CICC's trillion yuan merger "kickoff"

CICC absorbs and merges Dongxing and Cinda, outlining a new trillion-yuan brokerage profile with share exchange pricing and structural arrangements

On the evening of December 17th, CICC disclosed a significant announcement.

The major asset restructuring plan of the three brokerages "CICC + Dongxing + Cinda" was officially unveiled, revealing a "brokerage aircraft carrier" with assets close to one trillion yuan, and the relevant transaction details were presented to the market for the first time.

How the price is determined, how the shares are exchanged, who chooses to stay, and who can exit—these seemingly technical arrangements constitute the core clues that the market is currently most concerned about.

CICC's latest response to Wall Street Insights·Finance House: After the merger, CICC will not only see its asset scale, business scale, and revenue scale rise to the forefront of the industry, but will also form a comprehensive service system covering "institutional and retail," "international and domestic," significantly enhancing its ability to withstand cyclical fluctuations.

Beyond the announcement, what is truly worth dissecting is the logic and trade-offs hidden behind these arrangements.

Share Exchange Price Determined

According to the transaction plan, the pricing for this transaction is based on the average price of the last 20 trading days prior to the announcement of the board resolutions of all parties, with CICC as the surviving entity in the absorption merger.

The exchange price is set at 36.91 yuan/share, the exchange price for the absorbed Dongxing Securities is 16.14 yuan/share, and the exchange price for Cinda Securities is 19.15 yuan/share.

The plan also emphasizes that "this transaction scheme fully reflects the asset value of the two companies and is conducive to balancing the interests of all shareholders."

This statement may seem highly technical, but it holds significant practical meaning in major restructurings.

Using the average price of the last 20 trading days as the pricing benchmark means that the exchange price is anchored to existing market prices, rather than expectations of future synergy effects.

More importantly, this mechanism establishes a price bottom line that can be mutually accepted among shareholders with different backgrounds.

CICC, Dongxing Securities, and Cinda Securities are backed by a diverse group of major shareholders.

Public information shows that CICC's main shareholders include Central Huijin Investment Ltd. and Hong Kong Securities Clearing Company Ltd.;

Dongxing Securities' shareholder structure includes China Orient Asset Management Co., Ltd., Jiangsu Railway Group, Shanghai Industrial Investment Group, and Chengtong Holdings Group, among others;

The main shareholder of Cinda Securities is China Cinda Asset Management Co., Ltd., along with institutions such as Shenzhen Qianhai DreamWorks Operating Co., Ltd. and Zhongtian Jintou Co., Ltd.

It is worth noting that after penetrating the equity structure of the three brokerages mentioned above, they are all companies controlled by Central Huijin Investment Ltd., effectively representing three brokerages "merging into one" under the same actual controller.

Potential "Premium"?

Finance House noticed that there is a detail in this transaction plan that truly differentiates the parties, namely the share exchange ratio itself.

The announcement disclosed that the share exchange ratios for Dongxing Securities and Cinda Securities with CICC's A-shares are 1 to 0.4373 and 1 to 0.5188, respectively.

This means that, as absorbed parties, the number of CICC shares that each share of Cinda Securities can be exchanged for is significantly higher than that of Dongxing Securities. According to Dongfang Caifu: Before the suspension, the market values of Dongxing Securities and Cinda Securities were 42.4 billion yuan and 57.7 billion yuan, respectively, with total shares of 3.232 billion and 3.243 billion.

At least from the results, Cinda Securities obtained a higher share exchange ratio.

CICC recently stated to Zhitang: CICC has accumulated industry-leading professional capabilities in investment banking, private equity investment, institutional business, and international business, while Dongxing Securities and Cinda Securities have a solid foundation in regional layout and retail clients, and possess relatively ample capital. The three parties form a complementary advantage and efficient allocation.

CICC's "New Plate"

One statement in this announcement that has attracted attention is: Dongxing Securities and Cinda Securities will participate in the share exchange with all their A-shares. Based on this calculation, CICC expects to issue approximately 3.096 billion new A-shares.

This can be translated as: CICC is not using cash to buy the two companies, but rather using its newly issued shares to settle the transaction. The scale of the settlement is the addition of 3.096 billion shares.

To determine whether these 3.096 billion shares are significant, we need to look at them in the context of CICC's existing share capital.

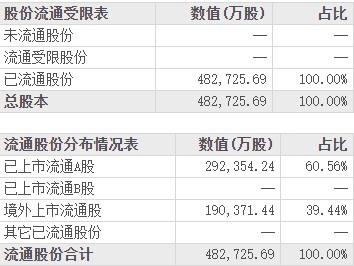

According to Dongfang Caifu, before the completion of this merger, CICC's total share capital was approximately 4.827 billion shares. Among them, about 2.924 billion shares were listed and circulating A-shares, and about 1.904 billion shares were listed and circulating in Hong Kong.

After the completion of this merger transaction, CICC's share capital "base" will change to approximately 7.923 billion shares, equivalent to a one-time expansion of about 64%.

At this point, this is merely a "rough calculation."

More importantly, since all of the newly issued 3.096 billion shares are A-shares, the proportion of CICC's A-shares in the total share capital will increase from about 60% before the merger to approximately 76% after the merger.

For ordinary investors, this change can be understood as: CICC's "plate" not only becomes larger, but the weight of A-shares significantly increases.

