Intel conference call: CPU demand surges but there are orders without inventory! CEO admits that inventory is depleted and yield rates are below standard, "I am very disappointed that we cannot meet the demand."

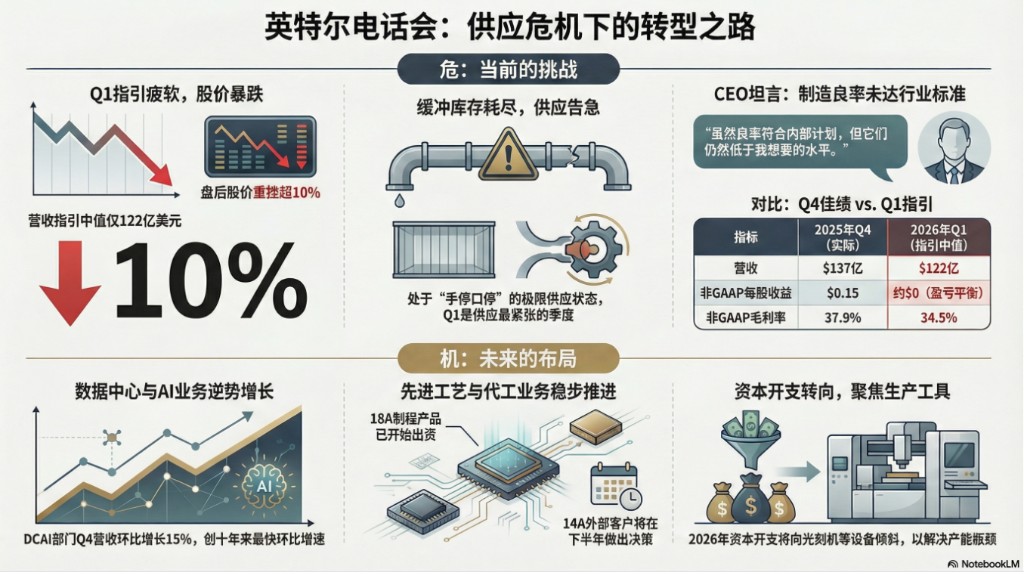

Intel's Q4 performance exceeded expectations, but weak guidance for Q1 led to a sharp decline in stock prices. CEO Chen Liwu admitted, "I am very disappointed that we cannot fully meet market demand." Despite strong demand for AI, particularly the critical role of CPUs in AI inference and orchestration driving a surge in orders from hyperscale cloud providers, the company is facing severe supply bottlenecks, with buffer inventory depleted, "orders without goods," and manufacturing yields not yet meeting internal standards

Key Points Summary:

Weak Q1 Guidance Leads to Sharp Stock Drop: Despite Q4 performance exceeding expectations, the midpoint of Q1 revenue guidance is only $12.2 billion, defined by the CFO as "at the low end of the seasonal range," resulting in a post-market stock plunge of over 10%.

Inventory Depletion: The company admits that "buffer inventory has been exhausted," and the capacity shift of wafers to server products will not yield results until the end of Q1, making Q1 the tightest supply quarter, facing an extreme supply situation of "hand to mouth."

CEO Discusses Yield Issues: Chen Liwu candidly stated that while the yield meets internal plans, it "is still below the level I want" and has not reached industry-leading standards. Improving yield will be a key lever in 2026.

Underestimated Role of CPUs in the AI Era: Management emphasized that the diversification of AI workloads has created significant capacity constraints, which in turn reinforces the CPU's role as the "core commander." From AI inference to orchestration control, CPUs are becoming increasingly indispensable, driving a strong upgrade cycle for traditional servers.

Strong AI and Data Center Demand but No Supply: DCAI (Data Center and AI) revenue increased by 15% quarter-over-quarter, but due to supply shortages, it missed out on "significantly higher" revenue; custom ASIC business is expected to grow over 50% in 2025, with a quarter-over-quarter increase of 26%, achieving over $1 billion in annualized revenue in Q4.

Foundry Timeline, 14A to Wait Until Second Half: 18A has begun shipping (Panther Lake), but exact orders for external customers of 14A will not be finalized until the second half of 2026 or the first half of 2027.

Capital Expenditure: CapEx is expected to remain flat or slightly decrease in 2026, with spending shifting towards wafer manufacturing equipment (Tools) and reducing expenditures on facility construction.

Overnight, Intel released a mixed earnings report. Although Q4 revenue and profit exceeded Wall Street expectations, the company's disappointing guidance for Q1 2026 was due to manufacturing yield issues and severe supply shortages caused by inventory depletion. This news led to a sharp drop of over 10% in Intel's stock during after-hours trading.

Intel CEO Chen Liwu pointed out the core of the issue candidly during the conference call: "I am disappointed that we cannot fully meet market demand." He stated that while the AI era has brought unprecedented semiconductor demand, Intel's current manufacturing yield, although meeting internal plans, "is still below the level I want." Additionally, the company consumed a large amount of inventory in the second half of 2025 to support demand, leading to "buffer inventory being exhausted" as it entered 2026.

Intel CFO Sinsner used a very vivid term to describe the current operational state: "It is essentially what is called 'hand to mouth'; we can only give customers what we can get from the wafer fab, and that is how we manage it." **”

Despite facing short-term pain, Intel emphasizes that its long-term transformation is still on track, especially as the market reassesses the value of CPUs in the AI ecosystem. The company revealed that the Core Ultra Series 3 (codenamed Panther Lake), based on the advanced 18A process, has been launched, and the data center business shows strong signs of recovery. Chen Liwu reiterated that rebuilding Intel will be a multi-year process, and the company is committed to regaining market trust by improving yield and execution, expecting external foundry customers to make firm supplier decisions in the second half of this year.

In the fourth quarter ending in December, Intel achieved revenue of $13.7 billion, at the high end of the previous guidance range; non-GAAP earnings per share (EPS) were $0.15, far exceeding the expected $0.08. However, market focus quickly shifted to the bleak Q1 outlook. Intel expects first-quarter revenue to be between $11.7 billion and $12.7 billion, with a midpoint of $12.2 billion indicating below-normal seasonal levels. More critically, the company anticipates Q1 non-GAAP gross margin will decline to 34.5%, with EPS barely breaking even.

“Buffer inventory has been exhausted,” CEO admits yield pain point: “Not yet at industry standards”

Supply shortages are the biggest headwind Intel currently faces. CFO David Zinsner explained that part of the weak Q1 guidance is due to “failing to meet the supply needed for seasonal demand.” He noted that internal supply constraints are most severe in Q1.

“Our buffer inventory has been exhausted,” Zinsner stated, noting that the shift in wafer production to server products began in Q3, but this capacity will not yield results until later in Q1. This means that in the short term, Intel can only “make to order” and cannot rely on inventory to buffer demand fluctuations.

