Goldman Sachs raises its copper price forecast for 2026, citing "the delay in U.S. copper tariffs, leading to a larger non-U.S. gap."

高盛將 2026 年銅價預測上調至 11400 美元/噸,預計美國銅關税將推遲至 2027 年實施,這意味着美國在 2026 年會繼續以溢價囤積銅,從而加劇非美市場的供應短缺並主導定價。分析師警告,當前銅價已包含極度擁擠的投機多頭和對 AI 數據中心概念的過度樂觀,若關税提前或市場情緒逆轉,價格將面臨顯著回調風險。

高盛關鍵修正 2026 年銅價預測至 11,400 美元/噸,核心邏輯在於美國關税 “時間差” 引發市場結構性割裂——全球銅市從統一市場分裂為 “美國囤貨市場” 與 “非美短缺市場”。

據追風交易台,12 月 16 日,高盛在最新報告中指出,美國針對精煉銅的關税不太可能在 2026 年上半年立即實施(原基本情景),而是會推遲到 2027 年。這種推遲引發了一個關鍵的市場結構變化:美國將繼續通過溢價囤積銅,導致 “非美國市場” 的銅供應出現比預期更嚴重的短缺。

- 價格支撐邏輯改變: 銅價的定價權正日益轉移到 “非美市場的供需平衡” 上。僅僅看全球總庫存已不足以判斷價格,必須關注美國以外的庫存緊張程度。

- 短期做多,中期警惕:儘管基本面(非美缺口)支撐 11,400 美元的價格,但目前的銅價(約 11,700 美元)已經包含了極其擁擠的投機性淨多頭倉位,且與 AI 數據中心概念高度綁定。一旦關税政策與其基準假設不符(如提前實施)或 AI 情緒降温,銅價面臨劇烈的回調風險。

預測調整:非美市場的庫存 “黑洞” 不僅在持續,還在擴大

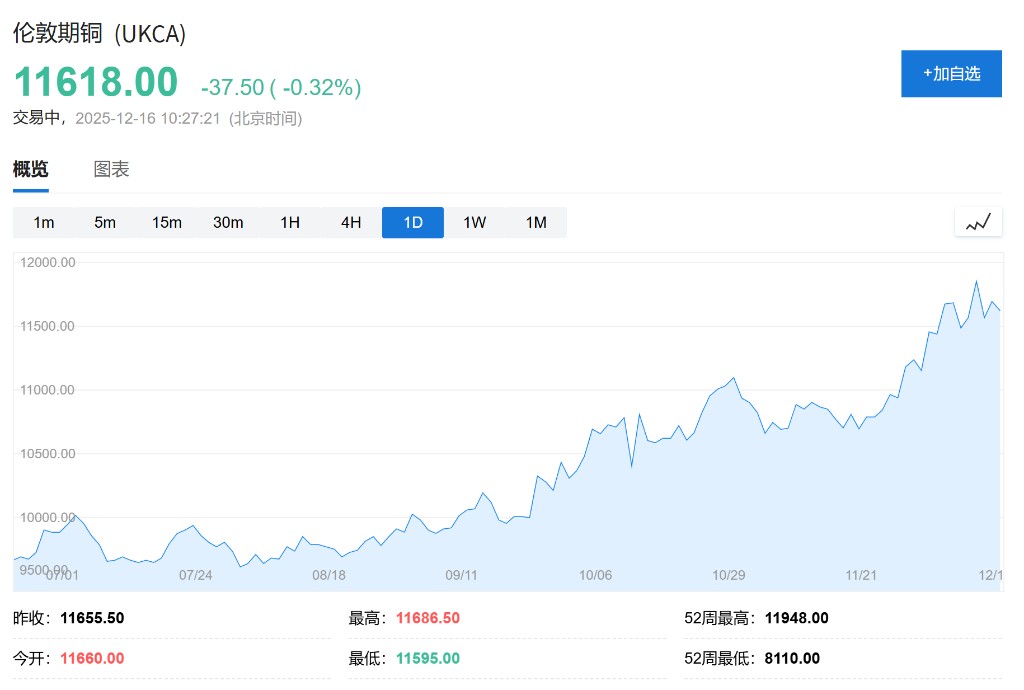

高盛明確指出,LME 銅價在 12 月 12 日創下了 11,952 美元的歷史新高,年初至今漲幅達 33%。

基於新的關税時間表假設,高盛調整了價格模型:

