The strongest storage upcycle in history? UBS: Expects DDR to rise 35% quarter-on-quarter, NAND shortage to last at least until Q3 next year

UBS data shows that the storage industry is facing an unprecedented supply-demand tension. In terms of DRAM, the supply shortage is expected to last until the first quarter of 2027, with DDR demand growing by 20.7%, far exceeding supply growth. The NAND shortage is expected to continue until the third quarter of 2026. UBS expects that DDR contract pricing in the fourth quarter is expected to increase by 35% quarter-on-quarter, and NAND prices are expected to rise by 20%, with this round of price increases far exceeding previous expectations

With the ongoing supply shortage, the storage market is entering the strongest price increase cycle in history.

According to the Chasing Wind Trading Desk, the latest report from UBS's Nicolas Gaudois team shows that the storage industry is facing an unprecedented supply-demand tension. In terms of DRAM, the supply shortage is expected to last until the first quarter of 2027, with DDR demand growing by 20.7%, far exceeding the supply growth. The NAND shortage is expected to continue until the third quarter of 2026.

This will lead to the strongest storage price increase cycle in nearly 30 years. UBS expects that in the fourth quarter of this year, DDR contract pricing is expected to increase by 35% quarter-on-quarter, and NAND prices will rise by 20%, with this round of price increases far exceeding previous expectations. In the first quarter of 2026, DDR contract pricing will further increase by 30%, and NAND prices will rise by 20%.

Customers are actively locking in long-term supplies, and large cloud service providers have extended their pre-purchase orders to 2028. Despite all parties making efforts to procure, customer inventory levels have not significantly increased, with server DDR inventory maintained at 11 weeks, PC and mobile DRAM at 9 weeks, and SSD at a low of 8 weeks. This indicates strong actual demand rather than speculative hoarding driving up prices.

Unprecedented Supply Shortage: NAND at least until Q3 next year, DRAM continuing until the year after next

UBS data shows that the storage industry is facing unprecedented supply-demand tension. In terms of DRAM, the supply shortage is expected to last until the first quarter of 2027, with DDR demand growing by 20.7%, far exceeding the supply growth of 18.6%. The NAND shortage is expected to continue until the third quarter of 2026.

