U.S. stocks are fluctuating due to news about Trump! Goldman Sachs: The economy has support, but don't chase the rise, look for bottom-fishing opportunities

高盛認為,儘管關税風波與日債動盪加劇了短期波動,且投資者倉位處於歷史高位,但美國經濟增長強勁且美聯儲提供流動性支撐,宏觀前景依然利好。市場已由極度平靜轉入震盪,策略上建議保持 “審慎看漲”,側重逢低買入而非追漲。

在經歷了特朗普相關新聞引發的市場動盪後,高盛對沖基金覆蓋業務主管 Tony Pasquariello 給出明確判斷:儘管短期波動加劇、投資者倉位擁擠,但美國經濟基本面有支撐、美聯儲提供流動性支持,宏觀前景對股市"本質上有利"。策略上,今年應側重逢低買入,而非追漲。

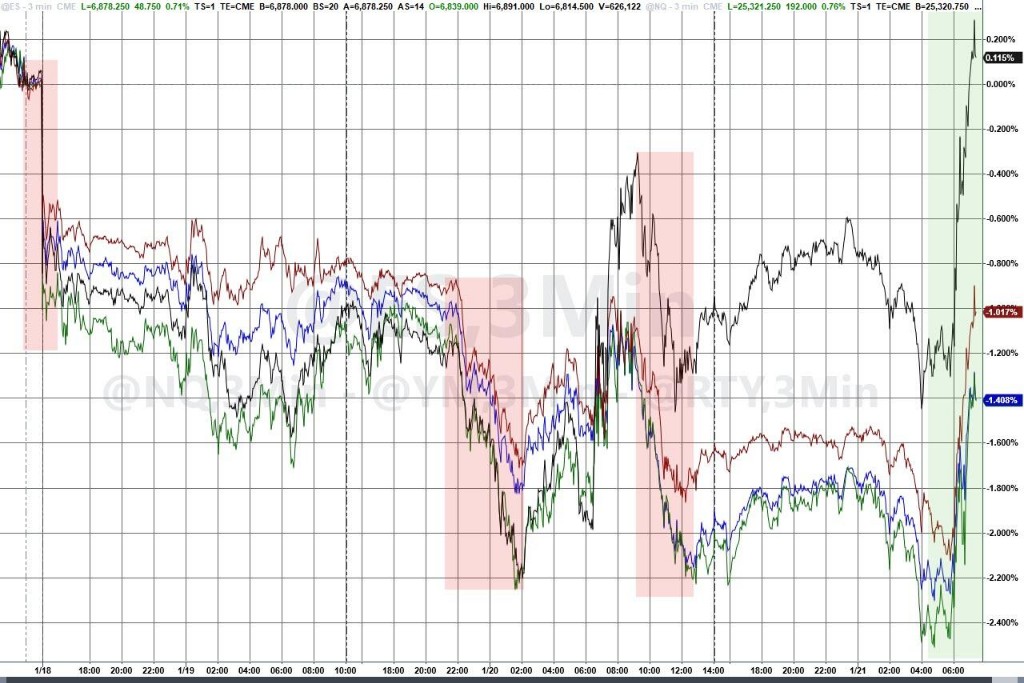

1 月以來市場情緒經歷了從亢奮到焦慮的劇烈轉換。儘管年初標普 500 指數波動率僅為 6%、債市波動率指標 MOVE 指數降至多年低位,但本週市場感覺已明顯改變。關税相關消息反覆、日本國債市場動盪兩大因素,令市場波動性從極低水平重燃。

投資者倉位問題令風險管控空間收窄。無論是散户還是專業機構,無論是個股持倉還是指數期貨,幾乎所有持倉指標都觸及近期歷史高位。與此同時,美國個人投資者協會 (AAII) 情緒調查顯示,投資者樂觀程度達到 2024 年 11 月以來最高。

