Forget about Q4 performance, the biggest highlight of Tesla's earnings report next week is the robot and autonomous driving

Morgan Stanley believes that the focus of Tesla's upcoming earnings report on the 29th has shifted from financial metrics to cutting-edge technologies such as unsupervised FSD, Robotaxi, and the Optimus robot. Despite facing pressures from lower-than-expected delivery volumes in 2026 and cash flow consumption, the progress of its AI5 chip and Cybercab mass production will determine the stock price direction. The market is closely watching Tesla's strategic transformation from a traditional automaker to an AI and robotics company

Tesla is set to announce its fourth-quarter financial report on the 29th, with investors shifting their focus from traditional financial metrics to advancements in cutting-edge technologies such as robotaxi, unsupervised autonomous driving, the humanoid robot Optimus, and the AI5 chip. According to the latest research report from Morgan Stanley, incremental information on these technological updates will determine stock price reactions, rather than unconventional delivery or profit margin data.

According to news from the Wind Trading Desk, Morgan Stanley analyst Andrew S. Percoco's team pointed out in a report on the 21st that there is a significant divergence in market expectations for Tesla's key financial metrics in 2026. The firm expects Tesla's 2026 delivery volume to be 1.6 million vehicles, which is 9% lower than the market's general expectation and a 2.5% year-on-year decline. More notably, Morgan Stanley predicts that Tesla will experience a $1.5 billion free cash flow consumption in 2026, while the market consensus expects a positive $3.1 billion.

This pessimistic expectation mainly stems from the firm's belief that the market has not fully reflected Tesla's significant increase in capital expenditures in 2026. Morgan Stanley expects Tesla's automotive business gross margin (excluding carbon credits) to be 14.2% in 2026, lower than the market expectation of 15.0%, partly due to its cautious judgment on sales growth.

In terms of technological progress, the launch of the robotaxi service without safety supervisors in Austin, Texas, is seen as a key recent catalyst for validating its autonomous driving technology and safety. Additionally, the latest updates on the Cybercab, which is planned to be produced in April 2026, and the anticipated debut of the third-generation Optimus robot in February or March, will also become market focal points.

Robotaxi and Cybercab Production Entering a Critical Phase

According to the Morgan Stanley report, Tesla's launch of the robotaxi public service without safety supervisors in Austin, Texas, is a key recent catalyst for validating its robotaxi platform technology and safety. The firm expects Tesla to update the cumulative mileage data of its Austin robotaxi fleet during the earnings call, which is crucial for measuring safety improvements.

Morgan Stanley assumes that by the end of 2026, Tesla's robotaxi fleet will reach 1,000 vehicles. Notably, the Cybercab has been tested in multiple markets, including Austin, Texas, the San Francisco Bay Area and Fremont in California, Chicago in Illinois, and Buffalo in New York.

The production plan for the Cybercab is set to start in April 2026, and any updates regarding the production timeline will be closely monitored. This model, designed specifically for autonomous driving, is seen as a key product for Tesla's transformation from a traditional automaker to a mobility service provider.

Unsupervised FSD Promotion Path Becomes a Focus

The cumulative mileage of Tesla's Full Self-Driving (FSD) system has shown exponential growth. According to the report data, the cumulative mileage of FSD has increased from approximately 90 million miles in 2022 (an average of 150,000 miles per day) to about 7.4 billion miles currently (an average of 11 million miles per day in 2025). Meanwhile, third-party reports indicate that the quality of the FSD product has seen significant improvement Morgan Stanley believes that the next major breakthrough will occur when Tesla is able to provide a more enhanced "eyes-off" experience (i.e., unsupervised FSD). The firm expects this to be rolled out in phases throughout 2026 and thinks that Tesla's decision to remove safety supervisors for robotaxis in Austin may be a precursor to the personal unsupervised FSD launch.

Tesla's recent decision to make FSD a subscription-only service may signal the introduction of tiered FSD products and pricing strategies. Morgan Stanley assumes that the global FSD subscription rate will increase from the current approximately 12% to 17.5% by the end of the year. The approval and rollout of unsupervised FSD in Europe and China will be key factors driving long-term penetration rates. This feature is crucial to support Morgan Stanley's assumption of a 17.1% growth in vehicle sales by 2027.

