Is the buying point for U.S. Treasuries approaching?

Recently, U.S. Treasury yields have risen, mainly influenced by expectations of improved fundamentals, the impact of Trump’s policies, and the erosion of the Federal Reserve's independence. Looking ahead, although the first quarter may face pressure, we are optimistic about the downward space for U.S. Treasury yields throughout the year, expecting the Federal Reserve to cut interest rates 3-4 times, with the 10-year yield potentially falling to 3.5%. Before the Spring Festival, the strong renminbi may benefit domestic institutions in increasing their holdings of U.S. Treasuries

Recently, the rise in U.S. Treasury yields is attributed to a comprehensive range of negative factors including expectations of improved fundamentals, the impact of Trump, damage to the Federal Reserve's independence, seasonal weaknesses, and the drag from Japanese bonds. After these factors have fully played out, it will be difficult to add further negative pressure.

The main background includes:

① A pause in rate cuts, with the Federal Reserve entering an observation period;

② A shift in the market's macro narrative towards recovery and inflation, with commodities surging;

③ The frequent emergence of extreme policies from Trump, affecting geopolitics (Venezuela, Greenland), the economy (buying MBS for the two housing agencies, credit card interest rate controls), and the Federal Reserve (criminal investigation into Powell), reminiscent of last April's "Liberation Day" mini-version;

④ The weakness of Japanese bonds spilling over, dragging down overall developed market government bonds;

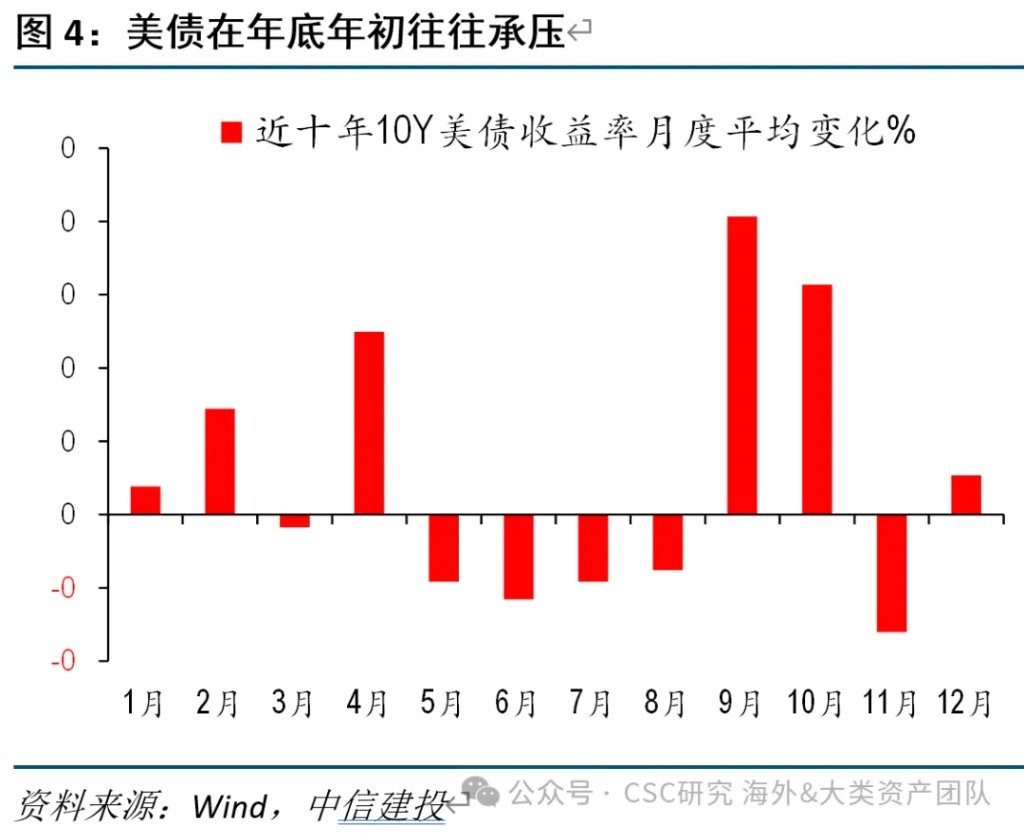

⑤ Seasonal disadvantages at the beginning of the year, with the Christmas-New Year period historically favoring stocks over bonds.