但 Pasquariello 強調不應忽視核心邏輯:美國經濟增長明顯,美聯儲加大流動性供應。這一組合是中期內股市的關鍵宏觀驅動力。他維持"審慎看漲"立場,認為當前風險回報比較棘手,但在更好的價位入場,股市仍將獲得宏觀面支撐。

市場從極度平靜轉向波動

今年 1 月成為市場快速變化的典型案例。上週五之前,全球主要資產市場在新年伊始表現異常穩定。標普 500 指數實際波動率僅為 6%,債市波動率指標 MOVE 指數持續下滑至多年低位。

但局面迅速逆轉。Pasquariello 指出,科技和地緣政治變化節奏"顯然令人震驚",多方力量以極快速度行動,由此產生緊張和交叉影響。金融資產實際上成為各方辯論和權衡重大議題的公開市場公投。目前市場感覺已經改變,尾部風險看起來更寬。

兩大風險因素引發關注

在當前的風險因素中,Pasquariello 更關注日本國債市場動盪的持續影響。他援引客户觀察指出,去年美國國債市場儘管經歷各種波折,但保持了顯著穩定性,為風險資產提供了壓艙石作用。數據顯示,去年各季度末美國 10 年期國債收益率分別為:一季度 4.21%、二季度 4.23%、三季度 4.15%、四季度 4.17%。

他提醒股票交易員應密切關注全球固定收益市場,股票風險敞口應嵌入對收益率曲線更陡峭、期限溢價更高的預期。此外,圍繞關税的"頭條新聞輪盤賭"捲土重來,也成為市場需要消化的不確定因素。

投資者持倉處於歷史高位

持倉維度的風險值得警惕。Pasquariello 指出,近期交易羣體——包括散户和專業投資者——已增加大量風險敞口。他追蹤的幾乎所有指標,包括個股或指數期貨、總敞口或淨敞口,都在觸及近期歷史區間的上限。

多項情緒調查也顯示投資者已進入樂觀區域,美國個人投資者協會情緒指標達到 2024 年 11 月以來最樂觀水平。Pasquariello 表示,這些因素本身不是"逃跑的理由",但確實構成了一個戰術層面容錯空間較小的局面。至少在極短期內,他不會對市場出現更多風險轉移感到意外。

經濟基本面提供支撐

儘管短期存在多重干擾因素,Pasquariello 強調不應忽視核心要素:美國經濟增長趨勢向上,美聯儲正加大流動性供應。這一互動關係是中期內股市的關鍵宏觀驅動因素,有別於每日的噪音和新聞流。

上週多項數據表現突出。ISM 服務業指數升至 54.4,創一年多來最高;首次申請失業救濟人數降至 19.8 萬,屬於明顯健康水平;多項住房活動指標顯示企穩跡象。高盛美國當前活動指標已升至 2024 年底以來未見的水平。

高盛經濟學家 Joseph Briggs 對美國經濟前景持積極態度。他預計未來三個月約 1000 億美元將通過税收退款流回家庭部門,對近期增長構成支撐。政策利率方面,考慮到新任美聯儲主席以及核心 PCE 預計將滑落至 2.1%,利率仍有望降至 3%。

策略:買跌不追漲

Pasquariello 將自己的立場概括為"審慎看漲",承認這一表述存在兩難:市場上漲時,"審慎"部分顯得保守;市場下跌時,"看漲"部分又顯得激進。但他選擇堅持這一判斷。

用更正式的表述:本質上有利的宏觀前景應支撐美國股市,但在看到更好的價位之前,風險回報比仍然棘手。他認為,今年的操作策略將傾向於逢低買入,而非追漲。

當前市場面臨的矛盾在於:一邊是關税新聞反覆、全球債市動盪、投資者持倉擁擠等短期擾動因素;另一邊是美國經濟增長、流動性改善等中期利好支撐。這要求投資者在戰術層面保持謹慎,在戰略層面維持信心,把握市場回調帶來的入場機會。