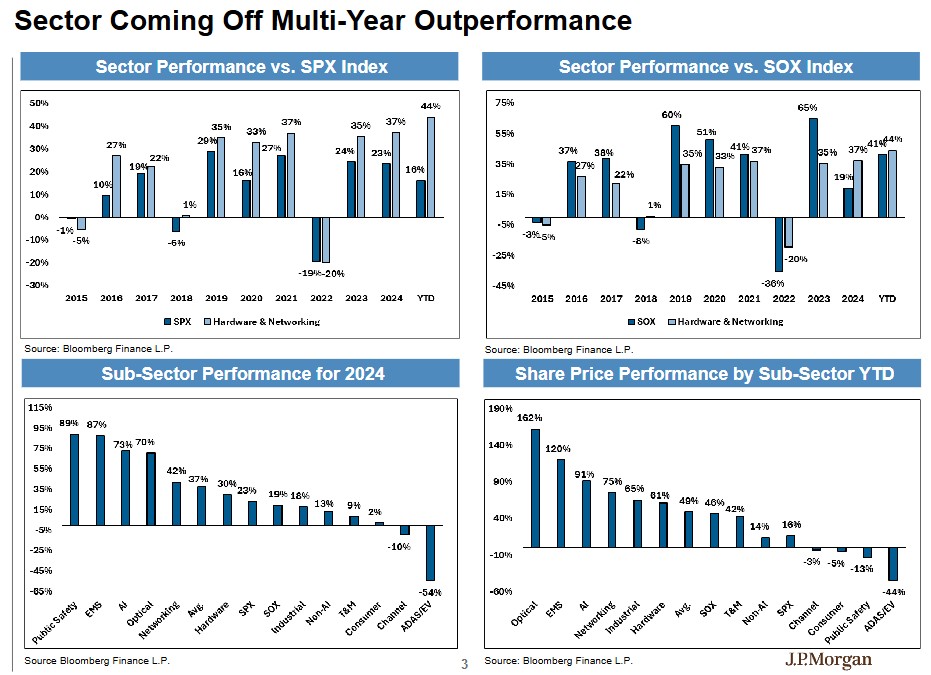

"Hold on to AI winners firmly, don't rotate"! JP Morgan's hardware team: By 2026, "network" growth will surpass "computing power"

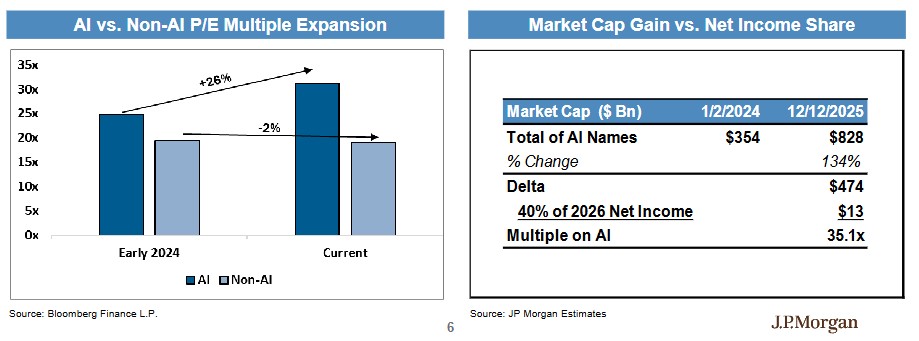

JP Morgan pointed out that the current valuation premium of AI-related companies in the US stock market is only 26%, while AI can actually bring about 60%-80% profit growth. Therefore, investors should stick to holding AI winner stocks. JP Morgan believes that the network infrastructure sector will outperform computing power next year, and expects AI switch revenue to grow by 48% in 2026, far exceeding the overall data center switch industry's 23%

In the face of the recent pullback in AI hardware stocks, JP Morgan's hardware team has sent a clear signal: investors should stick with AI winner stocks rather than engage in large-scale rotation. More importantly, the team expects that the growth of the "network infrastructure" sector will surpass "computing power" by 2026, providing investors with a new opportunity window.

