How long can the feast of the U.S. credit market last?

The U.S. credit market has been heating up since 2025, with credit spreads compressing to historical lows and corporate bond issuance reaching new highs during the same period. The annual corporate bond issuance is expected to reach USD 2 trillion in 2024-2025, with IG bond issuance hitting a record in 2025. Despite the low market risk premium, the credit return structure has shifted to being dominated by coupon payments, leaving investors facing a dilemma of low risk compensation. Geopolitical risks and other uncertainties have not significantly impacted market sentiment, but potential risks in the credit market are accumulating

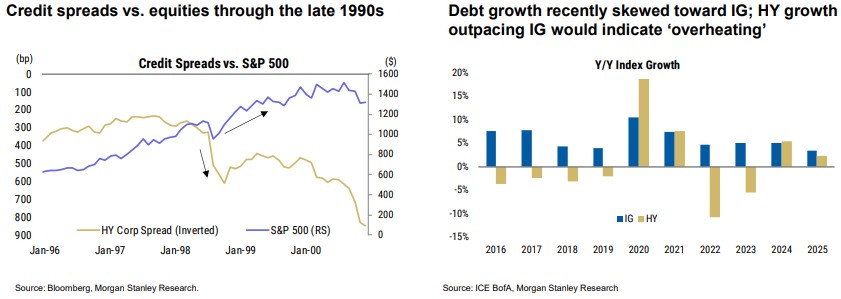

Since 2025, the U.S. credit market has continued to heat up, entering a booming state at the beginning of this year. Whether in the investment-grade (IG) or high-yield (HY) market, credit spreads have been compressed to near historical lows: the IG corporate bond spread (OAS) once approached the extremely low levels of 1998, and the HY corporate bond spread is also in a historically narrow range.

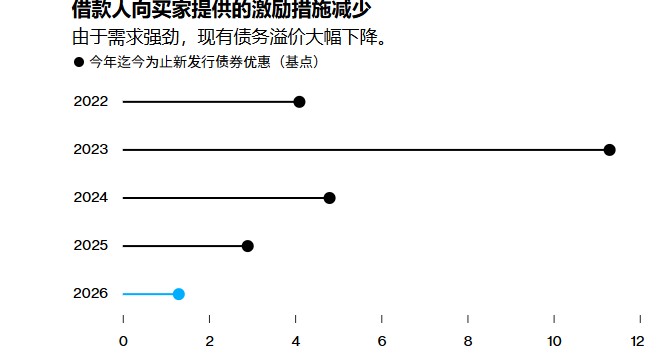

The primary market issuance has also been exceptionally active, with low financing costs attracting companies to launch a wave of bond issuance: since the beginning of the year, the scale of corporate bond issuance has reached a record high for the same period, with the subscription multiple for new bonds significantly increasing, and the new issuance premium being compressed to extremely low levels, with some transactions even approaching zero profit. The annual corporate bond issuance amount for 2024-2025 is projected to be $2 trillion, significantly higher than the $1.5 trillion for 2022-2023; among them, the issuance of corporate IG bonds in 2025 is expected to reach a record $1.64 trillion, and in 2026, driven by AI capital expenditures, total supply is expected to refresh the record to $1.8 trillion.

In addition, the recovery of mergers and acquisitions (M&A) activities has also boosted financing demand, leading the U.S. credit market to experience a supply peak driven by both AI infrastructure and corporate mergers.

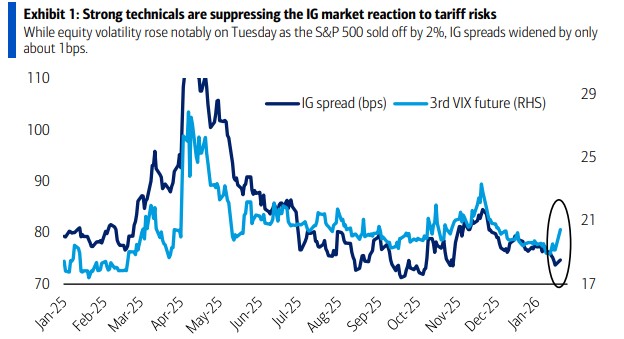

In the current context of extremely narrowed credit spreads and market risk premiums compressed to very low levels, the safety buffer of credit assets has significantly thinned, and the U.S. credit market has entered a low-tolerance phase. Currently, the premium on newly issued bonds is only 1.3 basis points, far lower than last year's 3 basis points. The sources of credit returns are changing: previously, returns came from both coupon payments and capital gains from spread compression; currently, with limited further space for spread narrowing, the structure of credit returns is rapidly shifting to be dominated by coupon payments.