In addition to inventory strategy missteps, the slow ramp-up of manufacturing yield is the fundamental reason limiting supply. As a CEO who has been in office for only 10 months, Chen Liwu chose not to sugarcoat the situation but instead responded candidly to analysts' concerns about yield.

“While the yield meets our internal plans, they are still below the level I want.” Chen Liwu candidly stated in response to a question from a Deutsche Bank analyst. He pointed out that while there has been a monthly yield improvement of 7%-8%, in terms of defect density and consistency, Intel “has not yet reached industry-leading standards.”

This candor, while earning trust, has also heightened short-term market concerns. Chen Liwu emphasized that accelerating yield improvement will be the most important lever in 2026, but this will take time and does not require additional capital investment, relying mainly on engineering optimization

Chen Liwu video screenshot

Undervalued CPU: The "Core Commander" in the Era of AI Inference

During this conference call, in addition to addressing supply crises, management spent a significant amount of time correcting the market's misunderstanding that "CPUs are dead in the AI era."

Chen Liwu pointed out: "The continuous surge and diversification of AI workloads have brought significant capacity constraints... This further reinforces the increasingly important role of CPUs in the AI era."

He explained that relying solely on cloud-based GPU computing power cannot meet the required scale of inference, especially in constrained power environments. This is accelerating the shift towards "hybrid AI," which allocates workloads between the cloud and client-side (such as AI PCs), with CPUs being the core of this hybrid architecture.

CFO Zinsner also added a key trend: The world is shifting from "human prompt requests" to "computer-to-computer interactions," and this persistent and recursive command flow requires powerful CPUs for orchestration and control.

"The core function of CPUs coordinating this traffic will not only drive updates to traditional servers but also create new demand for increased installed bases," Zinsner stated. It is this unexpectedly strong demand for CPUs, combined with Intel's own supply bottlenecks, that has led to the current shortage situation.

Data Center Priority Strategy, PC Business Under Pressure

With limited capacity, Intel has made a clear strategic trade-off: Prioritize supply for high-margin data center business.

The financial report shows that the DCAI (Data Center and AI) department's Q4 revenue reached $4.7 billion, a 15% quarter-over-quarter increase, marking the fastest quarter-over-quarter growth for the department in a decade. Zinsner noted, If supply were sufficient, revenue could have been "significantly higher." In contrast, the Client Computing Group (CCG) revenue fell 4% quarter-over-quarter, despite a 16% increase in AI PC shipments.

"When possible, we will prioritize internal wafer supply for data centers and utilize more external foundry resources in client products," Zinsner explained. This means that in Q1, the revenue decline for the CCG business will be more pronounced than for DCAI. Chen Liwu emphasized that the demand for CPUs from hyperscalers is returning, and the core role of CPUs in AI inference and orchestration is driving the traditional server refresh cycle.

Additionally, Intel's custom ASIC business has become a highlight, with a Q4 annualized revenue run rate exceeding $1 billion, a year-over-year increase of over 50%.

Foundry Business: 14A Major Clients Still Need to Wait Until the Second Half

As the core of Intel's revitalization plan, the progress of the foundry business (Intel Foundry) is closely watched. Chen Liwu stated that establishing the foundry business requires time and resources, but early milestones have been achieved Currently, Intel is the only semiconductor manufacturer in the world to achieve mass production of Gate-All-Around (GAA) transistors and PowerVia technology, which have been applied in the 18A process. For the more advanced 14A process, the company has currently released version 0.5 of the PDK and is actively engaging with potential customers.

Regarding when external customers will place orders, Chen Liwu provided a clear timeline: “We believe customers will start making firm supplier decisions in the second half of this year and continue into the first half of 2027.” He emphasized that the company will strictly control capital expenditures for 14A capacity until it receives confirmed customer commitments. This means that risk trial production for 14A may have to wait until later in 2027, while mass production is expected in 2028.

Capital Expenditure Strategy Adjustment

In response to supply bottlenecks, Intel has adjusted its capital expenditure (CapEx) strategy for 2026. While the total amount is expected to remain flat or slightly decrease, the allocation of funds has undergone a dramatic change. The company will significantly reduce its investment in facility construction (Space) and instead greatly increase spending on production tools (Tools), attempting to address the imminent capacity shortage through equipment purchases.

Full Translation of Intel's Q4 2025 Earnings Call:

January 23, 2026 - 7:57 AM

Company Participants:

David Zinsner, Chief Financial Officer

John Pitzer, Senior Vice President of Investor Relations

Lip-Bu Tan, Chief Executive Officer

Other Participants:

- Analysts from institutions such as Wells Fargo, Melius, Cantor Fitzgerald, JP Morgan, Morgan Stanley, Deutsche Bank, Bernstein Research, and Bank of America Securities.

Meeting Process

Operator

Hello everyone, welcome to Intel Corporation's Q4 2025 earnings call. At this time, all participants are in listen-only mode. After the presentation, there will be a question-and-answer session. (Instructions) Now, please allow me to introduce today's host, Mr. John Pitzer, Senior Vice President of Investor Relations. Please go ahead, sir.

John Pitzer

Thank you, Jonathan, good afternoon everyone. By now, you should have received the Q4 earnings press release and earnings presentation, both of which are available on our investor website at intc.com. For those attending online, the presentation is also viewable in the webcast window. Joining me today are our CEO Lip-Bu Tan and CFO David Zinsner

Lip-Bu will first comment on our performance in the fourth quarter and introduce the progress we have made on strategic priorities. Then, Dave will discuss our overall financial performance, including guidance for the first quarter, after which we will answer your questions.

Before we begin, please note that today’s discussion contains forward-looking statements based on our current view of the environment, and is therefore subject to various risks and uncertainties. The discussion also includes references to non-GAAP financial metrics, which we believe can provide useful information to investors. Our earnings release, the latest 10-K annual report, and other documents filed with the SEC provide more information about specific risk factors that could cause actual results to differ materially from our expectations. These documents also provide additional information about non-GAAP financial metrics, including reconciliation tables to the corresponding GAAP financial metrics where appropriate.

Next, I will turn the time over to Lip-Bu.

Lip-Bu Tan (CEO)

Thank you, John, and thank you all for joining us today. 2025 is a year of solid progress. Over the past 10 months, we have laid the foundation for the "new Intel." This is a more focused, execution-oriented company. We have streamlined our organizational structure, significantly reduced bureaucracy to improve efficiency and accelerate decision-making. We have also recruited new leaders from outside and empowered key leaders internally. We have strengthened our balance sheet, established strong new partnerships, and deepened relationships with existing and new customers.

