Why have Hong Kong stocks been performing weaker among the three markets recently?

Recently, the Hong Kong stock market has shown weak performance, attributed to factors such as reduced southbound capital flows, the arrival of the IPO lock-up period for Hong Kong stocks, concerns over interest rate hikes by the Bank of Japan, and expectations of interest rate cuts by the Federal Reserve. The short-term impact of liquidity is significant, and the downward trend in the credit cycle is exacerbating market volatility. Unless there are substantial policy adjustments, the credit cycle may continue to weaken, affecting market expectations and fundamentals

Many investors have recently asked a question: why are Hong Kong stocks particularly weak among the three markets of the US, Hong Kong, and A-shares?

Some explanations can be found in the funding situation: 1) The southbound capital has continued to shrink over the past few weeks, and the absence of Hong Kong stocks from the benchmark may lead to portfolio adjustments; in contrast, Hong Kong IPOs have not decreased at all, and the large stocks that went public in the first half of the year have all reached the six-month lock-up period; 2) Concerns about the Bank of Japan raising interest rates next week persist; 3) Although the Federal Reserve lowered interest rates this week, it is also seen as difficult to be dovish, resulting in US Treasury yields falling instead of rising, among other factors.

Indeed, liquidity has a short-term impact, especially on Hong Kong stocks that are more reliant on capital (along with structural issues related to the technology sector and the benchmark issues of domestic public funds). However, this is still not the long-term essence; conversely, it is precisely under the circumstances of poor fundamentals and incremental capital that these factors' disturbances are amplified. We have analyzed global liquidity in the context of new changes in liquidity, and simply put, short-term easing being reinforced is not "a sure thing." The Bank of Japan raising interest rates is not a systemic risk, but if the Federal Reserve adopts a hawkish stance on interest rates + next week's non-farm payrolls and CPI are both poor, then negative factors will converge, and the Bank of Japan raising interest rates will merely serve as a pretext and trigger, just like last August.

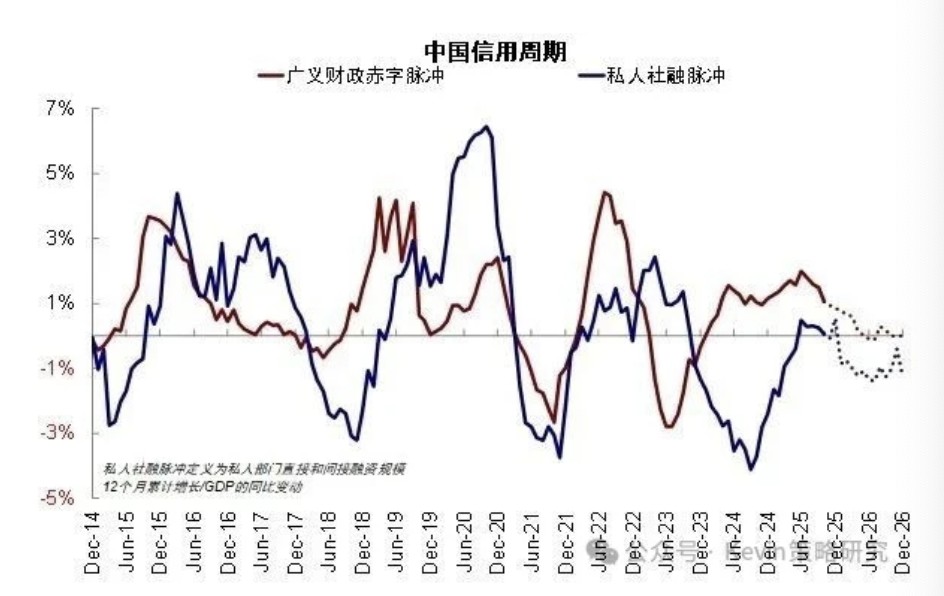

The key is still the downward turning point of the credit cycle, which has begun to appear since two months ago. We pointed out this point in our September report on the potential turning point of the US and China credit cycles, which is also the reason we have maintained our forecast of 26,000 for the Hang Seng Index this year without adjustment. However, at that time, the expectations were optimistic, so it was overlooked and masked.