Credit returns are highly dependent on coupon payments and time rolling, and with limited further space for spread compression, once risk events significantly increase, the asymmetry of spread repricing will be significantly amplified. However, recent geopolitical risks, uncertainties regarding Trump tariffs, and rising threats to the independence of the Federal Reserve have led the credit market to remain oblivious to risks. For the IG market, these risks are offset by strong investor demand, showing significant complacency. Investors currently face a dilemma of not wanting to miss out on the rising market (FOMO) while being forced to accept extremely low risk compensation

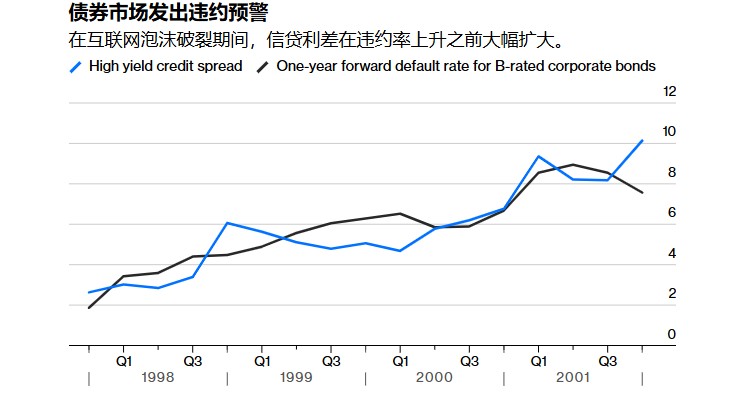

On the other hand, hidden risks in the credit market are accumulating, and the bond market's warning function as the "canary in the coal mine" is weakening. Over the past two decades, credit spreads have typically been able to accurately predict default risks. However, with the explosive growth of the private credit market—over $200 billion in new private loans added each year for the past two years—a large amount of high-risk debt (whose average credit quality is comparable to B-rated speculative bonds in the public market) is being hidden from public market visibility. The lack of transparency, liquidity, and effective market pricing mechanisms in the private credit market is gradually undermining the warning function of traditional bond markets based on credit spreads.

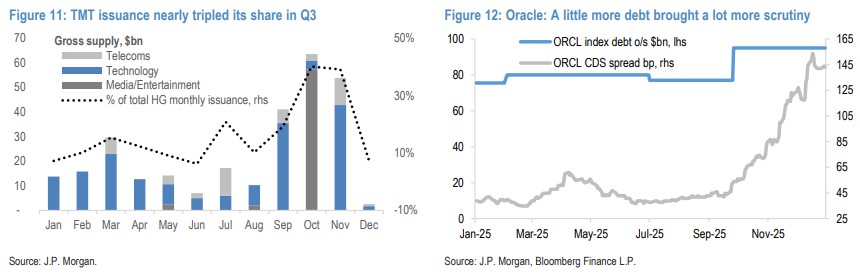

In addition, last year's AI boom drove American tech giants to go on a borrowing spree, raising market concerns about debt issues. The market is highly reliant on the AI narrative, and once faced with earnings falling short of expectations or risks of technological iteration, it will directly test the refinancing capabilities of issuers and the absorption capacity of the bond market. Significant valuation corrections and widening spreads on tech investment-grade bonds will quickly transmit risks to the private credit funds, banks, and pension systems that provide financing for them.

Why is the market so hot?

Despite the initially tight valuations, the logic supporting this round of market activity remains solid, and both the investment-grade (IG) and high-yield (HY) markets are still expected to achieve positive excess returns. First, the U.S. economy has shown unexpected resilience, inflation has eased, and combined with expectations of Federal Reserve interest rate cuts (albeit at a slower pace), the macro "Goldilocks" environment creates a perfect credit environment, sufficient to maintain spread fluctuations within a range.