I am encouraged by the conversations with global customers and partners. I have heard a clear and consistent message: they see the progress we are making. As they undergo their own transformations, they want Intel to be a part of it. The opportunities before us are meaningful and vast.

The era of artificial intelligence is driving unprecedented demand for semiconductors across the entire computing spectrum—from AI acceleration and traditional data centers to networking and enterprise, extending all the way to client and edge devices. Rapidly deploying AI workloads in this diverse environment will require leveraging heterogeneous chip solutions that utilize CPUs, embedded MPUs, discrete and integrated GPUs, ASICs, and XPUs. Additionally, we need to see innovation in the software stack, as well as breakthroughs in emerging technologies such as photonics, memory interfaces, interconnects, and quantum technologies.

With our extensive IP and expertise in chip design, system-level integration, wafer manufacturing, and advanced packaging, we have a unique advantage to capitalize on these AI-driven trends and achieve sustainable profit growth. This will not happen overnight, and our execution needs to continue to improve. But as we tackle the work ahead, we will remain humble and never be satisfied.

Our Q4 is another positive step forward. Revenue, gross margin, and earnings per share all exceeded our guidance. Despite facing supply constraints, we achieved these results, which have largely limited our ability to capture all the strong demand in the potential market. We are actively addressing this issue to better support customer needs in the future

Looking ahead to 2026, we will continue to position Intel to capture the tremendous growth opportunities that AI brings across all our businesses. We will achieve this by strengthening our client franchise, advancing our data center, AI accelerator, and ASIC strategies, and continuing to build trusted U.S. foundries.

Let me start with our core X86 franchise, which remains the most widely deployed computing architecture in the world. The deployment of AI will only amplify the importance of X86, from orchestration and control planes to inference edge workloads and AI.

In our Client Computing Group (CCG), we have solidified our position in consumer and enterprise laptops with the Core Ultra Series 3 (formerly codenamed Panther Lake), which is based on our cutting-edge Intel 18A manufacturing process. We initially committed to delivering the first Series 3 SKU by the end of 2025, and we have actually delivered the first three SKUs, exceeding that commitment. While we still have work to do, I am encouraged by the steady progress of Intel 18A yields, and Naga and his team remain focused on further improvements to elevate Series 3 to the high-volume production needed to meet strong customer demand.

Our client momentum was fully showcased earlier this month at CES, where we officially launched Series 3 in collaboration with OEM partners, powering designs for over 200 laptop models. Series 3 will become the most widely adopted and globally available AIPC platform we have delivered. Coupled with the next-generation Nova we will launch by the end of 2026, our current client roadmap combines top-tier performance with cost-optimized solutions, which gives me confidence that we are on the path to solidifying market share and profitability in the coming years, both in the laptop and desktop segments.

Additionally, PCs are becoming an important component of AI infrastructure. The surge in AI workloads is driving tremendous demand for data centers, but cloud capacity alone cannot meet the required inference scale, especially in constrained power environments. This accelerates the push towards hybrid AI—distributing workloads between cloud and edge, which offers clear advantages in performance, cost, and control. We are working closely with ecosystem partners to seamlessly enable hybrid AI, and we are encouraged by the opportunities to increase the installed base and accelerate the update rate over time.

Now let me talk about Data Center and Artificial Intelligence (DCAI). To support our AI goals, I believe our traditional server and accelerator roadmaps must advance in tandem. To strengthen this alignment, I have centralized our data center and AI business to ensure tight coordination between CPU, GPU, and platform strategies.

Demand for traditional servers remains very strong, and we are focused on enhancing available capacity to support the significant growth we are seeing, including working with major customers to support their needs beyond 2026. The ongoing proliferation and diversification of AI workloads present significant capacity constraints on both traditional and new hardware infrastructures, reinforcing the increasingly vital and indispensable role of CPUs in the AI era This is currently and will continue to benefit the ongoing ramp of Granite Rapids, as well as our mainstream product Sapphire Rapids.

We have also made decisive changes to simplify our server roadmap, focusing resources on the 16-channel Diamond Rapids and accelerating the introduction of Rapids where possible. Through Rapids, we will also reintroduce hyper-threading technology into our data center roadmap. We continue to work closely with NVIDIA to build a custom Xeon fully integrated with its NVLink technology, bringing best-in-class X86 performance to AI host nodes.

Over the past few quarters, we have been formulating a broad AI and acceleration strategy, with plans to refine it in the coming months. This will include integrating our X86 CPU with innovative options for fixed-function and programmable accelerator IP. Our focus is on the emerging wave of AI workloads—inferencing models, Agentic AI, and physical AI, as well as scalable inference, where we believe Intel can truly achieve disruption and differentiation. Our long-term ambition is clear: to rebuild Intel as the preferred computing platform for the next AI-driven computing era, grounded in world-class engineering design, an accelerated roadmap, and a redefined execution culture.

We are also building momentum in ASICs, as customers seek dedicated chips for AI, networking, and cloud workloads. Our combination of design services, IP building blocks, and manufacturing capabilities positions Intel favorably to solve specialized problems at scale. This is not a new area for us, but I am committed to putting more focus, resources, and investment funds into it, including leveraging my experience at Cadence Design to support and grow this market.

Finally, we remain focused on establishing a long-term goal of building world-class wafer and advanced packaging foundries, based on trust, consistency, and execution. As I mentioned earlier, building a foundry business takes time and a significant amount of energy and resources. While our journey is still in its early stages, we have already achieved some important early milestones worth highlighting.

We are now shipping the first products built on Intel 18A, which is the most advanced semiconductor process developed and manufactured in the United States. As mentioned earlier, yields continue to improve steadily, and we are working to increase supply to meet strong customer demand. Additionally, Intel 18 AP continues to progress well, and we are engaging with internal and external customers regarding this node, having delivered our 1.0 PDK at the end of last year.

**The development of Intel 14A is still on track. We have taken meaningful steps to simplify our process flows and improve our performance and yield improvement rates. We are developing a comprehensive IP portfolio on Intel 14A and continue to enhance our design support approach. Importantly, our PDK is now regarded by customers as the industry standard. Engagements with potential external customers regarding Intel 14A are actively ongoing. We believe customers will make firm vendor decisions starting in the second half of this year and into the first half of 2027 **

We also have the opportunity to provide strong differentiated advantages in advanced packaging, particularly by leveraging EMIB and Foveros technologies. We are focused on improving quality and yield to support our customers' desire to begin mass production in the second half of 2026.

In conclusion, reflecting on 2025, I am proud of the resilience and commitment demonstrated by our team. We have a stronger foundation by the end of the year and a clear roadmap for 2026 and beyond. As AI-driven computing expands into all the markets we serve, the future opportunities are significant and immense.