This raises a question worth observing in the capital market:

After the merger is completed, will CICC's stock price performance, valuation center, and market sentiment further increase their dependence on the A-share market?

How Small and Medium Shareholders "Exit"

In this merger plan, in addition to the price and share exchange ratio, another arrangement that directly relates to individual investor decisions is the exit mechanism for small and medium shareholders.

The transaction plan discloses: To protect the rights and interests of small and medium investors, dissenting shareholders of CICC's A-shares and H-shares can exercise their right to request a buyback, while dissenting shareholders of Dongxing Securities and Cinda Securities will have the option for cash.

The so-called right to request a buyback can be understood simply as if you hold CICC's stock, and vote against this absorption merger, you can request to have your shares repurchased at the specified price after meeting the legal conditions. Cash Option is more intuitive. If you hold shares of Dongxing Securities Co., Ltd. or Cinda Securities and do not wish to exchange them for shares of CICC, you can choose to take cash directly and exit, rather than passively participating in the share exchange and becoming a new shareholder of CICC.

The transaction plan also states: Major shareholders including Central Huijin, China Orient, and China Cinda have issued long-term commitments, locking their shares of CICC obtained or originally held in this transaction for 36 months.

This is a lock-up commitment from the major shareholders.

In simple terms: After the merger is completed, CICC's capital scale will significantly expand, and the market's biggest concern is the pressure brought by the concentrated release of new shares. Locking for 36 months means temporarily "withdrawing" this core and significant portion of chips from the secondary market, rather than viewing it as a phase of arbitrage.

Which Other Brokerages Are "Joining In"

In this absorption merger, the ones truly in the spotlight are CICC, Dongxing Securities Co., Ltd., and Cinda Securities, but the advancement of the transaction is not just a matter between the three parties.

(As shown in the image above) Zhi Shi Tang noticed a detail in the announcement: CICC, as the absorbing party, has hired Industrial Securities as an independent financial advisor; Dongxing Securities Co., Ltd. and Cinda Securities have hired Guotou Securities and Bank of China Securities as independent financial advisors for the absorbed party.

In simple terms: the role of "independent financial advisor" in major asset restructuring is equivalent to the "compliance gatekeeper" in a complex transaction.

Financial advisors do not help either party "negotiate a higher price," but rather stand on the position of the companies they serve to answer: Is this transaction fair to our shareholders? Does the pricing logic comply with regulatory rules, etc.?

In this brokerage merger, CICC chose Industrial Securities, essentially providing compliance justification for its share pricing, capital expansion, and overall structure after the merger; while Dongxing and Cinda brought in Guotou Securities and Bank of China Securities respectively to ensure that the asset value of the absorbed party's shareholders is reasonably reflected in the share exchange process.

"Trillion-Yuan Brokerage Aircraft Carrier"

If we pull the timeline back to the third quarter report of 2025, the merger concept of CICC, Dongxing Securities Co., Ltd., and Cinda Securities has become quite clear, with a brokerage platform that is larger and more capable emerging.

From the individual financial performance perspective, CICC achieved operating income of 20.761 billion yuan in the first three quarters of this year, with a year-on-year growth rate of 54.36%; net profit attributable to the parent company was 6.567 billion yuan, a year-on-year increase of 129.75%. As of the end of the third quarter, the company's total assets amounted to 764.941 billion yuan, continuing to rank first in the industry.

For Dongxing Securities Co., Ltd., the operating income in the first three quarters was 3.610 billion yuan, a year-on-year increase of 20.25%; net profit attributable to the parent company was 1.599 billion yuan, a year-on-year increase of 69.56%, with total assets at the end of the period amounting to 116.391 billion yuan Cinda Securities achieved an operating income of 3.019 billion yuan during the same period, a year-on-year increase of 28.46%; the net profit attributable to shareholders was 1.354 billion yuan, a year-on-year increase of 52.89%, with total assets reaching 128.251 billion yuan.

If the third-quarter report data of the three brokerages is placed on the same balance sheet for calculation, the total assets of the merged brokerage platform will exceed 1009 billion yuan, with a combined net profit attributable to shareholders of nearly 10 billion yuan in the first three quarters, and the core scale indicators overall entering the forefront of the industry.

In terms of total assets, the merged entity of "CICC + Dongxing + Cinda" can rank fourth in the current securities industry, only behind CITIC Securities, Guotai Junan, and Huatai Securities.

If compared based on net profit attributable to shareholders, the merged "CICC + Dongxing + Cinda" will rank behind CITIC Securities, Guotai Junan, Huatai Securities, China Galaxy, and GF Securities, entering the top six in the industry.

The change in personnel scale is also of reference significance. According to the 2024 annual report data, CICC, Cinda Securities, and Dongxing Securities have employee numbers of 14,523, 2,792, and 2,670 respectively, totaling 19,985 employees.

This scale has surpassed Guotai Junan, Huatai Securities, CITIC Jianan, and China Galaxy during the same period, closely approaching CITIC Securities, which has over 20,000 employees, ranking at the forefront of the second tier in the industry.

From this set of aligned data, it can be seen that this is not simply a matter of volume accumulation, but rather the embryonic form of a comprehensive brokerage platform that possesses significant competitiveness in terms of asset scale, profitability, and organizational scale