Moreover, duration protection is significant. Since 2022, the effective duration of the IG and HY markets has significantly decreased, with IG at a near 10-year low and HY reaching a historic low; even if spread premiums rise again, the impact on prices is naturally smaller.

Unlike previous cycles, a core driver of this round of credit expansion is AI. AI capital expenditures exhibit a desensitization to the macro economy, meaning that regardless of interest rates, tech giants will maintain substantial investments to seize computing power. By 2026, the bond issuance scale related to AI is expected to reach $500 billion. This rigid demand, combined with ample cash in investors' hands, allows the primary market to easily absorb a massive supply

The short-term health of corporate fundamentals provides support. Although leverage levels have risen, most companies still have strong interest coverage, and profitability is expected to improve in 2025. Rating migration data shows that the trend of investment-grade bonds migrating internally to higher ratings continues, with the proportion of BBB-rated bonds dropping to a ten-year low, which provides a certain sense of security for the market from a credit fundamental perspective, allowing investors to temporarily overlook the risks of long-term debt accumulation.

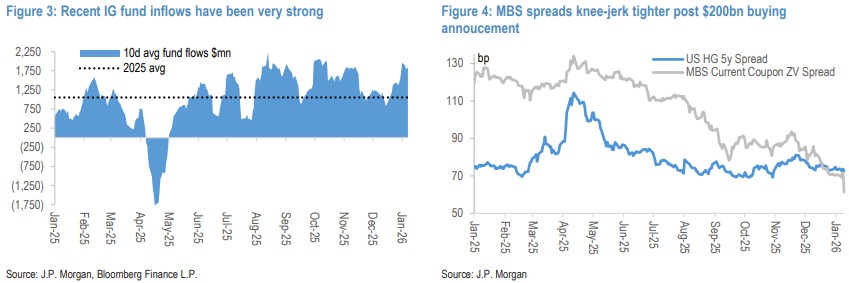

In addition, from a funding perspective, despite a surge in corporate bond supply, the demand from insurance companies and pension funds for long-duration assets remains strong, with continued robust inflows into mutual funds and ETFs, and investors holding a large amount of cash, resulting in extremely high subscription multiples for newly issued bonds; especially in the context of an expected steepening yield curve, high-grade corporate bonds remain the preferred choice for locking in yields. Furthermore, the Trump administration's support for the Government-Sponsored Enterprises (GSEs) plan to purchase $200 billion in MBS also indirectly benefits investment-grade credit spreads.

Follow-Up Attention

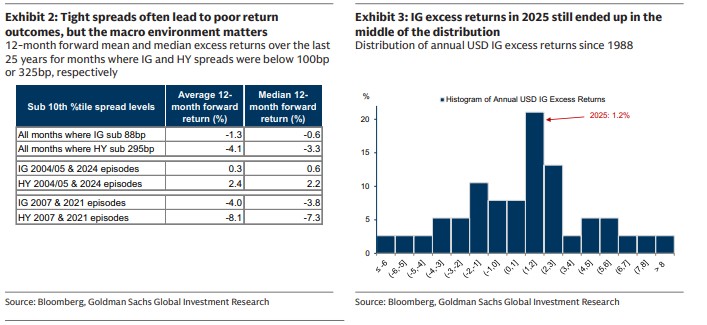

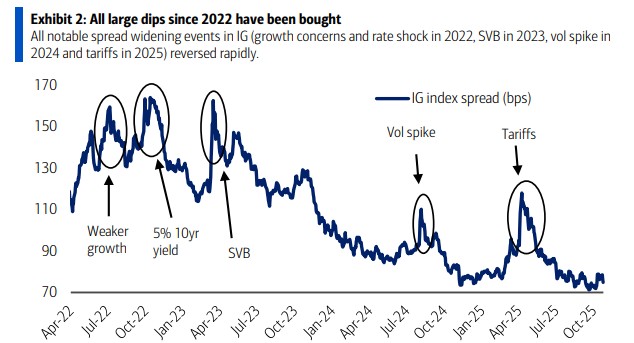

History shows that during periods of extreme spread compression, negative shocks often lead to a sharp rise in credit spreads and significant negative returns. For example, the low points of spreads in early 2007 and late 2021 were both followed by severe market adjustments.