According to the Wind Trading Desk, JP Morgan's hardware and network research team stated in their latest 2026 outlook that the valuation premium of AI-related companies in the U.S. stock market is only 26%, which means investors are overly conservative in their expectations for AI-driven profit growth. The team anticipates that, based on company guidance, AI could actually bring about a 60%-80% acceleration in profit growth, far exceeding the current market pricing of a 26% increase.

"Investors do not need to rotate out of AI leading companies but should focus on adjusting weights and rankings," said Samik Chatterjee, head of hardware research at JP Morgan, in the report. The team maintains Arista Networks, a U.S. cloud network solutions provider, and Amphenol, a leader in connectors, as their preferred stocks, and expects profit increases in 2026 to be the main driver of stock prices.

Investment Strategy After Recent Pullback: Hold Rather Than Rotate

After the recent pullback, the JP Morgan team believes it is a good opportunity to reassess AI portfolios but recommends a strategy of "holding" rather than "full rotation."

Analysis shows that the current valuation premium for AI-related companies is about 26%, which is relatively conservative. The team estimates that AI business will account for about 40% of these companies' revenues by 2026, corresponding to a price-to-earnings ratio of about 35 times, indicating that the market only expects sustainable capital expenditure growth related to AI to be 30%, far below the 70% growth rate for 2024-2025.

"Early company outlooks show that AI brings an average long-term revenue growth increase of 400 basis points and an average profit growth increase of 600 basis points," the report noted. This means that for industries previously thought to have only mid-single-digit growth, the actual growth acceleration brought by AI is close to 60%-80%.

More critically, capital expenditures for 2026-2027 have already been locked in. Recent announcements regarding data center construction provide clear visibility for early 2026 and 2027, with expected capital expenditures for hyperscale vendors and secondary cloud service providers growing by 52% and 45%, respectively, in 2026.

