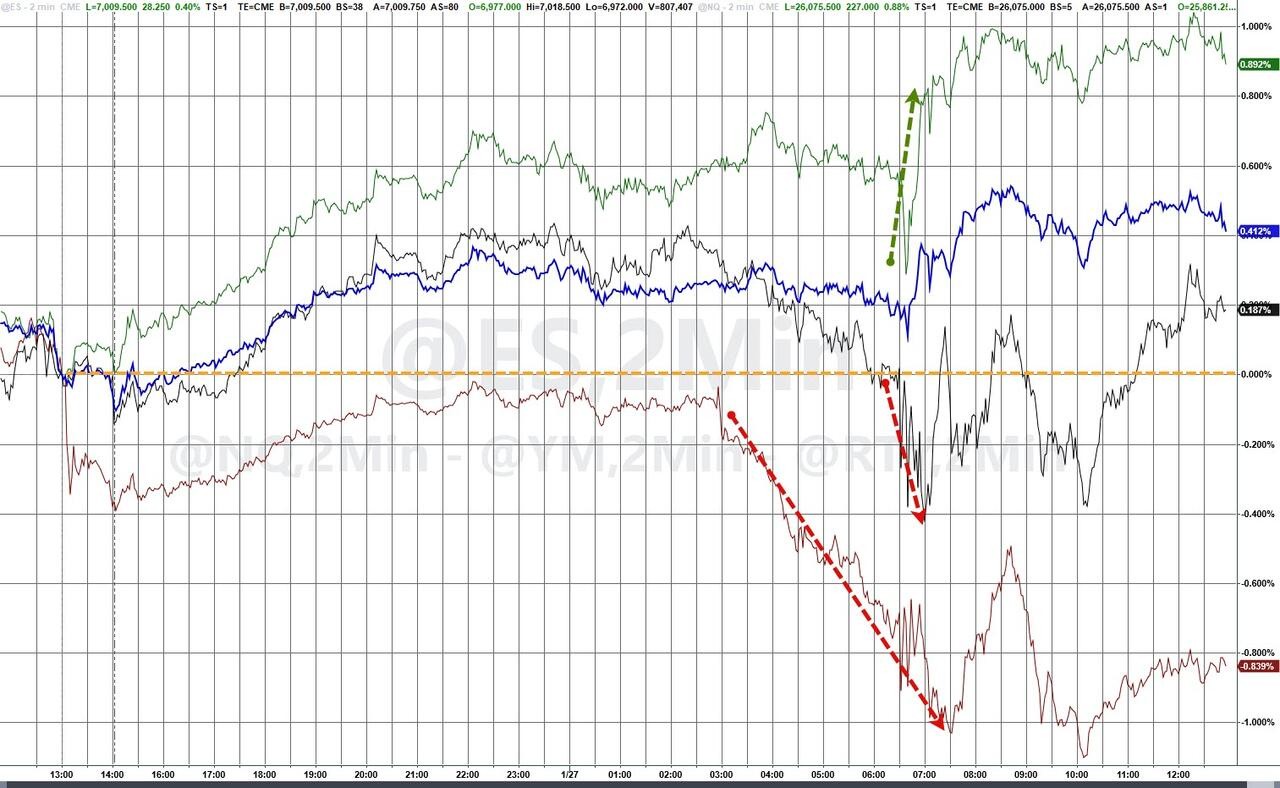

Global stock markets rose ahead of tech earnings, with Nasdaq futures up 0.6%. Gold briefly returned to 5,100, and silver rebounded to 110 USD

標普收創最高紀錄;醫保巨頭 UnitedHealth 跌近 20%、領跌道指成分股;財報公佈前,微軟漲超 2%、特斯拉跌 1%;美光漲超 5%;康寧漲超 15%;德州儀器和希捷科技盤後曾漲 9%。美元指數跌超 1%;日元三日累漲 4%,歐元和英鎊創 2021 年來新高,離岸人民幣近三年來首次盤中漲破 6.94。原油尾盤一度漲超 3%。現貨黃金盤中漲超 3%;盤中期銀曾跌超 10%、現貨白銀一度漲超 9%。

微軟等多家美國科技巨頭髮布財報前,市場對人工智能(AI)發展的樂觀預期持續發酵,兩大美股指保住漲勢,而特朗普政府提議明年維持對私人醫療保險計劃 Medicare 的支付水平幾乎不變、令投資者大失所望,醫保巨頭大跌,拖累另一主要股指道指回落。