Looking ahead, there is considerable room for U.S. Treasury yields to decline within the year. After the recent dual pressures on interest rates and exchange rates are released, buying opportunities will arise, particularly from after the Spring Festival to March:

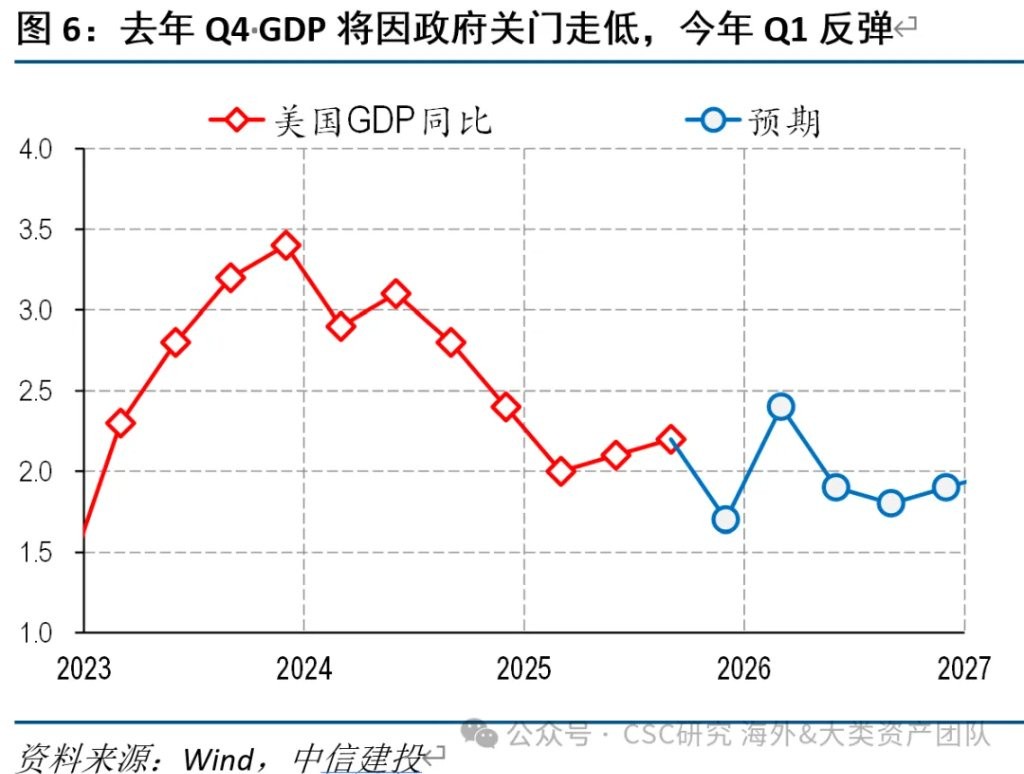

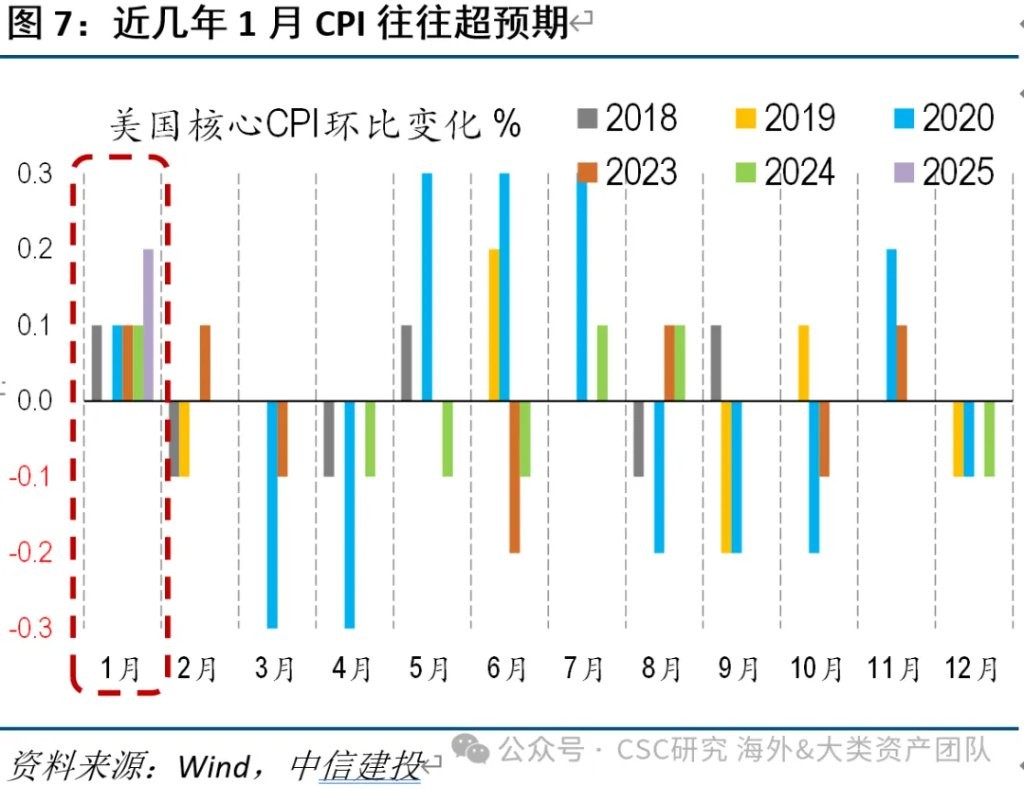

① The first quarter may still face pressure. A government shutdown could lower Q4 growth, with a potential rebound in Q1. CPI is expected to habitually exceed expectations in January, and short-term data cannot disprove recovery and inflation, while Trump's unpredictable behavior continues to cause disturbances.