However, currently, even with starting spreads extremely narrow, the credit market still has the capacity to achieve positive excess returns. The reasons are the strong macro backdrop, improvements in corporate fundamentals, and lower duration risk. As long as a recession does not occur, coupon income will be sufficient to offset capital losses caused by slight fluctuations in spreads.

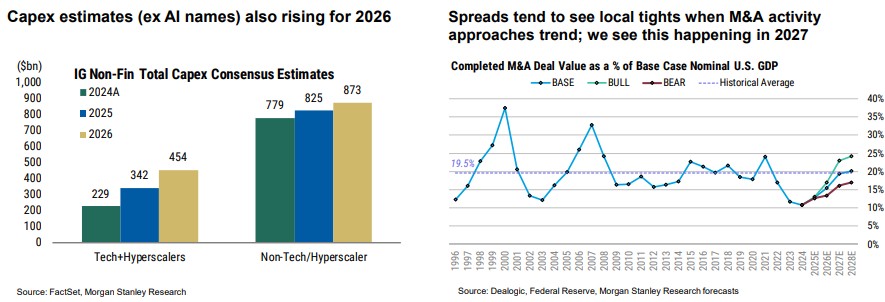

Caution is needed regarding the massive supply driven by AI and mergers and acquisitions leading to wider IG spreads. Due to the excessive supply pressure from AI capital expenditures and M&A activities, investment-grade spreads are expected to widen to around 95bp by 2026, resulting in near-zero excess returns for the year. In contrast, high-yield bonds (HY) may perform better than investment-grade bonds due to relatively controllable supply and benefits from economic growth.

Short-term catalysts: Pay attention to the earnings season for tech stocks after January 29, which will be a key point to verify whether AI spending can be absorbed by the market. If the AI capital expenditure plans announced by tech giants exceed market expectations, or if the resulting bond issuance exceeds the market's absorption capacity, spreads may rebound rapidly.

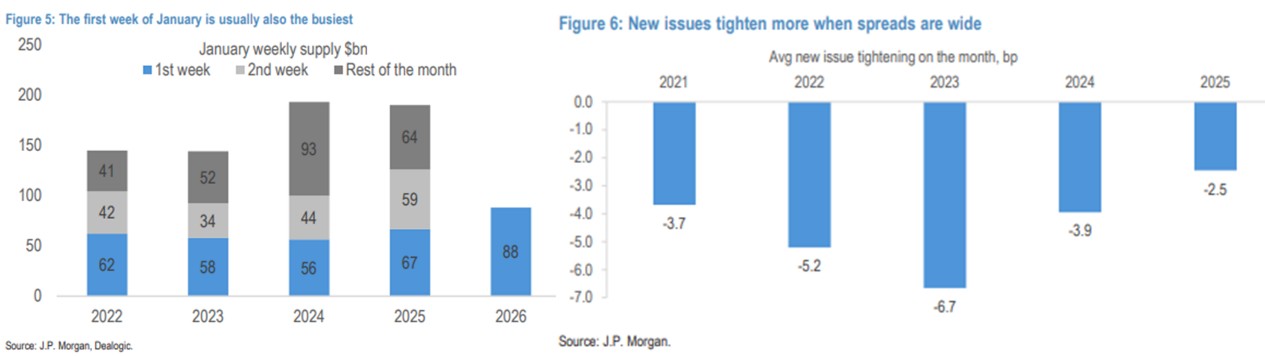

Also, watch for the fading of the "January effect": spreads often narrow at the beginning of the year and may subsequently rebound. Investors should be cautious of spread revaluation when the supply peak arrives. However, even with significant pullbacks, the market has recovered within a month since 2022.

Risk Warning and Disclaimer

The market has risks, and investment requires caution. This article does not constitute personal investment advice and does not take into account the specific investment goals, financial situation, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article are suitable for their specific circumstances. Investment based on this is at your own risk.