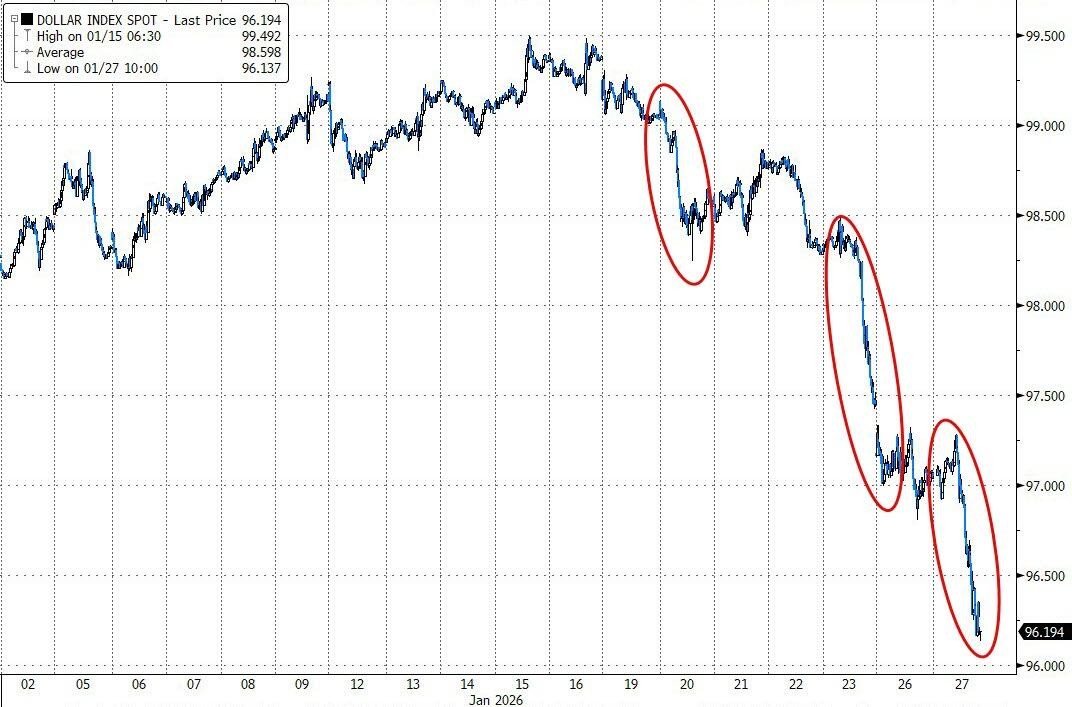

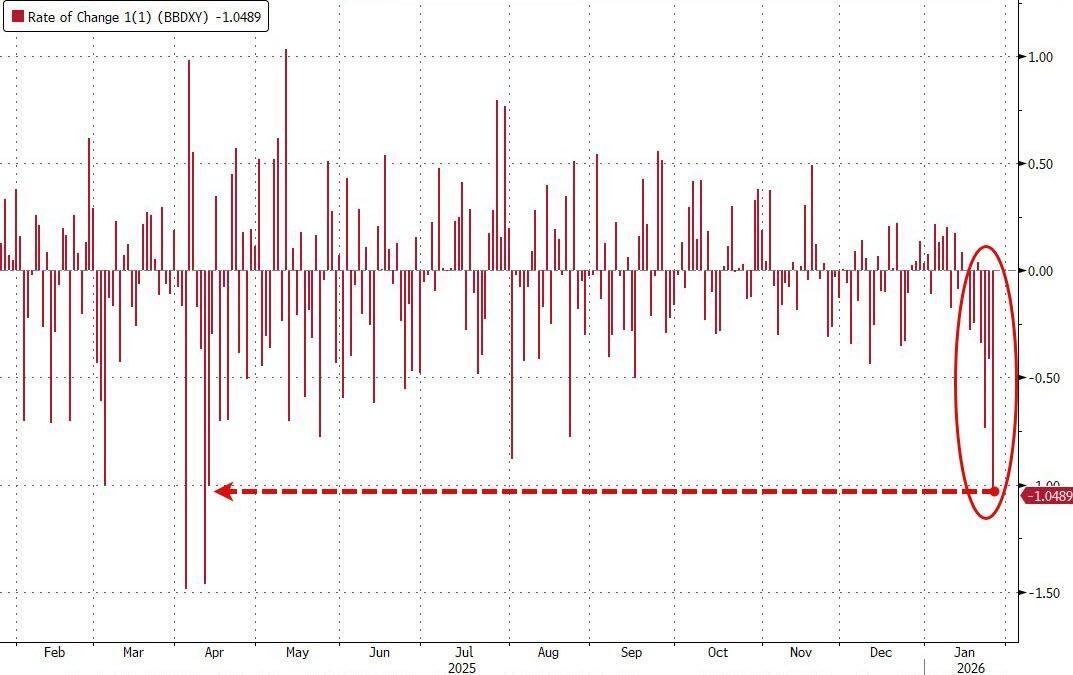

美國總統特朗普稱美元 “表現出色”,並預計匯率將波動,不擔心美元貶值。美元指數週二加速下跌至約四年來最低谷,創去年 4 月以來最大的四日和六日累計跌幅。

彭博美元現貨指數創去年 4 月特朗普公佈對等關税以來最大六日跌幅

隨着美國在中東地區加強軍事部署、美元跌幅超過 1%,原油盤中拉昇,漲幅擴大到 3% 以上。據新華社報道,美國將在中東舉行空軍戰備演習。據央視,美國被曝向以色列通報對伊朗行動準備進展。

評論認為,交易員持續關注美國可能對伊朗採取行動的可能性,冬季風暴導致美國本土原油產量下降,均對油價構成支撐。BOK Financial 的分析師 Dennis Kissler 在報告中指出:“雖然天氣造成的生產中斷是暫時的,但俄克拉荷馬州、路易斯安那州和德克薩斯州冰雪濕滑的天氣狀況將減緩生產恢復的速度。” 他表示,同時,伊朗局勢以及俄烏和談缺乏進展 “支撐着油價”。