But I am equally aware of the challenges we face and remain transparent about the areas where I have performed well and where improvements are needed. In the short term, I am disappointed that we are unable to fully meet market demand. My team and I are working tirelessly to improve efficiency and get more output from our fabs. While yields are in line with our internal plans, they are still below the levels I desire. Accelerating yield improvement will be an important lever in 2026 as we seek to better support our customers.

As mentioned earlier, we are on a multi-year journey. This will take time and determination, but my team and I are committed to rebuilding this iconic American company and enhancing long-term shareholder value. I want to thank my team for their hard work over the past 10 months. I look forward to updating everyone on our progress as we continue this journey, including hosting an Investor Day at our Santa Clara headquarters in the second half of this year.

Now, I will turn it over to Dave to provide details on our financial and business trends.

David Zinsner (Chief Financial Officer)

Thank you, Lip-Bu. We remain encouraged by the fundamental drivers of demand in our core markets. Fourth-quarter revenue was $13.7 billion, at the high end of the range we provided in October. We experienced strong growth across all businesses, benefiting from AI infrastructure buildout, with AIPC, traditional server, and networking revenues all achieving double-digit growth both sequentially and year-over-year.

Q4 marks our fifth consecutive quarter of revenue exceeding guidance, even as we faced industry-wide supply constraints on key products. Non-GAAP gross margin was 37.9%, approximately 140 basis points above guidance. This was due to higher revenues and lower inventory reserves, partially offset by an increase in the outsourced client product mix and the early ramp of Intel 18A supporting the Core Ultra Series 3 (codenamed Panther Lake) launch.

We delivered a non-GAAP earnings per share of $0.15 for Q4, while our guidance was $0.08, driven by higher revenues, stronger gross margins, and continued spending discipline. Q4 operating cash flow was $4.3 billion, with total capital expenditures (CapEx) for the quarter at $4 billion, and adjusted free cash flow was a positive $2.2 billion. Nvidia's $5 billion investment was completed as scheduled in Q4

Full-year revenue was $52.9 billion, a slight decrease year-on-year, due to limitations in our own manufacturing network and external suppliers, which constrained growth, particularly in the second half. The full-year non-GAAP gross margin was 36.7%, up 70 basis points due to a reduction in expenses during the period. The full-year non-GAAP earnings per share were $0.42, an increase of $0.55 year-on-year, benefiting from lower expenses and improved operating leverage. Specifically, non-GAAP operating expenses were $16.5 billion, down 15% from 2024, as we took actions to reduce complexity and bureaucracy in the business and drive improved execution.

For the full year, we generated $9.7 billion in cash from operations and made a total capital investment of $17.7 billion, with capital offsets of approximately $6.5 billion. Although the adjusted free cash flow for 2025 was negative $1.6 billion, we generated $3.1 billion in the second half, as operating cash flow more than doubled quarter-on-quarter.

By the end of 2025, we had $37.4 billion in cash and short-term investments, thanks to further monetization of Mobileye, completion of the sale of Altera shares to Silver Lake, accelerated funding support from the U.S. government, and investments from SoftBank Group and NVIDIA. Additionally, we repaid $3.7 billion in debt.

Looking back, 2025 marked a year of significant progress on our key priorities, although we recognize there is still more work to be done. Internally, we restructured and resized our teams to be customer-centric and focused on engineering, while strengthening our balance sheet to provide greater flexibility in pursuing our goals. We navigated a market that shifted from tariff-driven uncertainty in the first half to a strong AI-driven demand environment constrained by supply in the second half.

2025 showcased the resilience of the X86 ecosystem in both client and data center segments, as well as the importance of our manufacturing assets, with the launch of the Core Ultra Series 3 on Intel 18A, the most advanced process fully developed and manufactured in the U.S., both of which laid a solid foundation for building the new Intel.

Turning to segment performance. Intel Products Q4 revenue was $12.9 billion, a 2% quarter-on-quarter increase. CCG (Client Computing Group) revenue decreased 4% quarter-on-quarter, despite a 16% increase in AIPC shipments; DCAI (Data Center and Artificial Intelligence Group) grew 15%, reflecting strong demand for traditional server computing. These results reflect our efforts to balance constrained supply with strong data center demand while maintaining support for client OEM partners. Where possible, we prioritized internal wafer supply for data centers and utilized more external wafer sourcing in the client segment.

CCG revenue was $8.2 billion, in line with our expectations. We estimate that the client consumer TAM (Total Addressable Market) for 2025 exceeds 290 million units, marking two consecutive years of growth since the post-pandemic bottom in 2023, and the fastest TAM growth since 2021 In this quarter, CCG launched three Series 3 SKUs, exceeding our expectations by one. The performance evaluations are very satisfactory, with a battery life of up to 27 hours, a 70% improvement in graphics performance, and performance in industry-standard benchmark tests that is 50% to 100% better than peers.

DCAI revenue was $4.7 billion, a quarter-over-quarter increase of 15%, higher than expected, marking the fastest quarter-over-quarter growth in the past decade. If we had more supply, revenue would have been significantly higher. While the market continues to benefit from more energy-efficient CPUs, stimulating the upgrade cycle, all indicators point to the increasingly vital and indispensable role of CPUs in large-scale and enterprise AI data centers as AI usage driven by inference expands.

The world is shifting from human-prompted requests to persistent and recursive commands driven by computer-to-computer interactions. The core CPU functionality coordinating this traffic will not only drive upgrades of traditional servers but also create new demand for an increased installed base. Additionally, due to the network demand from AI infrastructure construction, our custom ASIC business is expected to grow over 50% in 2025, with a quarter-over-quarter growth of 26%, reaching an annualized revenue run rate of over $1 billion in Q4. This strength provides a solid foundation for our ASIC team to pursue a $100 billion TAM opportunity.

Intel Products' operating profit was $3.5 billion, accounting for 27% of revenue, a quarter-over-quarter decrease of about $200 million, due to an increase in outsourced product mix and seasonally higher operating expenses.

Intel Foundry achieved $4.5 billion in revenue, a quarter-over-quarter increase of 6.4%, primarily due to an increase in EUV wafer mix. EUV wafer revenue grew from less than 1% of wafer output in 2023 to over 10% in 2025. External foundry revenue was $22 million, mainly driven by U.S. government projects and the Altera divestiture. Intel Foundry's operating loss in Q4 was $2.5 billion, worsening by $188 million quarter-over-quarter, primarily impacted by the early ramp of Intel 18A.

In this quarter, Intel Foundry achieved key milestones for 18A and 14A. With the official launch of the Core Ultra Series 3, Intel Foundry is the only semiconductor manufacturer in the world to ship revenue-generating Gate-All-Around transistors with backside power delivery. These advanced wafers are being produced on our production lines in Oregon and Arizona, USA.

