Goldman Sachs Quick Commentary on the Federal Reserve Decision: Not So "Hawkish" "Hawkish Rate Cut," Uncertainty for January

Goldman Sachs interprets the Federal Reserve's December interest rate meeting, believing that despite the widening internal voting disagreements and the upward adjustment of economic expectations, the overall decision was "not as hawkish as the market feared," and represents a successful risk management operation. Goldman Sachs pointed out that the policy statement restored the wording of "considering additional adjustments," indicating that the future interest rate path will rely more on data and does not close the door on further rate cuts, to which the market reacted positively

The Federal Reserve lowered interest rates by 25 basis points as expected at the December monetary policy meeting, marking its third consecutive rate cut.

According to Chasing Wind Trading Desk, on December 11, Goldman Sachs analyst Giulio released a report stating that despite the meeting seeing the most dissenting votes since 2019 and an upward revision of economic growth expectations, which carried a certain "hawkish" tone, the overall resolution tone was "not as hawkish as the market feared," successfully balancing risks and eliciting a positive market response.

The Federal Open Market Committee (FOMC) voted 9 to 3 to lower the target range for the benchmark interest rate to 3.5%-3.75%. The voting showed significant divergence, with members Schmid and Goolsbee favoring maintaining the interest rate, while Miran advocated for a larger cut of 50 basis points. The key policy statement restored the wording that the Federal Reserve would consider the "extent and timing of additional adjustments," marking a shift in policy focus towards a cautious assessment of future data and labor market risks.

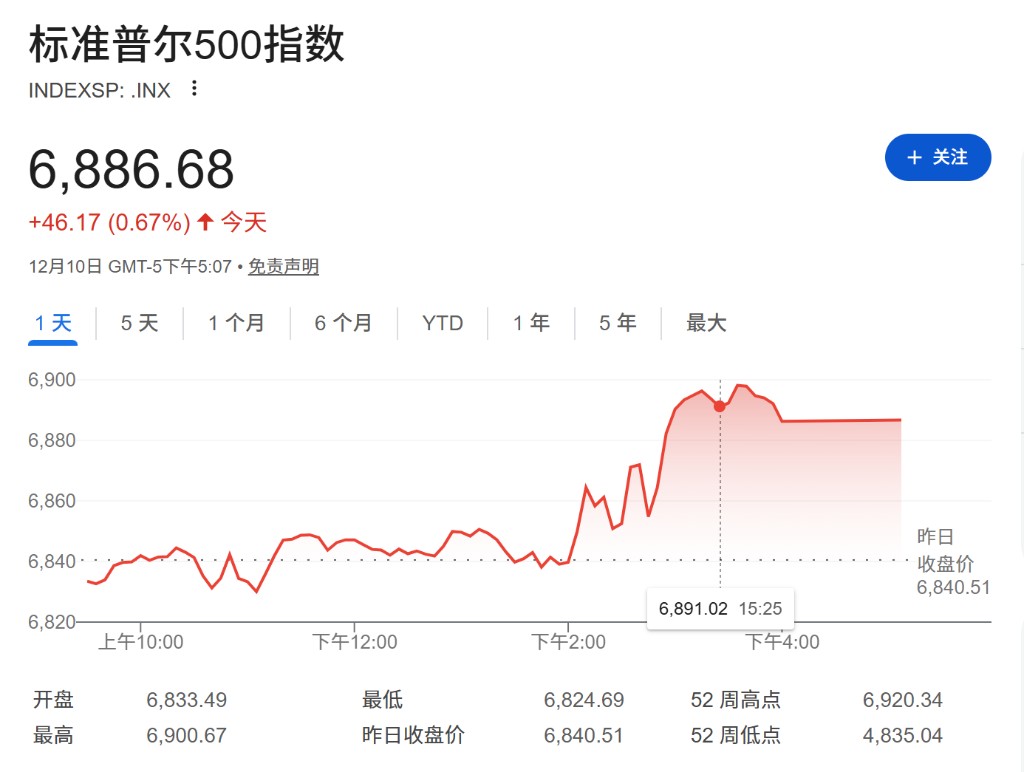

The market reacted positively, indicating that the Federal Reserve's operation was a successful "risk management" style rate cut. According to Bloomberg data, although investors held defensive positions before the meeting, following the announcement and Powell's speech, the S&P 500 index rose, while the dollar index and 2-year Treasury yield both fell to intraday lows.