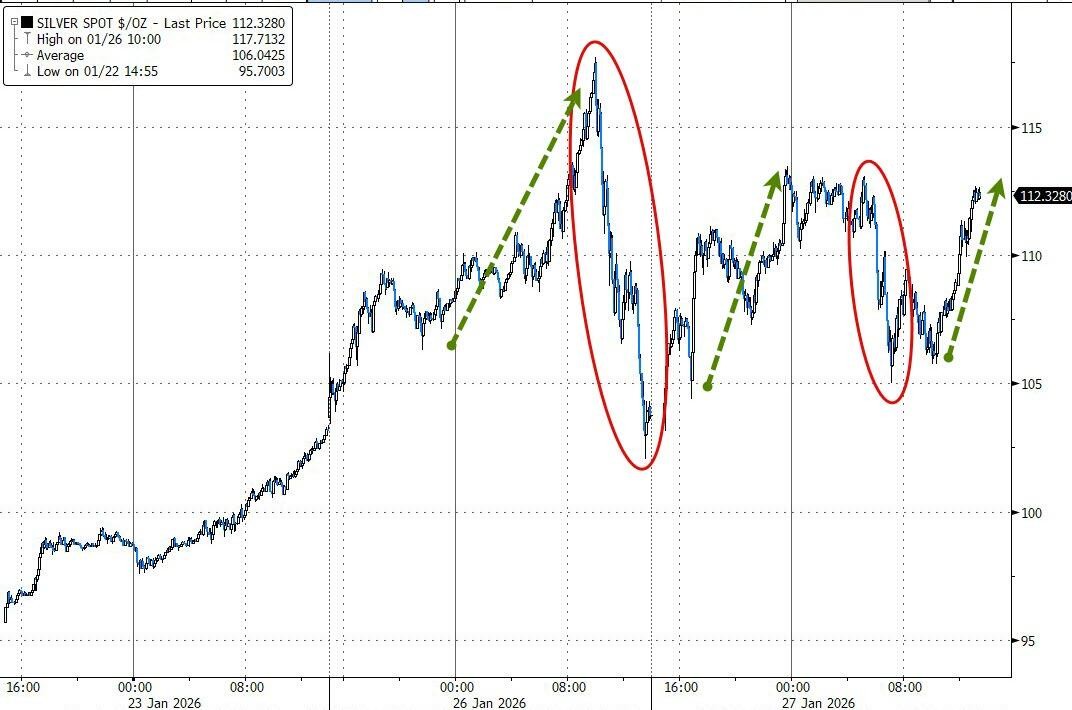

貴金屬漲跌不一。美元尾盤跌幅擴大之際,黃金進一步上行,再創盤中歷史新高,現貨黃金曾漲超 3%。盤中曾跌超 9% 的紐約期銀跌幅收窄到 3% 以內,現貨白銀的盤中漲幅曾擴大到 8% 以上。花旗預計現貨白銀價格將在三個月內創出每盎司 150 美元的新高,令其 1 月累計將近 50% 的歷史性漲勢再上一個台階。花旗分析師預計,中國強勁的買勢將得以持續,直到白銀相對黃金的價格按歷史標準顯得貴為止。

特朗普講話後美元跌幅擴大、現貨黃金加速上漲並創歷史新高

美國 1 月諮商會消費者信心指數超預期大幅下降至 2014 年來低位,數據公佈,美債價格普遍上揚、收益率刷新日低,後長債的收益率回升、短債的仍下行,收益率曲線趨陡。美聯儲決議前夕,美國國債價格繼續小幅波動。隨着就業市場趨穩,聯儲官員在經歷數月分歧後料將恢復一定的共識,市場預期美聯儲將暫停降息週期。

市場焦點已轉向週三的美聯儲利率決議,以及即將陸續出爐的大型科技公司財報,後者將檢驗本輪由人工智能驅動的股市上漲是否具備持續性。高盛 CEO 所羅門在分析全球市場環境時指出,刺激性財政政策、支持性的監管趨勢與基調,以及大規模的人工智能投資,共同構成了當前市場的主要推動力。他表示:

“從經濟角度來看,形勢發展良好。目前來看,總體形勢相對樂觀,但這並不意味着不會出現問題。”

SWBC 的高級副總 Chris Brigati 指出,鑑於經濟仍展現非凡韌性,美聯儲聲明料將強調未來政策決策將基於數據。他同時表示,本週 “科技七巨頭” 財報基調應保持穩健,分析師上調盈利預期也顯示市場信心正在增強。Brigati 稱:

“隨着 2026 年推進,本週財報將成為決定市場短期基調的關鍵節點。歷史表明,強勁的 1 月往往為全年定調,而投資者的心理發揮很大的作用。”

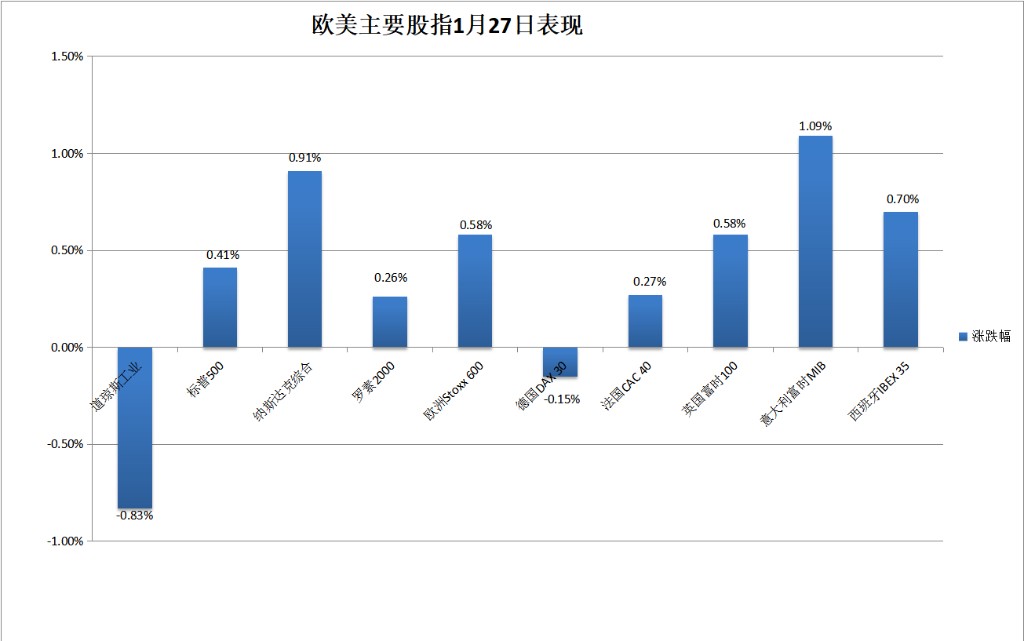

標普收創最高紀錄,和納指五連陽;道指回落,醫保巨頭 UnitedHealth 跌近 20%、領跌道指成分股;財報公佈前,微軟漲超 2%、特斯拉跌 1%;增加 NAND 製造投資的美光漲超 5%;和 Meta 簽下光纜大單的康寧漲超 15%。指引優異的德州儀器和希捷科技盤後曾漲 9%。