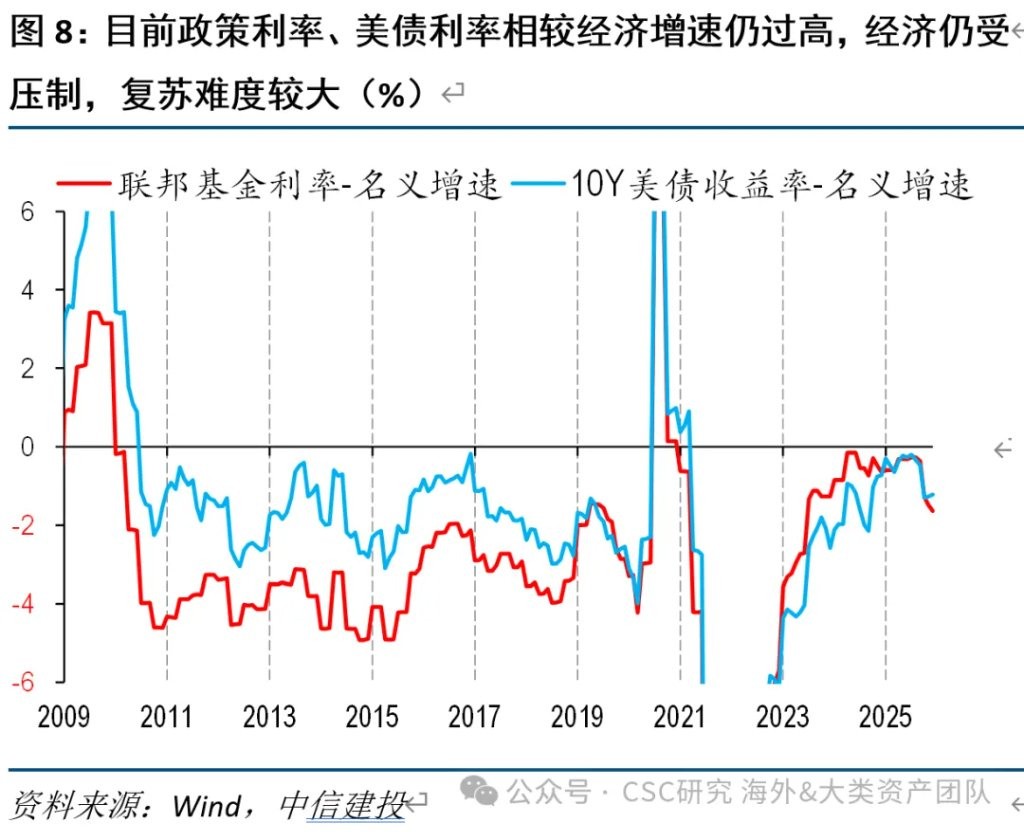

② However, the outlook for the entire year remains positive. Current interest rates are still too high and do not match the recovery narrative; the economy is expected to decline further, with the Federal Reserve likely to cut rates 3-4 times, bringing the 10-year yield down towards 3.5%.

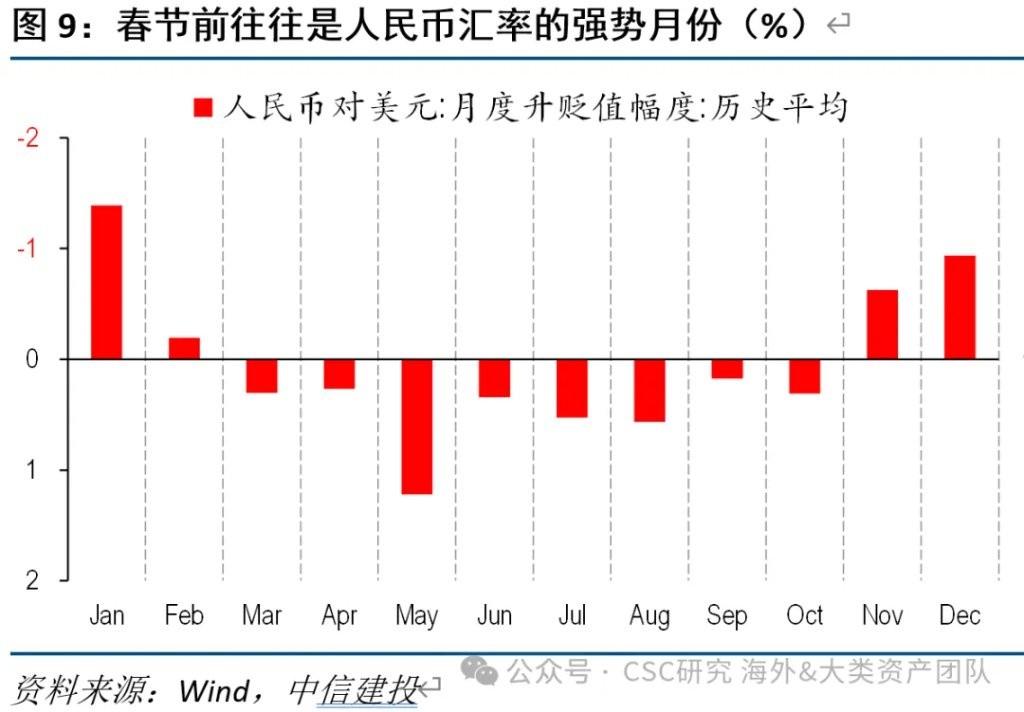

③ The period before the Spring Festival is often a strong month for the renminbi, and further appreciation pressure cannot be ruled out. The subsequent narrowing of exchange rate risks will be favorable for domestic institutions to increase their holdings of U.S. Treasuries.