Finally, our continued progress on Intel 14A demonstrates our commitment to developing the world's most important technologies domestically in the U.S.

Turning to the "All Other" business, revenue was $574 million, a quarter-over-quarter decrease of 42%, due to the completion of the Altera divestiture in Q3 25. The main components of Q4 "All Other" are Mobileye and IMS. The overall operating loss for this category was $8 million. I am pleased with the early momentum shown by Altera as an independent company with a new leadership team Their industry-leading programmable architecture, software tools driven by developer productivity, and large installed base put them in a favorable position to drive long-term value creation.

Now turning to guidance. In the second half of 2025, we supported strong product demand through wafer production within the quarter and available inventory. As we enter 2026, our buffer inventory has been depleted, and the transition of wafers to servers (which began in Q3) will not yield output from the fabs until later in Q1. Therefore, as we mentioned last quarter, our internal supply constraints will be most severe in Q1.

Given these dynamics, we forecast Q1 revenue in the range of $11.7 billion to $12.7 billion. The midpoint of $12.2 billion reflects the low end of the seasonal range for Q1. Within Intel Products, we expect the revenue decline in CCG to be more pronounced than in DCAI, as we continue to prioritize internal supply allocation to the server end market.

We expect Intel Foundry revenue to achieve double-digit growth quarter-over-quarter, driven by the continued transition to EUV wafers and pricing for Intel 18A. At the midpoint of $12.2 billion, we anticipate a gross margin of approximately 34.5%, a tax rate of 11%, and a non-GAAP earnings per share at breakeven. The quarter-over-quarter decline in gross margin is due to lower revenue, increased AT&A (assembly, test, and related) volumes, and product mix.

Let me take a moment to provide some background for your full-year model for 2026. First, from a revenue perspective, we expect our factory network to improve available supply starting in Q2 and throughout the remaining quarters of 2026. In the server market, customer feedback and our own market intelligence suggest that DCAI may have a strong year. Finally, client CPU inventory is being streamlined, and the market is excited about Series 3. In contrast, over the past few months, the supply of key components such as DRAM, NAND, and substrates has faced increasing pressure across the industry due to strong demand supporting the rapid expansion of AI infrastructure. Component price increases are a dynamic we continue to monitor closely, particularly relative to the client market, as this may limit our revenue opportunities this year.

For operating expenses (OpEx), our goal is to have operating expenses of $16 billion in 2026. We expect non-controlling interests (NCI) to be approximately $325 million net in Q1, with about $1.2 billion on a GAAP basis for the full year. NCI is expected to grow significantly again in fiscal year 2027.

First, we expect our share count to be 5.1 billion shares in Q1, which will grow with our future stock-based compensation. When considering capital expenditures for 2026, we are working to balance the ability to drive capital efficiency with the need to respond to the demand signals we receive. Previously, we indicated that capital expenditures would decline, but now we plan for flat to slightly down spending, with expenditures more concentrated in the first half. Just a reminder, capital expenditures in 2026 will be used to support demand in 2027 and beyond

We expect to generate positive adjusted free cash flow for the full year and plan to repay all $2.5 billion of maturing debt this year.

To summarize, Q4 was another solid quarter, marking our fifth consecutive quarter of exceeding guidance. As we approach the end of 2025, we are increasingly confident in the long-term sustainability of the end markets we serve. We believe this is due to the trust of our strategic partners, an improved balance sheet, and the strong talent we have, which will enable us to meaningfully participate in the next wave of computing as the entire industry pushes for returns on its AI investments. I look forward to updating you, our shareholders, on what this future means for you at our analyst day later this year.

Now, I will hand it over to John to start the Q&A session.

John Pitzer

Thank you, Dave. We will now transition to the Q&A portion of the conference call. A reminder, we ask that each person ask one question and a brief follow-up so that we can address as many questions as possible. Jonathan, please go ahead with the first question.

Q&A Session

Operator

Okay. Today's first question comes from Ross Seymore of Deutsche Bank. Please go ahead.

Q - Ross Seymore

Hi, everyone. Thanks for taking my question. I have two quick parts to my first question, both regarding supply. In the short term, given that Q1 is typically a revenue low point, are the improvements in yield and other actions you are taking sufficient to address the typical seasonal variations for the full year? More importantly, from a long-term supply perspective, you seem more confident about 14A, 18A, customer engagement, and internal roadmaps; when will you decide to ease the constraints on capital expenditures to meet future structurally higher demand through more internal supply?

A - David Zinsner

Thank you for the question, Ross. Regarding short-term supply, certainly, improving yield and throughput are significant drivers of increased supply. In fact, the return on investment (ROI) is very high because it doesn't require any incremental capital. This is an area that Lip-Bu and I are actively working to improve, and we have reason to believe there is a good trajectory there.

That said, when you look at capital expenditures, it is much more nuanced than just "flat to slightly down." In fact, spending in the space (facility construction) has significantly decreased. Therefore, relative to 2025, we are significantly increasing tool spending in 2026 to address this supply shortfall.

In fact, each quarter, we are almost universally increasing wafer starts on Intel 7, Intel 3, and 18A. So all three are improving and getting better each quarter to address supply issues. As I said, we believe the situation will definitely improve in Q2, but that doesn't mean we are completely out of the woods. However, as the year progresses, we believe things will continue to get better

Q - Ross Seymore

Is there any comment on 14A?

A - David Zinsner

Yes. Regarding 14A, Lip-Bu has been very direct with us on this issue. He is only willing to invest in 14A's capacity once we have identified customers, even in the fab, and is only willing to invest in TD expenses or R&D expenses related to 14A. We discussed the likelihood of identifying 14A customers, or ensuring their window will be in the second half of this year and the first half of next year. Therefore, once visibility improves there, we will begin to unlock spending on 14A.

A - Lip-Bu Tan

I can add a bit more. I think in terms of yield improvement, we are seeing a 7% to 8% improvement in yield each month. I think the focus is more on variability, ensuring we can deliver more consistently, and the defect density at the end so that we can ship high-quality wafers to customers. So I think all of this is very important for our PC clients as well as the development of 14A and 18A. Overall, I see improvements, but we have not yet fully reached that industry-leading standard.

A - John Pitzer

Ross, do you have a brief follow-up question?

Q - Ross Seymore

Yes, I do. Regarding gross margin, Dave, you provided many different factors for increases and decreases throughout the year, but you did not mention gross margin. How should we view it? Forgive me, this is a 40% to 60% increment. I know the range you provided is quite broad. Any slightly more precise directional guidance would be helpful. Thank you.