美股基準股指:

- 標普 500 指數收漲 0.41%,報 6978.60 點,創收盤最高紀錄。

- 道瓊斯工業平均指數收跌 408.99 點,跌幅 0.83%,報 49003.41 點。

- 納指收漲 0.91%,報 23817.098 點,刷新 11 月 3 日以來高位。

- 納斯達克 100 指數收漲 226.534 點,漲幅 0.88%,報 25939.744 點。

- 羅素 2000 收漲 0.26%,報 2666.7 點,在兩連跌後反彈。

- 納斯達克科技市值加權指數收漲 1.24%,報 2416.4314 點。

主要美股指週二表現不一,標普和納指繼續走高,道指轉跌,羅素 2000 連續三個交易日漲幅不及標普

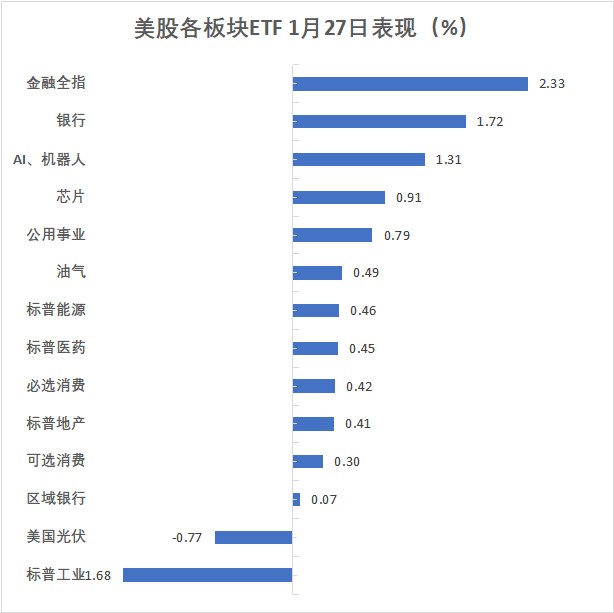

美股行業 ETF:

- 半導體 ETF 收漲超 2%,漲幅居首,而醫療業 ETF 跌近 1.7%。

科技七巨頭:

- 美國科技股七巨頭(Magnificent 7)指數漲 1.14%,報 209.16 點。

- 亞馬遜收漲 2.63%,微軟漲 2.19%,蘋果漲 1.12%,英偉達漲 1.10%,谷歌 A 漲 0.39%,Meta 漲 0.09%,特斯拉跌 0.99%。

芯片股:

- 費城半導體指數收漲 2.40%,報 8117.18 點,收創最高紀錄。

- 英特爾收漲約 3.4%,博通收漲超 2.4%,台積電收漲 1.69%,AMD 漲 0.29%;宣佈計劃投資約 240 億美元、在新加坡現有 NAND 閃存製造工廠內啓動一座先進晶圓製造工廠建設後,美光科技收漲逾 5.4%.