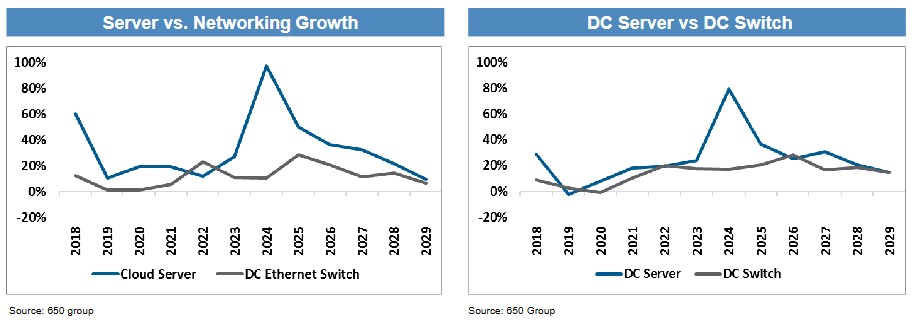

Network Catching Up to Computing Power: A Structural Shift is Happening

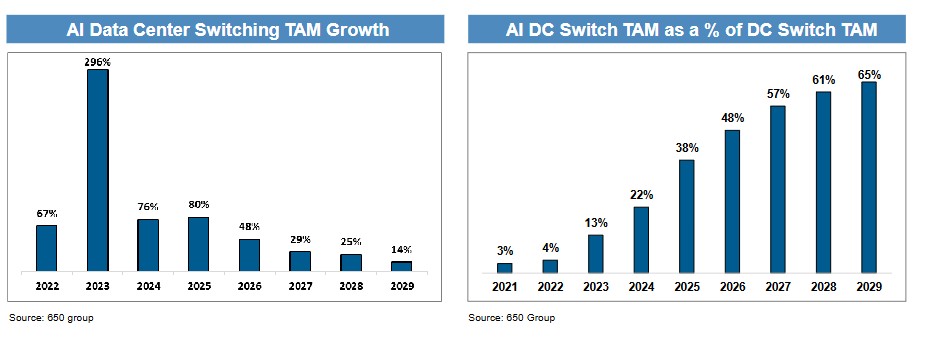

One of the core views of the JP Morgan team is that the growth of the network infrastructure sector is about to catch up with and surpass the growth of computing power, and this structural shift will redefine the AI investment landscape The report cites a forecast from research firm 650 Group, predicting that AI switch revenue will grow by 48% in 2026, 29% in 2027, and 25% in 2028. In contrast, the overall growth rates for the data center switch industry are projected to be 23%, 19%, and 18%, respectively. This indicates that AI is becoming the main driver of growth in the switch industry.

"As GPU cluster sizes expand, the additional ratio of computing power required by network devices continues to rise," Chatterjee explained. Data shows that the revenue from AI data center switches is expected to jump from 4% of the total switch market in 2022 to 57% by 2027.

The driving factors behind this trend include: the demand for larger cluster sizes, the urgent need for optimized GPU utilization, and the upgrade from 800G to 1.6T technology. At the same time, network architecture is shifting from scale-out to scale-up, with the latter expected to become a more significant growth engine by 2030.

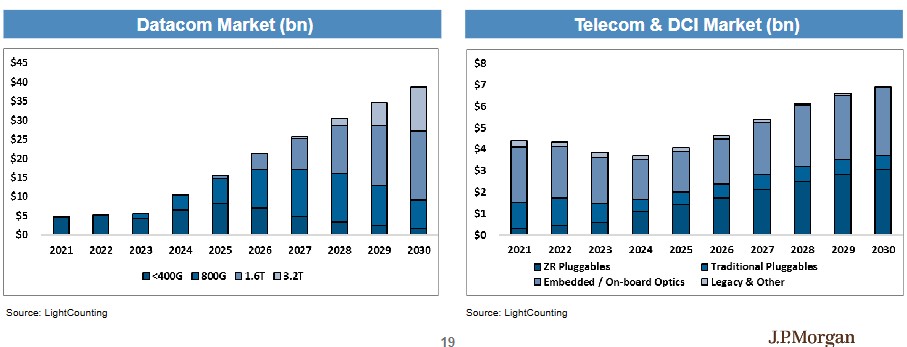

In the optical interconnect field, the data communication market is expected to grow by 40% to $20 billion by 2026, maintaining a compound annual growth rate of 20% before 2030. The telecom and data center interconnect market is also projected to grow by about 15% to $5 billion by 2026.

Based on these trends, JP Morgan has placed network-related companies high on its recommended list, while its participation in pure computing power companies is relatively limited. Arista and Amphenol are the top picks, followed by companies like Celestica, Coherent, and Lumentum.

Focus on Supply Chain Risks

Despite the optimistic outlook, the JP Morgan team also pointed out challenges expected in 2026. Supply chain constraints are anticipated to become a key topic of discussion each quarter, with major bottlenecks including HBM memory, CoWoS packaging, and capacity limitations for optical components.

High Bandwidth Memory (HBM) is sold out at major suppliers until 2026, and the broader memory market is also tightening. NAND and DRAM prices have increased year-on-year by 185% and over 300%, respectively, which will have differentiated impacts on various hardware categories.

Driven by geopolitical factors, manufacturing capacity is rapidly shifting to the Americas. The share of EMS (Electronic Manufacturing Services) companies' capacity in the Americas is expected to rise from 29% in 2022 to 35% in 2024, a trend that is expected to continue JP Morgan maintains an optimistic outlook on the investment prospects for AI infrastructure, expecting that the capital expenditure of hyperscale vendors' data centers will exceed $150 billion in 2026, setting a new historical high. At the same time, secondary cloud service providers and emerging cloud companies will also become important growth drivers, with their capital expenditure expected to reach approximately $80 billion in 2026.

For investors, the key lies in identifying companies that can benefit from structural changes in network infrastructure growth that outpace computing power, and positioning themselves at the current relatively conservative valuation levels