A - David Zinsner

I'm not sure if the math is that good this time. When you look at Q1, the decline in gross margin has two main components. Clearly, the drop in revenue combined with a business that is mostly fixed costs will impact gross margin. But the other part is Panther Lake (Series 3), although the cost structure improved from Q4 to Q1, it still has a dilutive effect on the company's average, and its proportion in the product mix is larger. So it actually has a relatively negative impact on gross margin. This is also part of the reason why we guided down. There are also some mix factors at play.

I think as the year progresses, two things should work in our favor. First, we have improved supply, so this should improve our revenue situation. In addition, the cost structure of Panther Lake will continue to get better. Look, we talked about the incremental improvements we will see in yield each month, and we are also working on throughput. These two things combined should help the cost structure, making this a more value-added product rather than a dilutive product. I think this will largely constitute the story of gross margin this year. There are still mix factors, depending on how things develop, and those mix factors could go in any different direction But what we are primarily focused on in the next 12 months is driving the cost structure of these products we are building to improve margins.

We know that a 34.5% gross margin is by no means an acceptable level. We are actively working to first raise it to 40%, and once we reach there, we will turn to new targets.

A - John Pitzer

Jonathan, please take the next question.

Operator

Okay. The next question comes from Tim at UBS. Please go ahead.

Q - Tim

Thank you very much. Dave, I want to know in the guidance you provided, but I want to know if you could give us a formal extrapolation, like if you could meet all the demands, what would the "unconstrained" guidance for March be?

A - David Zinsner

Yes. That’s a hard number to pin down, Tim, but I’ll tell you that if you look at that $12.2 billion relative to the $13.7 billion we released in Q4, and look at the normal seasonality, it’s within the seasonal range but at the low end of that seasonal range. If we had all the revenue or supply (I should say supply) to meet the revenue target, we would be well above seasonal levels.

A - John Pitzer

Tim, do you have a follow-up question?

Q - Tim

I do. Thank you. Lip-Bu, clearly everyone is very excited about your foundry business. It sounds like we might hear some customer announcements in the second half. But I just wanted to ask you, how do you define success for that business? I think before you came on board, the goal was to become the second-largest foundry by 2030. If you look at most forecasts for the second-largest player, revenue at that time is around $30 billion. Is that still a reasonable target you are pursuing? What do you consider a successful outcome? Thank you.

A - Lip-Bu Tan

Yes. Thank you. Good question. So I think we are determined to drive a world-class foundry business. So I think first, development is clearly on track. We like what we see, and we have streamlined the entire process. Most importantly, we are building an IP portfolio so that we can serve customers. Some IP is critical to serving customers. Another part is yield and improvement. We are seeing trends of improvement, and we are also seeing variability getting better.

I think in the long run, it’s clear that we expect to be in deep engagement with some key customers. We believe that in the second half of this year, they will show us what kind of capacity commitments they are firmly making. So that we can deploy capital expenditures to really build it. So I think overall, this is a service business. We really need to build the trust and consistency that we need to be able to deliver. We had a 0.5 version PDK of 14A in Q1, and then we started engaging with customers about the key products they want to run with us So I believe that throughout this process, I think in the second half of this year, we will be able to secure commitments that will truly drive operational scale.

A - David Zinsner

I think another early indicator of successful foundry operations will be advanced packaging, and even before we start seeing meaningful wafer revenue, we will begin to see this revenue come in. I believe, as I have thought while talking to investors over the past 12 to 18 months, that those opportunities will be measured in hundreds of millions of dollars, while wafer opportunities will be measured in billions of dollars. I want to say that some early customer engagements indicate that we will far exceed $1 billion in many of these advanced packaging opportunities. So this is even more exciting than I expected.

This is because we have very good technology there, highly differentiated, and supporting AI in a special way.

A - Lip-Bu Tan

Yes, I think Foveros T is a very significant differentiator for us. Clearly, we have several customers who are even willing to prepay for substrate costs because substrate supply is very tight, and they are willing to share that with us, which means Joe's company is working with us.

A - John Pitzer

Jonathan, please take the next question.

Operator

Okay. The next question comes from Joe Moore of Morgan Stanley. Please go ahead.

Q - Joe Moore

Yes, thank you. I would like to know if you could talk about the outlook for servers. You mentioned some challenges, with Diamond Rapids lacking symmetric multithreading, and Cooper Rapids being important. Can you give us a timeline for Copper Rapids? And in the meantime, what are your expectations for potential market share changes?

A - David Zinsner

Yes, good question. So I think first, I will centralize and unify the management of data centers and AI, and I have hired [Name] to help us build it. He has built a team, including recruiting some talent. I think what’s more important now is that we are focused on our 16-channel Diamond Rapids, we have streamlined the product roadmap, and another part is accelerating the introduction of Rapids. Rapids will have multithreading reintroduced in our data center roadmap. So overall, I think we are very positive. The team is now in place. The roadmap is very clear, and we are very decisive in doing this, focusing on the 16-channel Diamond Rapids and accelerating the introduction of Rapids.

A - John Pitzer

Joe, do you have a brief follow-up?

Q - Joe Moore

Yes, of course. Thank you. Regarding the product mix for the remainder of this year, are you able to shift wafers from PCs to data centers? Is this something you are considering? It seems like the constraints in Q1 were at their worst point and then improved, but I assume you are still constrained after that. Can you shift the mix towards data centers?

A - David Zinsner

We are definitely constrained, Joe. So what we are doing internally on the client side is focusing on the mid-to-high end and not so much on the low end. Then within the range of our excess capacity, we are pushing all of this into the data center space to meet that customer demand. I think you will see some share shifts as a result because our primary focus is on our key customers, and clearly, we have significant customers in the data center space. We have important OEM customers in both data center and client, and it has to be our priority to allocate our limited supply to these customers.

A - John Pitzer

Jonathan, please take the next question.

Operator

Okay. The next question comes from Ben Reitzes of Melius. Please go ahead.

Q - Ben Reitzes

Hey, everyone, thank you very much. My first question is about seasonal performance for the full year. So Dave, you mentioned that your Q1 performance was below seasonal, and you said that if there was supply, you would be well above seasonal. What does this mean for Q2 to Q4? Should we model above seasonal performance, or is the PC constraint so significant that we shouldn't? Thank you.

A - David Zinsner

Yes, thank you. Yes, I mean we expect that if we can increase supply to the levels we think we can achieve as we enter Q2, the performance for the year will be above seasonal. That is correct.

A - John Pitzer

Ben, do you have a follow-up question?

Q - Ben Reitzes

Sure. I wanted to ask about the situation with hyperscalers. In terms of the momentum you are seeing there, is it primarily driven by hyperscalers, or do you feel that the shortages have mainly impacted them, causing you to be below seasonal? Or is there enterprise demand that you are seeing there as well? Thank you.