Main Text

Since December last year, U.S. Treasury yields have begun a rising process, with the 10-year yield increasing by about 30 basis points from around 4%. On January 20, it rose by 9 basis points during the day, breaking through the 4.3% mark. This is due to multiple negative factors, with the main background including:

(1) A phase of paused rate cuts, with the Federal Reserve entering an observation period, leading to the market exhausting bullish trades

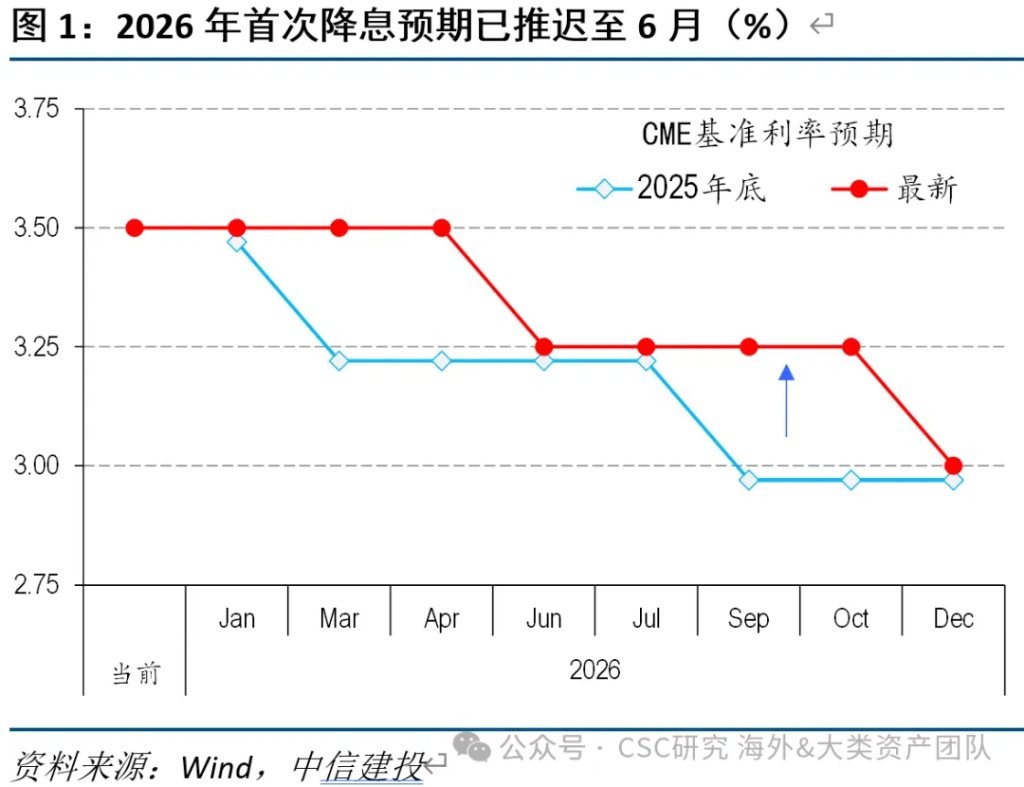

Due to abnormally low CPI data in November and December, which did not gain more trust from the market and the Federal Reserve, expectations for rate cuts have continued to converge. As of last weekend, the market has pushed back the first rate cut expectation from March to June, and several Federal Reserve officials have voiced support for the Fed's independence and maintaining short-term policies unchanged.

In this context, the market has exhausted bullish trades, leading to rising yields. Similar situations occurred in September and October, where after two rate cuts, U.S. Treasury yields rebounded significantly.

(2) The market has entered recovery and inflation trades, which are unfavorable for bonds

On one hand, under favorable policies such as rate cuts and tax reductions, the market has high expectations for a recovery in the U.S. economy by 2026, even though recent employment data has been average and recession fears have almost not emerged. A typical example is that, according to sector earnings forecasts for U.S. stocks, traditional cyclical industries (materials, energy, industrials, consumer, real estate, etc.) are expected to improve systematically by 2026 On the other hand, extreme market conditions have emerged in commodities, with gold, silver, and copper all rising sharply, reaching historical highs, and inflation trading is prevalent.