2026 年預測上調:從 10,650 美元/噸上調至 11,400 美元/噸。

2027 年預測維持:保持在 10,750 美元/噸不變(預計屆時關税落地,全球庫存水平重新成為焦點,價格將回落)。

非美市場的決定性作用:高盛認為,由於美國的銅庫存實際上處於 “被鎖定” 狀態,銅價主要由非美市場的平衡決定。

量化模型:根據歷史迴歸分析,庫存消費天數每下降 1 天,LME 銅價(同比年度均價)將上漲約 1.4%。

高盛預計,2026 年非美市場的銅庫存將減少約 45 萬噸,這將允許美國市場在同一年累庫 75 萬噸。這種極度的不平衡是支撐高盛上調銅價的核心算術基礎。

關税博弈:推遲實施 = 美國繼續 “虹吸” 全球銅資源

高盛大幅調整了對美國關税政策落地的概率預測,這是本次研報的 “勝負手”:

- 新基準情景(55% 概率):2026 年上半年宣佈關税,但推遲至 2027 年實施(預計起徵點為 10%,2028 年升至 30%)。

- 原基準情景(降至 25% 概率):2026 年上半年直接實施關税。

- 完全擱置(20% 概率):2026 年無公告,關税被無限期擱置。

為何推遲?高盛認為,考慮到 “負擔能力” 和限制對美國企業造成的干擾,當權者更傾向於給予緩衝期。參考案例是 12 月 9 日對尼加拉瓜的關税決定,該決定雖已宣佈,但要到 2027 年才生效。

延遲實施的市場後果:只要關税是 “未來的威脅” 而未即刻落地,美國國內銅價相比 LME 就會保持溢價,驅動美國繼續囤貨。對於非美市場而言,這等同於供給收緊。如果關税提前在 2026 年上半年落地(25% 風險概率),美國囤貨將停止,LME 價格將面臨快速回調。

全球供需:看似過剩,實則短缺

一個反直覺的數據是,高盛實際上上調了 2026 年全球市場的過剩預期,但依然看漲銅價。

- 全球過剩上調:將 2026 年全球精煉銅過剩量從 16 萬噸上調至 30 萬噸。

- 原因:高銅價刺激了約 10 萬噸的額外廢銅收集,並導致約 4 萬噸的需求因鋁的替代效應而減少。

- 非美缺口擴大:儘管全球總賬是過剩的,但由於美國不僅吸納了所有過剩量還額外囤積,導致非美市場的赤字從 2025 年的約 25 萬噸,擴大到 2026 年的約 45 萬噸。

這就是高盛看漲的邏輯閉環:全球過剩是假象,非美市場的實物短缺才是定價的真相。

風險警示:極度擁擠的交易與 AI 敍事的脆弱性

儘管基本面支持 11,400 美元的均價,但高盛非常嚴肅地警告了當前的下行風險。目前約 11,700 美元(截至 12 月 15 日)的市場價格已經略高於高盛的基本面估值。

投機倉位見頂:銅的投機性淨多頭倉位已接近歷史最高水平,市場極度擁擠,任何風吹草動都可能引發踩踏。

AI 數據中心的 “幻覺”:銅價近期走勢與 AI 數據中心概念股(如電力基礎設施、半導體等)高度相關。

數據驗證:2025 年數據中心確實貢獻了全球銅需求增量的 26%(儘管其總量只佔銅消費的 1%),這得益於建設速度的爆發式增長。

預期差:市場目前的定價隱含了未來幾年數據中心需求將持續爆發。但高盛認為,除非建設速度在當前高位上再 “上一個台階”,否則 2026-2027 年來自數據中心的銅需求增量將非常有限。

投資者需要警惕市場對 AI 基礎設施建設的過度樂觀情緒,這種情緒的逆轉可能成為銅價回調的催化劑。