A - Lip-Bu Tan

Yes. I think I can answer that question. I believe hyperscalers are very important for us to scale our business, and I have spent a lot of time with hyperscalers. I think there are a few things. First, it is clear from their messaging that CPUs are actually driving a lot of the business around the different workloads they are driving. So I think it is very encouraging to see them willing to commit to long-term agreements to really prioritize their CPU deployments. That is very positive. Secondly, I think they are very excited to work with us, not just on chips but also on software and system-level engagements, which is also very exciting So overall, I think they are very strong.

Their workload, they shared with us what they are looking at and how we can help them. Additionally, ASIC design is also an opportunity for us. They want to build some dedicated chips that include Xeon CPUs. They are also very interested in how to use advanced packaging overall to make it more complete. I think overall, this is a great opportunity for us to collaborate with them.

A - John Pitzer

Jonathan, please take the next question.

Operator

Okay. The next question comes from Stacy Rasgon of Bernstein Research. Please go ahead.

Q - Stacy Rasgon

Hi, everyone. Thanks for taking my question. For my first question, I want to dig deeper into the segments. If I do the math, Mobileye will go up, and Altera foundry revenue could be close to several hundred million dollars. I need both DCIA and client to decline quite significantly. If the client declines more, I mean maybe DCIA declines in the high single digits, and the client declines in the mid-teens. I want to ask, first, is this true? Second, given where the demand is and where you prioritize, why would the data center decline so much? Like why would I expect data center unit shipments to decline? It seems like they must decline significantly in Q1.

A - David Zinsner

Yes. I mean, both will decline due to supply constraints. Obviously, we are shifting as much as we can to data centers to meet high demand, but we cannot completely abandon the client market. So we are doing our best to support both. Clearly, we need to work on resolving this supply issue. I do believe that Q1 is the trough. We will improve supply in Q2. Part of the challenge is that in the third and fourth quarters of 2025, we relied on supply to survive, but also consumed a significant portion of finished goods inventory.

Unfortunately, the current inventory levels have dropped to 40% of peak levels. So we do not have that to rely on. So it is actually what is called "hand to mouth," what we can get from the foundry and what we can give to customers, that is how we manage it.

A - John Pitzer

Stacy, do you have a follow-up question?

Q - Stacy Rasgon

I do. Thank you. Just wanted to follow up. I mean, you have your own factories, why are you in such an inventory situation? And then, like, I understand the overall concept about finished goods versus other things. But I mean, you have $11.6 billion in inventory. However, it is not showing up in the right place at the right time for shipment, how did that happen?

A - David Zinsner

This has largely happened. I would tell you, Stacy, that the biggest thing is that if you look back at the outlook from about six months ago, the core numbers absolutely looked like they would increase. But the unit numbers are not expected to increase. Every hyperscale customer we've talked to has been signaling this. Clearly, it ramped up quickly in the third and fourth quarters. Just before this conference call, I spoke with several of them, and it feels like this will be a story we continue for several years. Yes, our advantage is that we do have our own fabs, so we can squeeze out supply as much as possible, which is what we are working on. But we did not anticipate that the unit numbers in the data center would increase so significantly in terms of managing supply.

A - John Pitzer

Jonathan, please take the next question.

Operator

Okay, our next question comes from Vivek Arya of Bank of America Securities. Please go ahead.

Q - Vivek Arya

Thank you for taking my question. First, Lip-Bu, I'm curious when you think Intel should start to see recognition for its external foundry efforts? Because you mentioned that you might hear about orders in the second half of this year. I assume you would start building capacity for that after, right, around late this year or next year. So when do you actually expect to start seeing meaningful revenue from these customers? I think you mentioned that building this business will require incremental resources. So how much external foundry revenue does Intel need to consider this business a success? When can you get there? Is it 2027, 2028? Or even later?

A - Lip-Bu Tan

Yes. Good question. I think first, the engagement around 14A with our potential external customers is currently very active. Several key customers are working with us. We hope they will really get through the 0.5 PDK milestone basis and then start looking at test chips to see how our yield performance is, which will be a process of working with them. Then I think in the second half of the year, they will start to feel satisfied, and then they will ask us, okay, now this is the specific product we want to run with your foundry and production, which will give us guidance. At that point, my discipline is that I will only start to really build and then expand foundry capacity once they have a commitment on yield.

Another part is that in parallel, they also give us an IP list, which if it's mobile-related, must have low-power IP. If it's data center-related, it will obviously be performance, connectivity, all the things we need to have ready so that we can serve as a service to customers. So the readiness of IP and our yield readiness is parallel. Then once they start to feel satisfied, okay, now this product, this is the volume we want to run with you, that's how you start building. So in terms of 14A, actually, the so-called risk production is in late 2027, and true mass production is in 2028, which aligns with the timeline of leading foundries. **

I'm just saying that we might provide you with more information around all these things at the analyst day we mentioned in the second half of the year.

A - John Pitzer

Vivek, do you have any follow-up questions?

Q - Vivek Arya

Yes. Thank you, John. For my follow-up question, I'm curious, what do you think the server CPU TAM will be in 2026? How much of that will be X86? How much will be ARM? I mean, if your supply is constrained, is the entire industry supply constrained? Do you think that any part you can't supply, all that market share will flow to your X86 competitors and every AI community building on ARM servers? So how much do you think your supply... market growth will be? When do you think your server CPU supply constraints will be lifted? Thank you.

A - David Zinsner

Okay. Maybe I'll start first. So I think this demand we see is primarily an x86 phenomenon because it is, in many ways, an upgrade cycle around old networks that need to communicate with AI systems in some way, and the performance hasn't reached the required level. So I really think this is about X86. Of course, we do have another competitor in this space, and we will be competing for position from a market share perspective. I think as we move through this year, we will make significant progress on the supply side. So I wouldn't envision this ultimately becoming a fundamental driver of market share; it's really about the products, talking about the launch of the 16-channel Diamond Rapids and accelerating the introduction of Coral Rapids.

As we look at the market share dynamics over the next few years, these will be the most important things for us.

A - Lip-Bu Tan

Yes, I think from my side, obviously, the hyperscalers and high-end ODMs are critical for us in this regard. We are basically working with them. Their preference is for CPUs from Intel, which is very clear from them. They will try to get as much as they can from us. I think that's the key driver.

A - John Pitzer

Jonathan, please take the next question.

Operator

Okay, our next question comes from C.J. Muse of Cantor Fitzgerald. Please go ahead.

Q - C.J. Muse

Yes, good afternoon. Thank you for taking my question. I think this is a follow-up to Stacy regarding supply issues. Given your bullish comments on AI-driven demand and how you are constrained by supply, while your peers TSMC and Samsung are actively arranging equipment deliveries, are you concerned that if you wait until the end of 2026 to place orders, the lead times may be longer than you expect? As part of that, why aren't you more proactive about it now?

