Wall Street comments on Micron's financial report: Performance guidance is too "explosive," but the market is concerned about a pullback in HBM prices next year

Micron's financial report and guidance "exploded," with revenue and gross margin significantly exceeding expectations. Morgan Stanley stated that, apart from NVIDIA, this could be the largest revenue and net profit guidance upgrade in the history of the U.S. semiconductor industry. Although AI demand will keep supply and demand tight until 2026, Wall Street is concerned that next year's competitor capacity release may trigger a pullback in HBM prices

Micron Technology's latest financial report and performance guidance exceeded Wall Street's expectations, but institutions still have slight differences regarding the sustainability of the future cycle: bulls believe this is a historic turning point in profitability, while the cautious faction is beginning to worry that with increased supply, high bandwidth memory (HBM) prices may see a pullback in 2026.

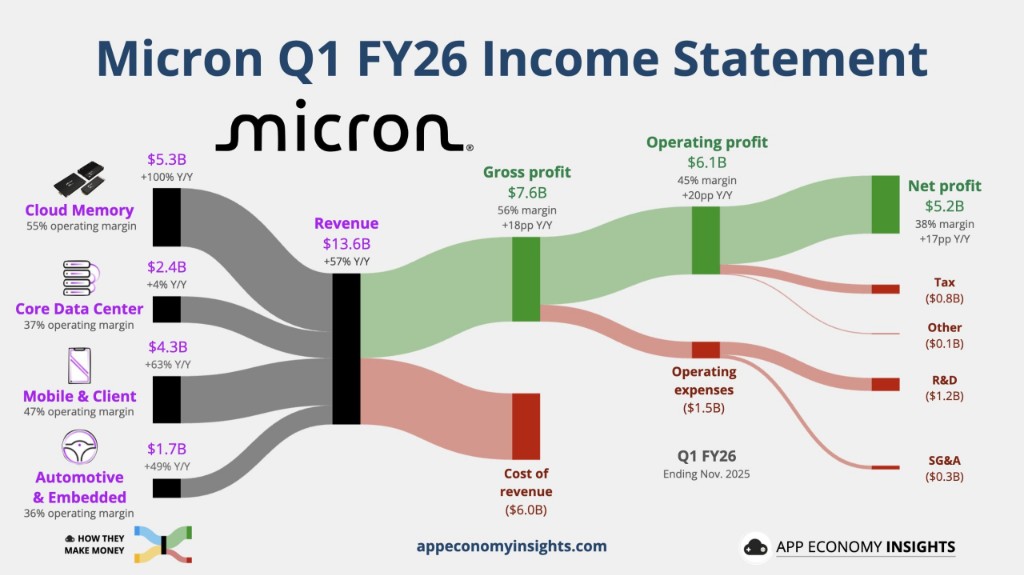

According to news from the Wind Trading Desk, in the recently announced performance guidance, Micron expects revenue for the next fiscal quarter to reach $18.7 billion, a figure far exceeding the market's general expectation of $14.5 billion; at the same time, the company expects non-GAAP gross margin to soar to around 68%, significantly higher than analysts' expected 55%, marking a historic leap in profitability. In terms of quarterly performance, Micron also comprehensively exceeded expectations, with its profitability rapidly recovering driven by significant increases in DRAM and NAND prices.

This "explosive" performance guidance immediately triggered a strong reaction on Wall Street, with several institutions quickly raising their target prices. Morgan Stanley believes that, aside from NVIDIA, the revenue and net profit revisions provided by Micron are nearly unprecedented in the history of U.S. semiconductor stocks. Barclays stated that due to the improvement in the pricing environment, this is an anticipated but astonishingly large "breakout quarter." The market consensus is that the structural demand brought by AI is reshaping the supply-demand landscape of the storage industry, and the tight supply situation will last at least until 2026.

However, amidst the general optimism, concerns about mid-term price trends still exist. Although Goldman Sachs has significantly raised its profit expectations, it maintains a "neutral" rating, with its core concern being that as competitors like Samsung release capacity, the HBM market may face price downside risks in 2026.