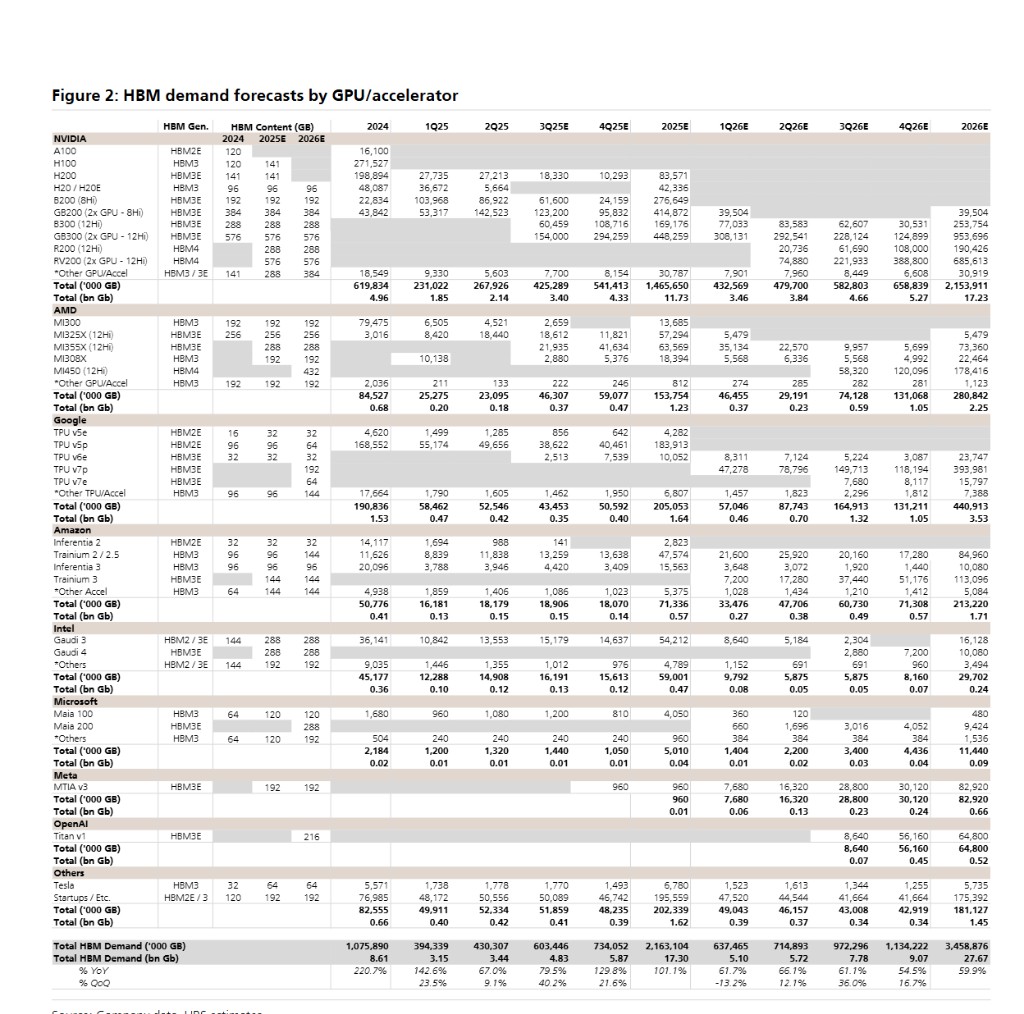

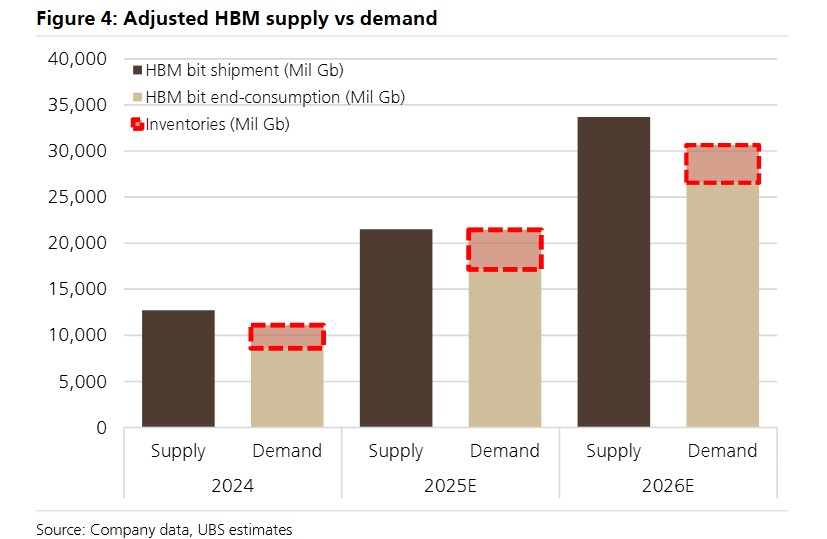

The surge in demand for AI servers has become one of the driving factors. UBS expects that server shipments will grow by 12.9% to 18.1 million units in 2026, with AI servers having a lower proportion but significantly increased unit storage capacity. HBM (High Bandwidth Memory) demand continues to explode, with demand expected to reach 27.67 billion Gb in 2026, a year-on-year increase of 59.9%.

Demand in traditional application areas is also strong. The storage configuration of terminal devices such as smartphones and PCs continues to upgrade, while the digital transformation and cloud computing demand in the server field provide stable growth momentum for the storage market.

To Ensure Supply, Customers are Locking in Long-Term Contracts

In the face of supply tightness, customer procurement strategies have fundamentally changed. Large cloud service providers are signing pre-purchase orders (PPO) extending to 2027 or even 2028 to ensure long-term supply security. These agreements lock in supply volumes but do not lock in prices, leaving room for suppliers to increase prices.

At the same time, PC and smartphone manufacturers are facing increased procurement risks. Compared to cloud service providers with stronger bargaining power, traditional OEM manufacturers are more vulnerable to price fluctuations UBS analysts pointed out that even though double-digit quarter-on-quarter price increases may intuitively be difficult to sustain until the second, third, and fourth quarters of 2026, customers may still need to accept price increases to ensure supply continuity.

Inventory data further confirms the tightness of supply and demand. The storage inventory levels of various customers remain relatively low, with server DDR inventory at about 11 weeks, mobile and PC DRAM at about 9 weeks, and SSD at about 8 weeks. This indicates that the current price increases are not driven by speculation, but rather reflect the real supply and demand relationship.

The reshaping of the industry landscape is imminent, who will be the biggest winner?

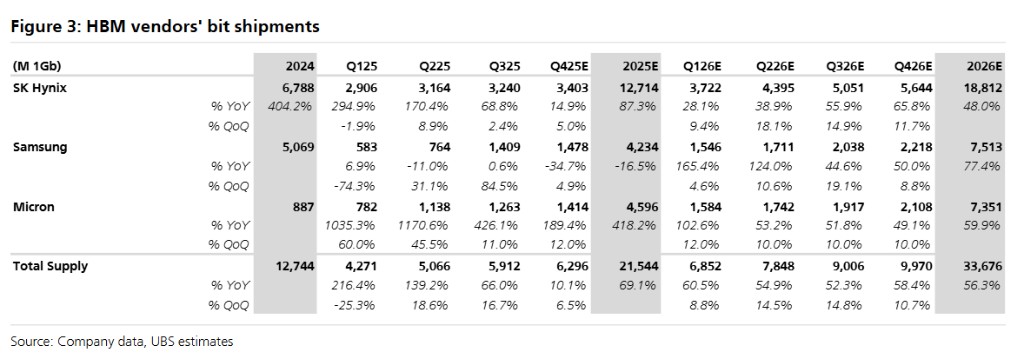

The report indicates that the competition landscape in the HBM market is relatively stable, with SK Hynix expected to continue holding about 70% of the HBM4 market share. In the new generation Rubin architecture, SK Hynix is expected to become the main supplier. At the same time, the company may also become the preferred HBM3E supplier for Google TPU 7p, with Samsung as the second supplier.

UBS has significantly raised the target prices for major storage manufacturers: SK Hynix from 710,000 KRW to 853,000 KRW, maintaining a key buy rating; Samsung Electronics from 128,000 KRW to 154,000 KRW, maintaining a buy rating; Nanya Technology from NT$140 to NT$190, with the rating upgraded from neutral to buy.

The upward demand for traditional servers provides support for the entire storage industry. According to Dell'Oro data, server procurement volume in the third quarter of 2025 is expected to grow by 41.8% year-on-year, with a 27.3% increase in the first nine months. This trend is expected to continue, providing a stable profit foundation for storage manufacturers