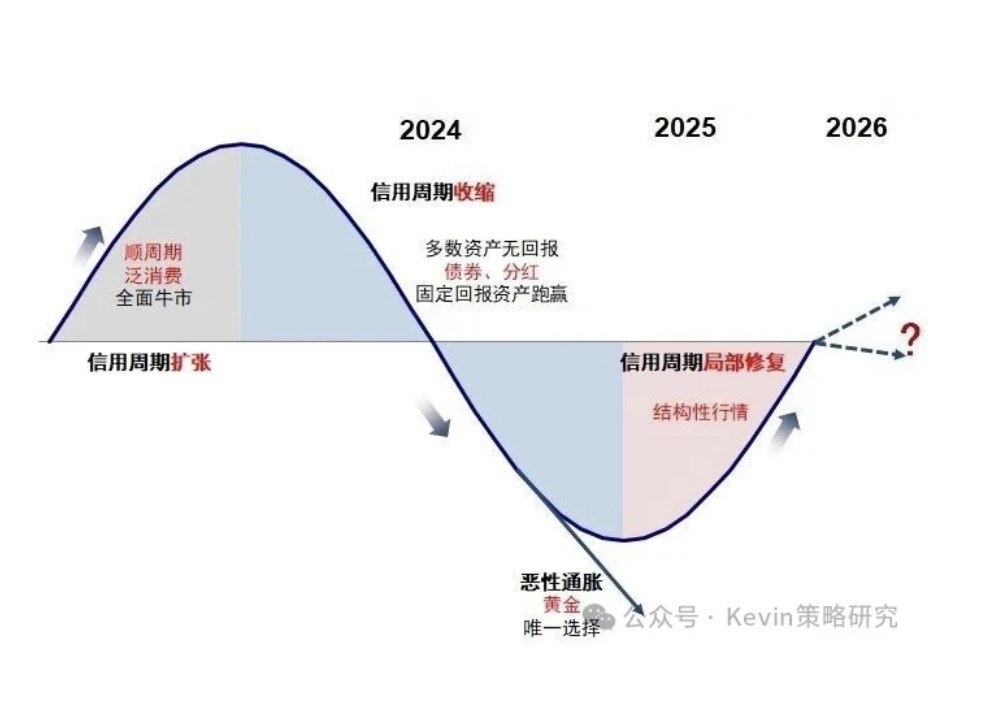

The credit cycle is a slow variable but will determine the central direction, especially when other factors (such as concerns about the AI bubble) and optimistic sentiment dissipate. Overall, unless there is a significant policy push, under issues such as high base numbers, income expectations, and inverted return costs, private credit and even the overall credit cycle are likely to trend towards fluctuations or even a phase of slowdown. The outlook for 2026: the next step of the "bull market."

Whether the market is entangled or the back-and-forth between dividends and technology, the essence is the current mismatch between fundamentals and expectations, which is also a direct reflection of the domestic credit cycle's weakening. On one hand, the high expectations for technology growth and high positions make investors sensitive to negative news, coupled with concerns about the AI bubble in the US stock market and the Federal Reserve's interest rate cut expectations. On the other hand, as candidates for "high cut low," domestic consumption and the real estate chain, although valuations and positions are attractive, the accelerating weakening of fundamentals makes it difficult to form a consensus. In our October report on gold, dividends, and growth, we pointed out that if policies cannot hedge in a timely manner, it will either lead to a phase of risk aversion or a return to a prosperous structure