Additionally, the Federal Reserve announced it would begin purchasing short-term government bonds starting December 12 to maintain ample reserve levels, a technical adjustment that also supported market sentiment.

Goldman Sachs pointed out that although Powell emphasized that there is "no risk-free path" for policy and did not provide clear signals for a pause or rate cut at the January meeting, the overall communication effectively soothed the concerns of both hawks and doves. The current policy path has not completely closed the door on further rate cuts, but future adjustments will depend more on the employment and inflation data in the coming weeks.

Divided Votes and "More Resilient" Economic Expectations

The most notable feature of this meeting was the widening divergence within the FOMC.

The 9 to 3 voting result showed that there is controversy within the committee regarding the policy path: in addition to Schmid and Goolsbee advocating for maintaining the interest rate, several members, including these two, expressed "soft dissent" in the dot plot forecast, indicating a preference for higher interest rates next year than expected.

According to the latest economic forecast summary, although the median in the dot plot remained unchanged, indicating one rate cut each in 2026 and 2027, there were six "soft dissent" opinions in the 2026 forecast, slightly leaning hawkish.

Meanwhile, the Federal Reserve raised its economic growth expectations for the coming years. The GDP growth forecast for 2026 was revised up from 1.8% to 2.3%, and for 2027 from 1.9% to 2.0% Goldman Sachs analysis believes that this reflects the resilience of consumer spending, the increase in AI capital expenditures, and the rebound after the impact of the government shutdown fades. In terms of inflation expectations, the core PCE inflation rate has been slightly revised down to 2.4% in 2026, and the unemployment rate is expected to peak in 2025.

“No Predefined Path” and the Fog of the Labor Market

At the press conference, Federal Reserve Chairman Jerome Powell reiterated the dual mandate and emphasized that due to the lack of incremental data, changes in employment and inflation expectations are minimal.

Regarding the wording of restoring “the degree and timing of additional adjustments,” Goldman Sachs interprets that after a cumulative rate cut of 75 basis points since September, the FOMC currently believes there is ample space to observe the situation, which suggests that the duration at this interest rate level may be extended in the future.

Powell clearly stated that no decisions have been made regarding the January meeting, and currently, no one is considering a rate hike as the baseline scenario. Future policy choices are not a binary risk of rate cuts and hikes, but rather a trade-off between “maintaining rates” and “the magnitude of rate cuts.”

Regarding the labor market, Powell pointed out that job growth may have been overestimated by about 60,000 (implying that the average monthly employment number may have actually decreased by 20,000 since April), and the current rate cuts are a reasonable response to rising unemployment and slowing job growth. He emphasized that there is “no risk-free path” between inflation and employment targets.

Restarting Bond Purchases to Maintain Ample Reserves

In addition to the interest rate decision, the Federal Reserve also announced an important balance sheet operation. The committee determined that bank reserve balances have fallen to “ample levels,” and therefore will begin purchasing short-term Treasury bonds starting December 12 (Friday) to maintain this level.

According to Goldman Sachs citing information from the New York Fed, these purchases will amount to approximately $40 billion per month. Combined with the $20 billion monthly reinvestment of mortgage-backed securities (MBS), the total amount of Treasury bonds purchased by the Federal Reserve in the coming months will reach about $60 billion per month.

The New York Fed noted that as the balance of the Treasury General Account (TGA) declines, the pace of purchases may slow after April. This move aims to ensure ample liquidity and avoid turmoil in the money market