How high will U.S. Treasury yields soar? Nomura: They may rise as high as 6% this year

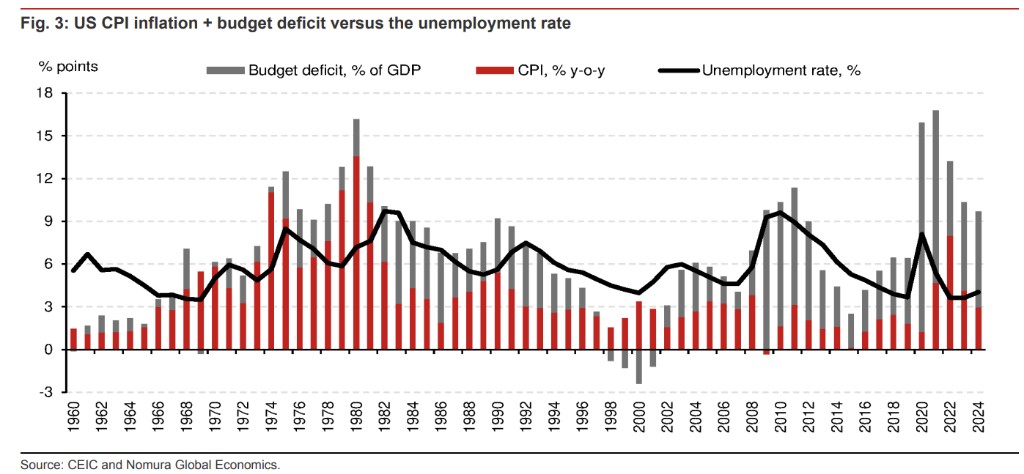

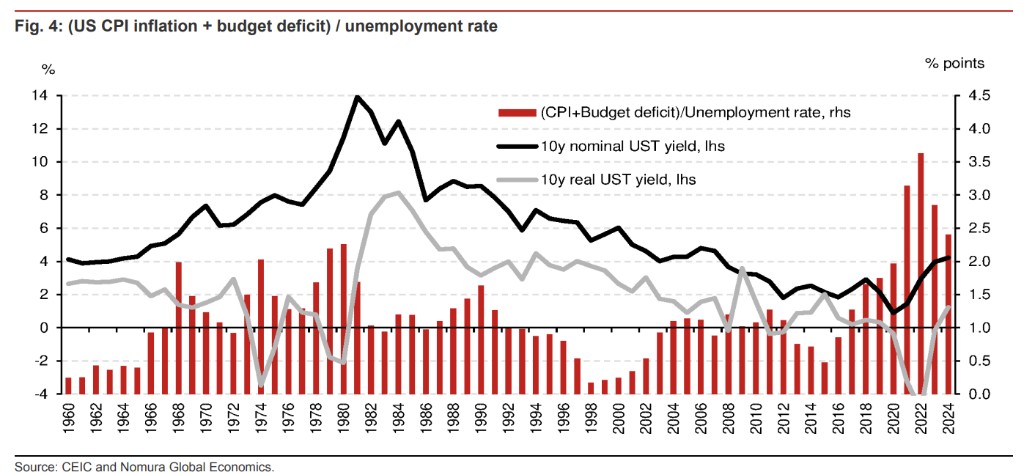

野村表示,從長期的歷史角度來看,10 年期美債收益率相對於 “CPI 通脹率” 和 “預算赤字” 這兩個主要驅動因素而言仍然偏低:當前,經週期調整的 “CPI 通脹率 + 預算赤字(佔 GDP 的比例)” 水平處於自 1960 年以來的最糟糕狀態。

通脹頑固、赤字高企的背景下,美債收益率還能飆多高?

1 月 17 日,野村分析師 Rob Subbaraman 和 Yiru Chen 發佈報告稱,從長期的歷史角度來看,10 年期美債收益率相對於 “CPI 通脹率” 和 “預算赤字” 這兩個主要驅動因素而言仍然偏低。目前美債收益率應當參照 20 世紀 80 年代或 90 年代,而非過去二十年。

野村解釋道,當前的 “CPI 通脹率 + 預算赤字(佔 GDP 的比例)” 水平是 2011 年以來最糟糕的,但是,2011 年美國還未完全走出全球金融危機的陰影,失業率超過 9%,導致貨幣和財政政策極度寬鬆。

因此,如果根據經濟週期調整(用失業率除以 “通脹率 + 預算赤字”),則結果顯示:當前,經週期調整的 “通脹率 + 預算赤字” 水平是自 1960 年以來最糟糕的。

此外,野村還表示,特朗普政策可能進一步利用美國作為全球儲備貨幣的優勢,而這也可能導致 10 年期美債收益率繼續上升。

然而,美國聯邦政府削減預算赤字的空間很小,再加上到期債務的再融資需求,可能導致今年美債發行總量達到 GDP 的 17% 左右。

在大量低息債券到期之際,美債收益率上升直接提高了政府的淨利息支出。此外,美聯儲的量化緊縮政策以及外匯儲備的調整(要麼降低美元配置,要麼賣出美債以進行匯市干預)可能導致官方對美債的購買力度不如以前強勁。

綜上所述,野村預計,10 年期美債收益率可能進一步飆升至 5-6%。

截止發稿,10 年期美債收益率報 4.6%。

1995-1996 年的情景重現

野村表示,10 年期美債收益率近期上升的最直接原因是美國經濟的韌性以及 “最後一英里” 的通脹挑戰,因為這限制了美聯儲進一步降息的空間,而這種經濟背景與美國 1995-1996 年的情況類似。

當時,核心個人消費支出通脹率略高於 2% 的目標,但失業率略有上升,且聯邦公開市場委員會的會議記錄顯示出對美國經濟衰退的擔憂。1995 年 7 月,美聯儲開始降息(從 6.00% 下調 25 個基點)。

儘管 5.75% 的實際政策利率依然較高,但美股市場表現強勁。最終,美聯儲僅在 1995 年 12 月和 1996 年 1 月分別降息了 25 基點,然後將利率維持在 5.25% 的水平長達 13 個月,並於 1997 年 3 月加息 25 個基點。