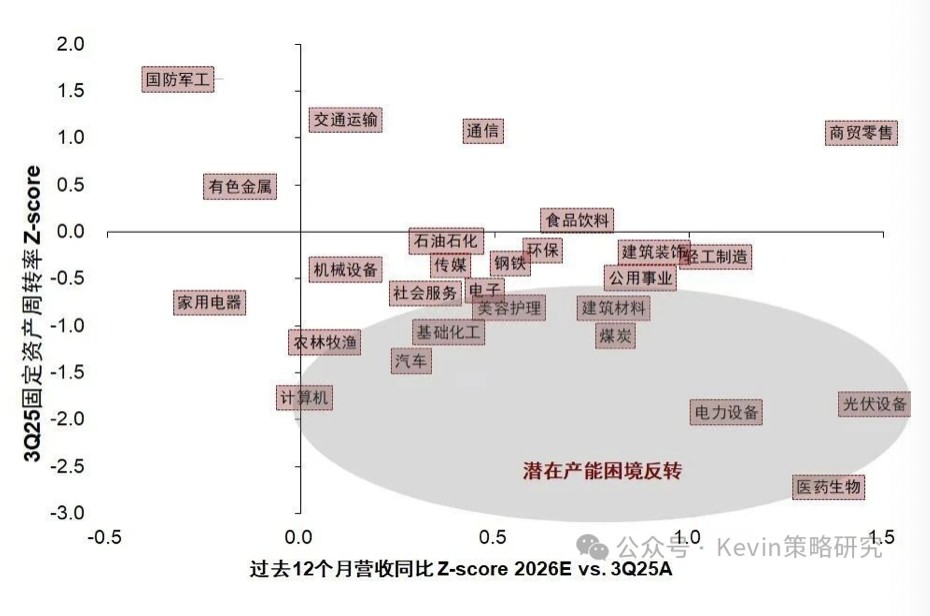

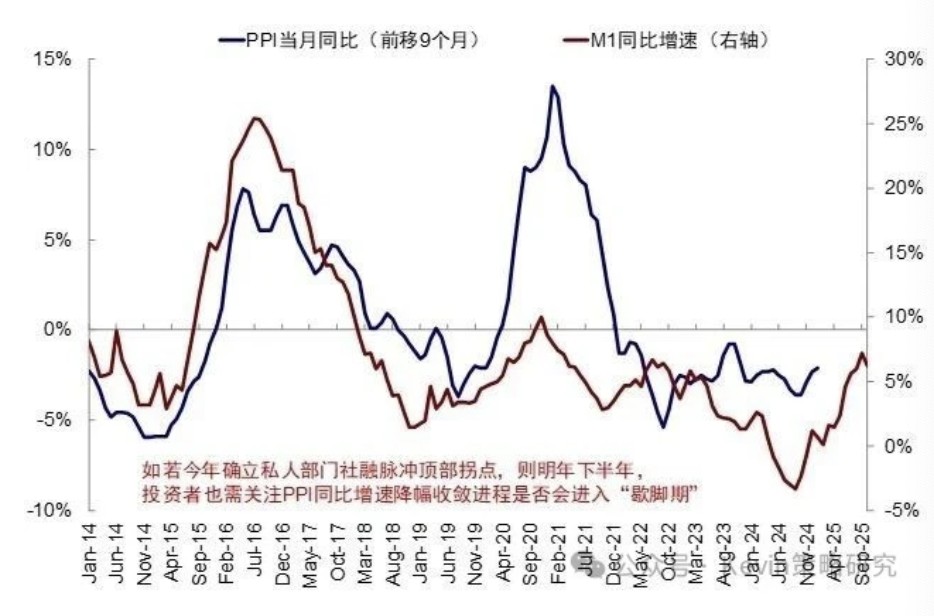

At first glance, it is highly likely that the short-term trend will continue unless the new chairman of the Federal Reserve adopts a more dovish stance and expands the balance sheet, or if the economic work conference exceeds expectations. Among the four major sectors: 1) AI requires new industrial catalysts (thus hardware visibility is greater than applications, with the former more prevalent in A-shares and the latter more in Hong Kong stocks), or liquidity catalysts (looking at the Federal Reserve); 2) Strong cycles, driven by U.S. fiscal and real estate demand in the first quarter and the rising window of domestic PPI; 3) General consumption, lacking fundamental support; 4) Dividends, hedging against the next stage of industry selection ideas as general consumption and credit cycles weaken.

Risk Warning and Disclaimer

The market has risks, and investment should be cautious. This article does not constitute personal investment advice and does not take into account the specific investment goals, financial conditions, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article are suitable for their specific circumstances. Investing based on this is at one's own risk