Is the Federal Reserve restarting QE? RMP is here! The market wants to relive the "good memories of 2019"

美聯儲隔夜宣佈將根據需要開始購買短期美債,紐約聯儲同步公告計劃未來 30 天買入 400 億美元短期國債,儘管 RMP 並非 QE 但市場不在乎,美債、美股、比特幣、黃金和原油齊漲。美銀表示,根據 2019 年的經驗,流動性注入將迅速壓低擔保隔夜融資利率(SOFR),而聯邦基金利率(FF)的反應則相對滯後,這種 “時間差” 將為投資者創造顯著的套利空間。

上週華爾街見聞文章預測 “RMP” 將刷屏全市場,美聯儲本週如期宣佈啓動儲備管理購買(RMP)計劃,華爾街或將迎來了一場流動性注入盛宴。

據追風交易台,美聯儲隔夜宣佈,將根據需要開始購買短期國債以維持充足準備金供應。紐約聯儲同步發佈公告,計劃未來 30 天買入 400 億美元短期國債,這是自上週正式停止縮表後的最新動作。此舉出台背景是規模高達 12 萬億美元的美國回購市場近期出現令人不安的利率波動,貨幣市場持續動盪迫使美聯儲加快行動。

這一旨在維持充足準備金的舉措,儘管官方反覆強調"並非量化寬鬆",但市場已用實際行動投票:美債、美股、比特幣、黃金和原油齊漲,美元走弱,這是典型的 “量化寬鬆交易”,投資者正試圖重現 2019 年那場流動性盛宴的收益。

這一決定對短期融資市場的影響可能立竿見影。根據 2019 年的經驗,流動性注入將迅速壓低擔保隔夜融資利率(SOFR),而聯邦基金利率(FF)的反應則相對滯後,這種 “時間差” 將為投資者創造顯著的套利空間。

400 億美元月度購買拉開序幕

紐約聯儲週三發佈的公告詳細闡述了 RMP 的操作框架。根據 FOMC 的指示,紐約聯儲將通過在二級市場購買短期國債、必要時買入剩餘久期最多三年的國債來維持充足的準備金水平。這些購買規模將根據對美聯儲負債需求的預期趨勢以及季節性波動進行調整。

月度 RMP 金額將在每月第九個工作日左右公佈,同時還會公佈接下來約 30 天的暫定購買計劃。紐約聯儲交易台計劃於 12 月 11 日公佈首份計劃,屆時 RMP 的短期國債總額約為 400 億美元,將於 12 月 12 日開始購買。

紐約聯儲預計,為抵消明年 4 月非準備金負債預計大幅增加的影響,RMP 的購買將在未來幾個月內保持較高水平。此後,總購買速度可能會根據美聯儲負債的預期季節性變化而大幅放緩。購買金額將根據準備金供應前景和市場狀況進行適當調整。

FOMC 在聲明中表示:"委員會認為,準備金餘額已降至充足水平,並將根據需要開始購買短期國債,以此持續維持充足的準備金供應。"這一表述標誌着美聯儲資產負債表管理策略的重要轉折。

美聯儲主席鮑威爾表示,美聯儲本身並不"擔心"貨幣市場的緊張狀況,"我們知道這一天遲早會來,只是比預期來得快一些"。但美聯儲立即啓動國債購買計劃,並預計一段時間內購買量將"保持在高位",這表明官員們確實對流動性緊縮感到擔憂。

RMP 並非 QE,但市場不在乎

“量化寬鬆” QE 的主要目標是通過購買長期國債和 MBS 來壓低長期利率,以刺激經濟增長。而 RMP 的目的則更為技術性,專注於購買短期國債(T-bills),確保金融體系的 “管道” 中有足夠的流動性,防止發生意外。

儘管美聯儲和純粹主義者反覆強調 RMP 僅僅是調整而非 QE,但市場已經用"量化寬鬆交易"做出了回應。美銀利率策略團隊的最新報告與市場共識相似,該行確信大規模的流動性注入即將到來。

美銀此前預計,RMP 資金將由兩部分組成:一部分是自然資產負債表增長(Natural Growth),這是為了適應經濟體量和流通貨幣需求的自然擴張;一部分的 “回填”(Backfill),預計將持續 6 個月,用於修補前期流動性回籠可能造成的缺口。

美銀表示,相比於單純為了壓低長期利率或刺激經濟的 QE,RMP 更像是一種對銀行體系"管道"的維護。然而,對於短期融資市場而言,其實質影響就是直接的流動性注入。美銀認為,通過 RMP 注入的現金將迅速壓低 SOFR,但聯邦基金利率的反應會相對滯後,這種"時間差"創造了顯著的套利空間。

目前市場定價嚴重低估了這種流動性注入的風險。美銀認為 SOFR/FF 價差將從目前的-10bp 迅速回歸至-5bp 甚至更窄。這對投資者意味着前端利率市場存在明顯的交易機會。

2019 年劇本能否重演

為了理解即將發生的事情,美銀利率策略 Mark Cabana 團隊強調歷史只提供了一個真正具有參考價值的 RMP 案例,那就是 2019 年秋季。

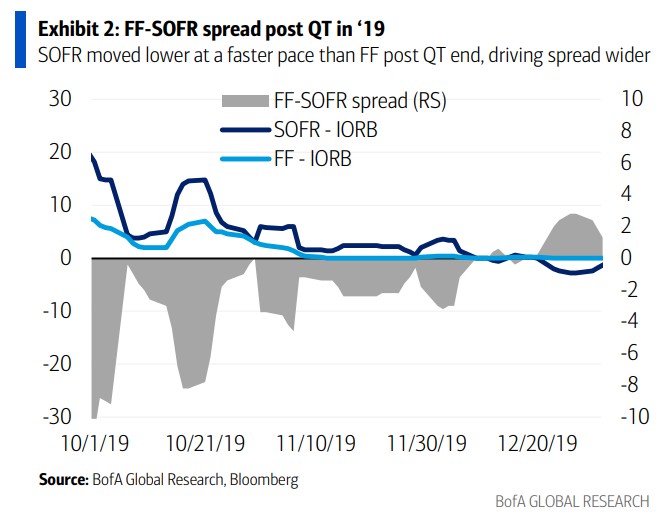

2019 年 9 月中旬,SOFR 突然飆升,顯示出系統內流動性極度短缺,即著名的回購危機。美聯儲迅速推出回購操作,並於 10 月 11 日宣佈、10 月 16 日開始執行 RMP。當時每月的 RMP 規模約為 GDP 的 0.2-0.3%,加上回購操作總計約為 GDP 的 1%。

市場反應立竿見影。流動性的注入推動 SOFR/FF 的價差從 9 月的-21bp 迅速收窄至 10 月的-3bp,並在 11 月進一步穩定在-2bp。2019 年的經驗表明,現金注入能極其迅速地推動 SOFR 變化,而聯邦基金利率則表現出滯後性。

美銀指出,雖然歷史韻腳相似,但 2025 年並非 2019 年的簡單重演。當前美聯儲的過度回籠情況並不像 2019 年那樣嚴峻,因此美聯儲此次的反應不會像 2019 年那樣劇烈。美銀預期的月度 RMP 規模約佔 GDP 的 0.15%,低於 2019 年的水平。

儘管力度較小,但邏輯傳導機制是一致的:現金增加推動 SOFR 迅速反應,而 FF 滯後。這種機制在 2021 年下半年也得到了驗證,當時美聯儲的 QE 推動 SOFR 比 FF 更快地跌向零值。無論官方如何定義,市場顯然已經準備好迎接新一輪的流動性盛宴。