AI Chips and Optimus Robot Update Coming Soon

Morgan Stanley expects Tesla to update its AI5 chip design progress during the earnings call, as well as how its chip projects and computing power investments will evolve over time, including projects like AI6+ and Dojo.

Tesla previously stated that the third-generation Optimus humanoid robot will debut in February or March 2026. This is becoming an increasingly important component of Tesla's story and valuation. Following the intensive showcase of humanoid robot products at this year's Consumer Electronics Show (CES), the market will closely monitor the latest information on product debut timing and production launch.

Morgan Stanley assigns a valuation of $60 per share to the Optimus business in its baseline scenario (applying a 50% probability discount). In a bull market scenario, the business valuation could reach $225 per share (0% probability discount).

Musk's Business Empire Synergy Draws Attention

The report notes that the integration of Musk's other businesses with Tesla has become clearer. The market is looking forward to updates on how these businesses will achieve synergies in the future.

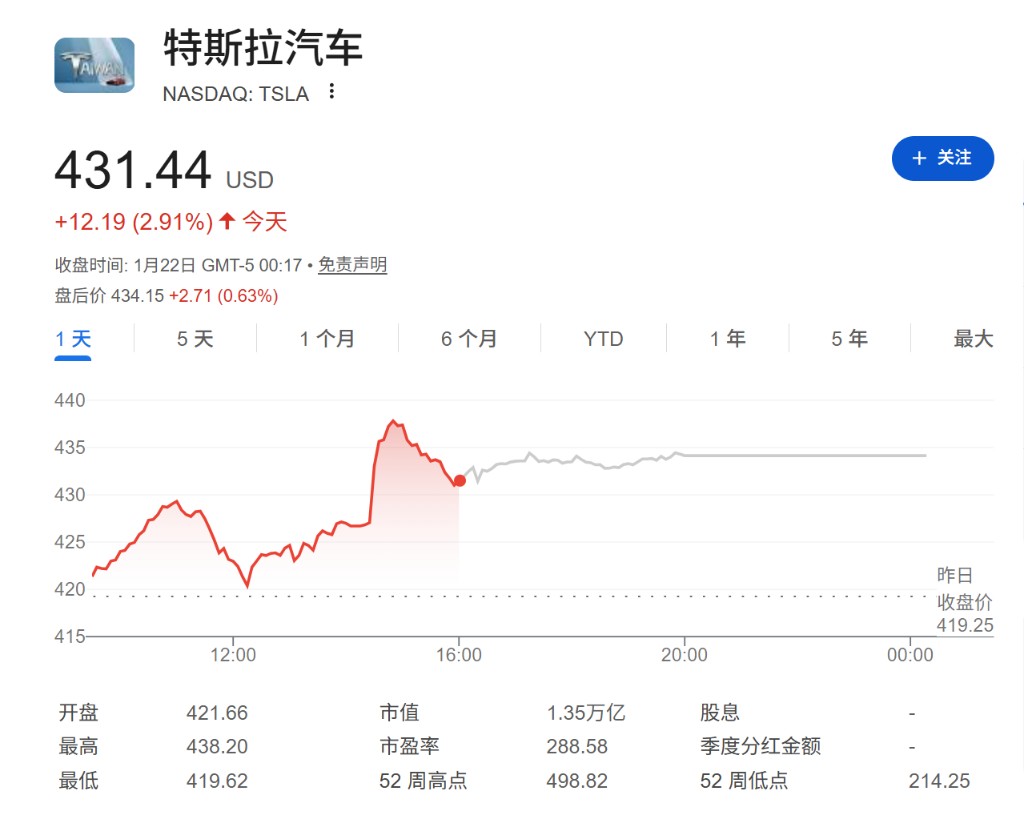

Morgan Stanley maintains a "hold" rating on Tesla with a target price of $425, while the current stock price is $431.25. The firm's target price is composed of five parts: $55 for the core automotive business, $145 for network services, $125 for mobility services, $40 for energy business, and $60 for humanoid robots.

In a bear market scenario, the firm gives a target price of $145; while in a bull market scenario, the target price could reach $860. This vast valuation range reflects the uncertainty Tesla faces as it transitions from a traditional automaker to an artificial intelligence and robotics company