Is the Bank of Japan's interest rate hike in December a done deal? Nomura: An interest rate hike is highly likely, the key is the terminal rate and the future pace of rate hikes

Nomura Securities believes that after the interest rate hike in December, the focus has shifted to Ueda's statements on the neutral interest rate and hints about the future path of interest rate hikes. Ueda may maintain the view that "real interest rates are very low" or "still far below the neutral interest rate even after the rate hike," which means that no dovish signal indicating the end of rate hikes will be issued. Attention should be paid to whether the wording "raise the policy interest rate based on improvements in economic and price developments" is removed. If removed, it should be interpreted as a hindrance to further rate hikes

The Bank of Japan's monetary policy meeting in December is approaching, and the market has priced in about a 90% probability of a rate hike to 0.75% in December. Nomura Securities believes that a rate hike in December is almost a foregone conclusion, and the focus has shifted to how Governor Kazuo Ueda will convey the future rate hike path, particularly regarding the terminal rate level and the pace of rate hikes.

On December 11, according to news from the Wind Trading Desk, Nomura Securities stated in its latest research report that due to the absence of an economic outlook report in December, Ueda's remarks on the neutral rate and hints about the future rate hike path will become the market's focus.

The firm expects Ueda to emphasize that "real interest rates are still very low," which means that no dovish signals indicating an end to rate hikes will be issued. Regarding the neutral rate, Ueda may keep his statements vague to maintain policy flexibility. Nomura particularly emphasized that if the Bank of Japan removes the wording "raise the policy rate based on improvements in the economy and prices," it would imply that additional rate hikes are hindered.

The latest survey shows that 90% of economists predict that the Bank of Japan will raise rates by 25 basis points at the meeting on December 18-19, and the market has fully digested a very aggressive rate hike path, with rates expected to rise to 1.0% before September 2026, and terminal rate expectations as high as 1.5%.

However, Nomura believes that even considering the expansion of the economic stimulus plan and the recent depreciation of the yen, this meeting is unlikely to release a more hawkish rate hike pace or higher terminal rate signals than what the market has already digested. The firm maintains that the timing for raising rates to 1.0% should be in January 2027, rather than the market's priced-in September 2026.

December Rate Hike is No Longer in Doubt

Nomura clearly pointed out that the Bank of Japan will raise the policy rate from 0.50% to 0.75% at the monetary policy meeting in December. This judgment is based on Ueda's clear statements in his speech on December 1 — the central bank is "laying the groundwork for a rate hike in December," mainly for the following reasons:

Shunto Wage Negotiations: The central bank has grasped the preliminary trends of the 2026 wage negotiations.

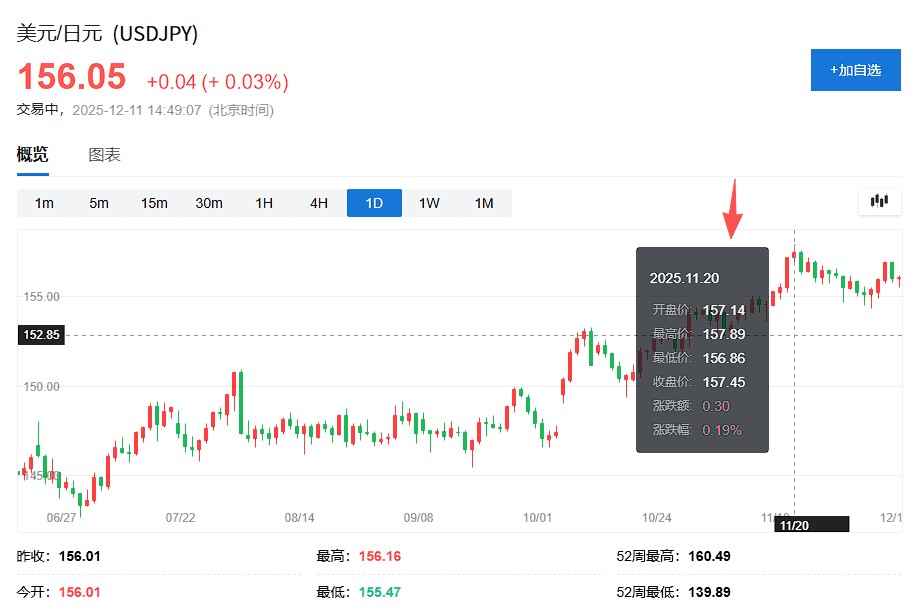

Exchange Rate Inflation Transmission: Ueda has clearly expressed concerns about the potential impact of the exchange rate on underlying inflation. On November 20, the yen briefly fell below 157 against the dollar, which clearly triggered the central bank's nerves.

At the same time, the shift in political winds has become an important variable supporting the rate hike. According to reports, due to concerns about the excessive depreciation of the yen, Finance Minister Shunichi Suzuki's originally aggressive stance on fiscal expansion may be weakening.

Suzuki has not only shifted to accepting rate hikes, but the voices within the government advocating for aggressive fiscal expansion seem to be dwindling. In discussions on tax reform for the fiscal year 2026, the Liberal Democratic Party did not propose any significant tax cuts. According to government officials, Suzuki has stopped making overly ambitious demands for the initial budget for the fiscal year 2026 Nomura believes that since the market has priced in about 90% of the interest rate hike possibility, unless there is severe turmoil in the financial markets on the eve of the meeting that forces the central bank to hesitate, the interest rate hike is a foregone conclusion.

Policy Communication Becomes a Key Variable

Considering that a rate hike in December is almost certain, the real focus after this rate hike will be how Governor Kazuo Ueda manages market expectations through the press conference. Nomura expects that Bank of Japan Governor Kazuo Ueda may signal in two aspects:

Qualitative Aspect, Ueda may maintain the view that "real interest rates are very low" or "still far below the neutral rate even after the rate hike," which means no dovish signal indicating that rate hikes are about to end will be issued.

Quantitative Aspect, the Bank of Japan's estimated natural interest rate range for 2024 is between -1% and +0.5%. Assuming the expected inflation rate stabilizes at 2%, the corresponding nominal neutral interest rate should be in the range of 1% to 2.5%. Ueda may express some views based on the latest data but will also remain vague to allow for flexible adjustments based on subsequent data.

Nomura points out that media reports and institutional forecasts suggest that the estimates of the natural interest rate are rising, and the Bank of Japan may raise its lower estimate of the neutral interest rate from the current 1.0%.

Regarding the terminal interest rate, Nomura Securities notes that the current market pricing is quite aggressive. The "one-year interest rate two years from now," which serves as a proxy indicator for terminal interest rate expectations, has risen to 1.49%, and the overnight index swap for September 2026 is at 0.9875%, indicating that the market is fully pricing in a rate increase to 1.0% before September 2026.

Nomura's economic team believes that this expectation may be overly hawkish, as even considering fiscal stimulus and yen depreciation, inflation and economic activity in 2026 will not significantly overshoot.

Regarding the future pace of rate hikes, Nomura believes that unlike the October meeting, the central bank will not link rate hikes to specific events such as the "Shunto," but will emphasize that rate hikes will continue as long as the economy and prices meet expectations.

Nomura insists that the timing for raising rates to 1.0% should be in January 2027, rather than the market pricing of September 2026, which means the market is overpricing the future rate hike magnitude.

The research report also specifically mentions that investors should pay attention to whether the Bank of Japan removes the wording "raise the policy interest rate based on improvements in economic and price developments." This wording was added in May to address the risks of U.S. tariffs, and if removed, it should be interpreted as a reduction in additional rate hike obstacles.