Finally, a major bank has called it: interest rate cuts are a matter for 2024, and now we should discuss "what will cause the Federal Reserve to raise interest rates"?

美銀認為,最新的非農數據意味着穩就業目標已經實現,因此美聯儲沒有進一步降息的必要。如果核心 PCE 物價指數同比增速超過 3%、長期通脹預期失控,將為美聯儲下一步加息奠定基礎。

上週五公佈的非農數據意外強勁,重燃通脹擔憂,美聯儲的降息前景是否就此被扭轉?

近日,美銀多個團隊陸續發佈最新研報,就美聯儲今年的貨幣政策路徑進行了展望。

美銀分析師 Aditya Bhave 領導的經濟團隊認為,12 月的非農數據意味着美聯儲降息週期的結束,考慮到當前的通脹仍高於目標且有上行風險,而勞動力市場已有企穩趨勢,可能為美聯儲轉向加息打開大門。

美銀分析師 Ebrahim H. Poonawala 領導的銀行團隊則預計,利率前景仍不明朗,10 年期美債收益率可能繼續上行至接近 5% 的水平。

隨着美聯儲加息的可能性不斷放大,美銀分析師 Mark Cabana 領導的利率團隊全面上調了今年對各期限美債收益率的預期值,並警告長債收益率短期內飆升可能帶來的衰退和滯脹風險。

穩就業目標暫時完成,焦點再次轉向通脹

美國 12 月非農報告顯示,12 月新增就業 25.6 萬人,為九個月最大增幅,遠超預期的 16.5 萬人;12 月失業率為 4.1%,低於預期和 11 月的 4.2%;儘管平均時薪同比增速放緩,但整體增速仍較高。

美銀經濟團隊之所以認為這份報告 “關上了美聯儲降息的大門”,是因為美聯儲此前的貨幣政策重心此前已從抗通脹偏向穩就業,而最新的非農數據標誌着穩就業目標已經實現,意味着美聯儲沒有進一步降息的必要。

同時,由於當前的通脹水平仍高於 2% 的目標水平,對利率路徑的關注焦點將重新轉回通脹。因此該行推測,美聯儲下一步行動的風險更傾向於加息而不是降息。

該團隊還警告稱,2025 年將繼續是增長不平衡的一年,意味着政策的不確定性和分歧將會加劇。

美聯儲加息需要什麼條件?

美銀經濟團隊表示,當前的聯邦基金利率仍具限制性,要想關於加息的討論會提上日程,“門檻會很高”,可能需要核心 PCE 物價指數同比增速超過 3%+ 長期通脹預期失控。

最新數據顯示,美國 11 月 PCE 物價指數同比增 2.4%,為 7 月以來最高水平;核心 PCE 物價指數同比增長 2.8%,持平前值。

該行的利率團隊也發佈報告稱,隨着美聯儲加息可能性放大、美債市場供需失衡進一步加劇,美債收益率仍有上行空間。

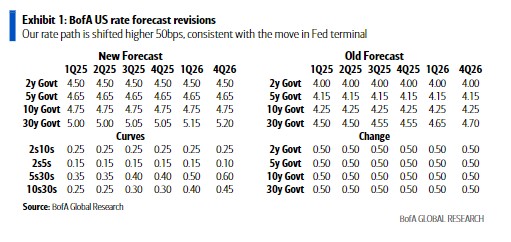

在報告中,該團隊將美債利率的預測區間全面上調 50 個基點,10 年期美債收益率的預期值被上調至 4.75%。

美銀利率團隊預計,如果 10 年期美債收益率在短時間內快速飆升(例如因通脹抬頭或財政赤字擴大引發市場動盪),可能會給美國經濟和股市帶來衝擊,並增加經濟衰退或滯脹的可能性。

該行的銀行團隊還補充稱,美債收益率水平的升高雖然一般會導致信貸質量逐漸惡化,但如果就業市場保持彈性且美國 GDP 增長在 2-3% 範圍內,預計信貸不會出現大範圍惡化。

該團隊預計,利率前景仍不明朗,預計接下來聯邦基金利率將將保持穩定或小幅走低,10 年期美債收益率則可能接近 5%。