(3) Trump's extreme policies frequently emerge (geopolitical, economic, Federal Reserve), consuming the credibility of U.S. Treasury bonds

As we enter the midterm election year, Trump has clearly intensified his intervention efforts. Geopolitically, there have been raids in Venezuela, escalating tensions in Iran, and threats to Greenland and even Canadian sovereignty; economically, he has demanded that Fannie Mae and Freddie Mac purchase MBS for disguised QE, setting a cap on credit card interest rates at 10%, and previously proposed a $2,000 tariff rebate plan; regarding the Federal Reserve, he has facilitated a criminal investigation into Powell, and the selection of a new chairperson has once again become uncertain.

These various policies constitute a negative impact on U.S. Treasury bonds, similar to the market shock from the "Tariff Liberation Day" last April: potential increases in oil prices, overheating of the economy, loss of Federal Reserve independence, and hostility from Canada and the EU towards the U.S. (selling U.S. Treasury bonds).

(4) The drag of Japan's bond market losing strength

Entering 2026, concerns over the new prime minister's fiscal policy continue to fester, causing the yen and Japanese bonds to decline further, especially as Japanese government bond yields rose more than 10 basis points in a single day on January 20, significantly dragging down the bonds of developed countries globally. As a result, the 10-year U.S. Treasury yield also rose by 5-10 basis points on that day.

(5) Seasonal disadvantages at the beginning of the year, historically stocks outperform bonds during the Christmas and New Year holidays

Additionally, from the seasonal trends of stocks and bonds each year, the market sentiment tends to be better at the end of the year and the beginning of the year due to the Christmas and New Year holidays, making U.S. stocks likely to strengthen, while U.S. bonds are often suppressed in December and February.

Looking ahead, we remain optimistic about the annual trend of U.S. Treasury bonds. The recent dual pressure from interest rates and exchange rates will provide buying opportunities, particularly after the Spring Festival until March.

Several important judgments:

(1) U.S. Treasury bonds may continue to be under pressure in the first quarter

Economic trends and interest rate cut expectations remain the core of U.S. Treasury yields, and it is not easy to falsify the recovery and inflation logic with first-quarter data. On one hand, the government shutdown in Q4 last year led to poor data, and there may be a rebound in data this first quarter, as CPI data in recent years tends to seasonally rise in January; on the other hand, even if the data continues to be poor, the market is still trading based on expectations, and just one or two months of data cannot reverse optimistic sentiment. The recent significant decline in CPI has been selectively ignored by the market, which serves as an example In addition, Trump's extreme policy trends are unpredictable and may still cause disturbances.

(2) However, looking at the whole year, there is still considerable room for decline in U.S. Treasury yields. The U.S. recovery and inflation may be falsified, and the Federal Reserve is expected to cut interest rates more than the current expectation of 1-2 times.

The market's expectation for the recovery of the U.S. economy is based on anticipated policy improvements, but in reality, the current rate cuts by the Federal Reserve are still insufficient (U.S. Treasury yields have not significantly retreated compared to 2024). If fiscal stimulus is limited to the beautiful big plan, it cannot lead to a substantial increase in the deficit rate. Service inflation is lagging in its decline, and with a weak job market and wages, overall inflation is unlikely to constrain the Federal Reserve.

(3) The period before the Spring Festival is often a strong month for the Renminbi. If the Renminbi continues to release appreciation pressure against the U.S. dollar recently, the subsequent exchange rate risk will narrow, creating favorable conditions for domestic institutions to increase their holdings of U.S. Treasuries.

Recently, the exchange rate of the U.S. dollar against the Renminbi has also continued to rise. Given that the willingness to exchange currency remains strong in the short term, and that the beginning of each year is a major time window for Renminbi appreciation, it is possible that the Renminbi will continue to rise before the Spring Festival, releasing appreciation pressure. The combination of falling U.S. Treasuries and a strengthening Renminbi will pose considerable pressure on current U.S. Treasury holdings, but after entering March, U.S. Treasury yields and the Renminbi exchange rate may both reach a peak, providing a more ideal buying point.

Risk Warning and Disclaimer

The market has risks, and investment requires caution. This article does not constitute personal investment advice and does not take into account the specific investment goals, financial situation, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article are suitable for their specific circumstances. Investing based on this is at one's own risk.