A - David Zinsner

Yes. Maybe I don't know if this is the answer you want to hear, but what I mean is that we are actively acquiring tools for Intel 7, 10, Intel 3, and 18A, and that is happening. We will increase the wafer start volume on these nodes as aggressively as possible. What we are holding back is 14A because 14A is really tied to foundry customers, until we know we have customers who will accept that demand; otherwise, it doesn't make sense to build a lot of capacity on that. So that is the discipline we will have. A lot of things regarding supply, first and foremost, is our short-term focus, which we believe we can gain significant supply by better utilizing our existing tools and facilities, improving yield, and reducing cycle time, and we are actively working on this.

We believe there are many opportunities to improve our supply just through these two things, and honestly, this does not require capital expenditure. This may be what makes us more unique relative to other foundries right now.

A - John Pitzer

C.J, do you have a follow-up question?

Q - C.J. Muse

Yes, John, thank you for Dave's answer. In the press release, you talked about demonstrating the technical feasibility of future HVM (high-volume manufacturing) on High Numerical Aperture (High NA). So I'm just curious, is this something you are still considering for 14A, or is it more about the adoption of 10A? Thank you.

A - David Zinsner

This will be part of our 14A process. Of course, 14A will have different variants, but High NA is aimed at 14A.

A - John Pitzer

Jonathan, shall we move to the next question?

Operator

Okay. The next question comes from Harlan Sur of JP Morgan. Please go ahead.

Q - Harlan Sur

Yes, good afternoon. Thank you for taking my question. Lip-Bu, as you look ahead to 14A, you talked about engineering engagement with customers. Typically, large mature semiconductor companies around the world want to run their own test chips to evaluate a new foundry node, and they usually wait until PDK 0.4 to start their test chip designs. It seems with your release of PDK 0.5, they can start their test chip designs now. So I guess the question is, have customers already started their test chip designs, or are they even further along, with customers now running their own 14A test chips?

I mean, for them to make decisions unfortunately in the second half, they need to run their test chips fairly quickly. So please give us an update on that.

A - Lip-Bu Tan

Yes, good question. So I think you are absolutely correct. Several clients have already been in contact regarding PDK 0.5, and they are looking at test chips. More importantly, they will be running specific products in our foundry. In that area, we are working with them, and of course, they want to know about capacity and pricing, which are all under discussion now. So that’s why I mentioned that in the second half of this year, they will start to be satisfied, and then they can say, okay, now we need this volume, we need your specific factory to do this. Another part is whether we have all the right IP to serve them.

So these are the things we are working on in parallel with their supply chain and their design teams. This is a very complex step, and we are very familiar with it. We are working in the right way.

A - John Pitzer

Harlan, do you have any follow-up questions?

Q - Harlan Sur

Yes. Thank you. Regarding your server product portfolio, I apologize if I missed this earlier, but Clearwater Forest, right? Your E-core cloud workload optimized server platform. Its goal is to be the first server platform using your 18A manufacturing and ramping up in the first half of this year. However, you mentioned changes in the server roadmap, focusing on more performance-oriented products. So is the team still supporting Clearwater Forest, or is it now solely focused on Diamond Rapids? Has the team already Tape-out or Tape-in your next-generation Xeon 7 Diamond Rapids products? What are the initial thoughts on the ramp-up time for Diamond Rapids?

A - David Zinsner

Yes. So to answer your question, yes, we continue to support that. I also mentioned focusing on the 16-channel Diamond Rapids, which is a focus on the high-end of Diamond Rapids so that we can really concentrate on delivering differentiated competitive products. Then another part is, as I mentioned in the past, this multithreading is very important for driving performance, and we need to really get that out, it takes time to have it, and we will have it in Rapids. Now the question is how to accelerate it? They are bringing it in early because customers are really excited about it. So, can you bring it in earlier? That’s why I am working with him and his team to see how much we can really push this acceleration to bring it to market earlier for the customers.

A - John Pitzer

Jonathan, we have time for one more question.

Operator

Okay. So the last question today comes from Aaron Rakers of Wells Fargo. Please go ahead

Q - Aaron Rakers

Yes, thank you for answering the question. If possible, I have two questions. But regarding memory and the situation we see in the market, I'm curious how you view customer reactions to memory, and whether there is potential demand destruction in the PC market? Just curious what you are seeing in this regard, given that Lunar Lake demand is clearly more long-lasting and stronger, how significant is the impact of memory pricing on gross margins?

A - David Zinsner

Yes, good question. So I think one of the very big challenges the industry faces is memory constraints and pricing. So I think we also listen to the voice of the customer, some of the big players in OEMs and the hyperscalers, they have more channels into memory allocation. So we hear from them. Secondly, I think some of the smaller players, they really struggle to get memory. So I think that’s very important for us, for Dave and me, how to allocate and how our sales do well in allocating to the right customers. No, we don’t want to send CPUs to them, but they lack memory, and they can’t complete their products. So we need to try to do this right. Having that intelligence and feedback from customers working with us is very important so that we can meet their demands. Dave?

A - David Zinsner

Yes. I think on the Lunar Lake side, I think we have what we need based on current forecasts, and of course, there can always be upside, and then we will need more memory, which will impact gross margins. But we are relatively aggressive in getting memory early on. So I feel we are in a relatively good position there. That said, those margins are low because the memory is in the package. So that’s also an impact on our gross margins. But I think we are largely where we thought we would be a quarter or two ago.

A - John Pitzer

Aaron, do you have a brief follow-up?

Q - Aaron Rakers

I do. I’ll be quick. I’m curious about custom ASICs; you mentioned reaching a $1 billion run rate business. How do we view that progress? How broad is the customer base for that opportunity? Thank you.

A - Lip-Bu Tan

Yes, good question. I think Dave mentioned earlier the $100 billion TAM market opportunity, and we are excited. We are already at a $1 billion run rate. There is strong demand, and customers are very excited about what we have in CPU, Xeon, and AI-related momentum, so they are building more dedicated chips for AI, networking, and experimentation. I think we will continue to work on that part. More importantly for them is advanced packaging, which makes it more attractive. That’s Intel’s advantage; we can do both to provide customer satisfaction. So I think this is a great opportunity for us

Finally, thank you all for joining us today. As we move forward, I remain focused on strict execution and deep collaboration with our clients to seize the meaningful opportunities created by the AI era. While there is still much to be done, we are confident in the foundation we have built and the progress we are making, and we look forward to providing another update in April.

Operator

Thank you, ladies and gentlemen, for participating in today's meeting. The meeting is now concluded. You may disconnect. Have a great day