在挑戰,中國減少對進口的依賴需要過程,但隨着數百億美元的政府資金投入到本地芯片企業,中國芯片產業鏈的半導體設備商以及芯片製造商所扮演的角色將變得日益重要,預計未來 5 到 7 年內國產芯片產量有望翻番。