Performance guidance far exceeds expectations, gross margin approaches 68%

The core highlight of this financial report is that the forward guidance provided by management significantly exceeded Wall Street's conservative models. Morgan Stanley's Joseph Moore analysis team pointed out in a report on the 18th that Micron's earnings per share (EPS) guidance for the next quarter is about 75% higher than the market consensus, with the median non-GAAP EPS guidance reaching $8.42, while the market previously expected only $4.78. The analysts at this institution stated, aside from NVIDIA, this may be the largest revenue and net profit guidance revision in the history of the U.S. semiconductor industry.

Barclays' Tom O'Malley team emphasized in their report that this is a "breakout quarter." Although the market had anticipated recent price dynamics, the magnitude of this performance exceeding expectations is still shocking. The guidance indicates that gross margin will reach 68%, with further improvement expected in the coming quarters. This suggests that with the support of long-term agreements (LTA), the pricing environment will continue to improve In addition, the average selling prices (ASP) of DRAM and NAND continue to rise due to supply constraints. Barclays' model shows that Micron's DRAM ASP is expected to increase by 30% quarter-over-quarter next quarter, while NAND is expected to increase by 40%.

Capital Expenditure Raised to $20 Billion, Capacity Shortage to Persist

In response to the market's high concern regarding capital expenditure (Capex) plans, Micron announced an increase in its net capital expenditure for fiscal year 2026 from the previous $18 billion to approximately $20 billion.

Morgan Stanley interprets this positively, believing that this figure is actually "below market concern levels." Analysts point out that the increased expenditure is primarily for building cleanroom facilities and supporting capacity for HBM and 1-gamma processes, but this does not mean that there will be a large influx of mature wafer supply into the market in the short term. Management revealed that the No. 1 wafer fab in Idaho will not produce wafers until the first half of 2027, which means that the supply shortage situation for the entire year of 2026 will be difficult to alleviate.

Barclays added that management expects the potential market size (TAM) for HBM to grow at an annual compound growth rate (CAGR) of about 40%, reaching $100 billion by 2028. Micron is committed to enhancing supply capacity, but this supply tightness will negatively impact consumer markets such as PCs, as capacity is prioritized for the high-margin AI and data center sectors.

Goldman Sachs Maintains "Neutral" Rating, Concerned About HBM Price Pullback Next Year

Despite such strong earnings reports, Goldman Sachs has chosen to maintain a "neutral" rating and has not been as aggressively bullish as other institutions. Analyst James Schneider's team raised the target price from $205 to $235 and acknowledged Micron's excellent execution in HBM products, expecting it to capture about 20% of this high-growth market.

However, Goldman Sachs' core concern lies in the pricing environment for 2026. Analysts believe that the current risk-reward ratio is relatively balanced. Although the current DRAM market is healthy and NAND supply is tight, as more suppliers (such as Samsung) validate and release capacity, there may be a risk of HBM price pullback in 2026. The firm stated that it would only consider a more constructive stance on the stock when it sees the entire industry maintaining disciplined supply growth in 2027.

Nevertheless, based on the company's far better-than-expected revenue and gross margin assumptions, Goldman Sachs has raised its non-GAAP earnings per share expectations by an average of 97%.

Morgan Stanley Reiterates "Preferred Stock," Target Price Raised to $350

In contrast, Morgan Stanley maintains an extremely optimistic stance, raising the target price from $338 to $350 and reiterating Micron as its "preferred stock" in the U.S. semiconductor sector.

Morgan Stanley believes that the memory chip industry is entering "unknown territory," with pricing not only showing no signs of decline but becoming more certain under multiple long-term contracts. Analysts point out that as long as the wave of AI continues, Micron will continue to benefit over the next 12 months, with its profitability expected to exceed the $40 mark. Regarding valuation concerns, Morgan Stanley counters that despite the rise in stock price, considering the company could generate $30 billion to $35 billion in free cash flow over the next year and that its book value could double, the current valuation is actually undervalued Barclays also gave an "overweight" rating, raising the target price from $240 to $275. Its optimistic view is based on structural changes in the storage industry, believing that Micron will continue to benefit from improved operating models before supply shortages ease. The optimistic scenario target price set by Barclays could even reach $325, provided that HBM growth is faster and the pricing environment is better than expected