- 盤後各自公佈第一季度和第三財季的指引高於市場預期後,德州儀器和希捷科技盤後均曾漲約 9%。

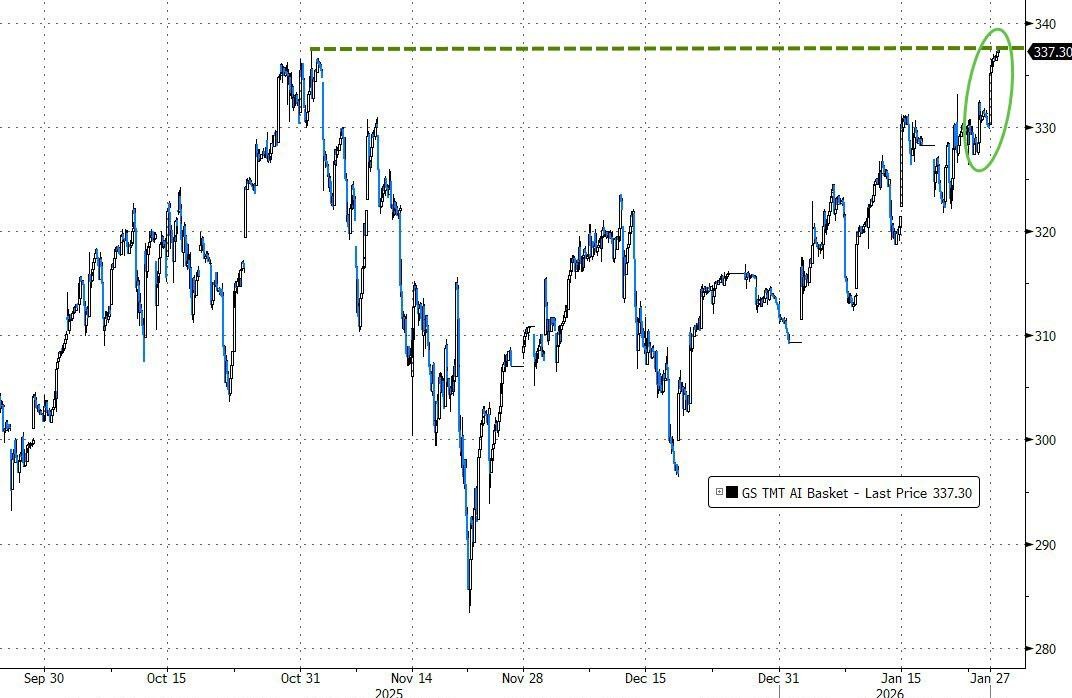

AI 概念股週二總體跑贏大盤

醫療保險股:

- UnitedHealth(UNH)收跌 19.6%,領跌道指成分股,CVS Health Corp.(CVS) 收跌近 14.2%,Humana Inc.(HUM) 跌 21.1%。

UNH 跌近 20%,在道指成分股中跌幅居首

中概股:

- 納斯達克金龍中國指數收漲 0.48%,報 7866.61 點。

- 虎牙收漲 19.3%,金山雲漲近 8.8%,世紀互聯漲超 4%,百勝中國漲超 3%,百度漲超 1%,阿里漲近 0.8%。

公佈財報的個股:

- 公佈四季度盈利和 2026 年指引高於預期、季度分紅上調 20% 及 60 億美元回購計劃後,通用汽車(GM)收漲近 8.8%。

- 四季度業績優於預期的物流巨頭 UPS 收漲 0.2%。

- 公佈四季度 EPS 創十多年新高但若剔除出售數據航空業務則 EPS 由盈轉虧後,波音(BA)收跌 1.5%。

- 四季度業績遜於預期的美國航空(AAL)收跌 7%。

波動較大的個股:

- 報道稱 Meta 與其達成協議投入 60 億美元購買數據中心光纜後,康寧(GLW)收漲近 15.6%。

- 參與美國國防部高達 150 億美元的合同後,太空公司 Redwire(RDW)收漲 29.7%。

- 宣佈計劃裁員約 15%、將更多資源投入 AI 相關職位和戰略中後,社交媒體 Pinterest(PING)收跌 9.6%。

泛歐股指兩連漲、靠近紀錄高位,銀行板塊漲近 2% 領漲,安踏宣佈將收購 29% 股權後彪馬漲 9%。

泛歐股指兩連漲。歐洲斯托克 600 指數收漲 0.58%,報 613.11 點,連續兩日刷新 1 月 16 日上上週五報 614.38 點以來高位,靠近 1 月 15 日所創收盤歷史最高位 614.57 點。

主要歐洲國家股指週二大多上漲,英意西股兩連漲,富時意大利綜合股價銀行指數收漲 1.67%,銀行股帶動意股漲超 1%,兩連跌的法股反彈,而週一反彈的德股回落。

斯托克 600 各板塊中,銀行收漲 1.8%,成分股中,意大利裕信銀行漲 2.13%,法國巴黎銀行漲 1.82%,荷蘭國際集團(ING)漲 1.80%;科技板塊收漲近 0.4%,荷蘭上市的歐洲最高市值芯片股 ASML 收漲 3.36%,而德國上市的 SAP 跌 2.69%。

個股中,安踏將獲得控股權、成為其最大股東的彪馬收漲 9.02%。

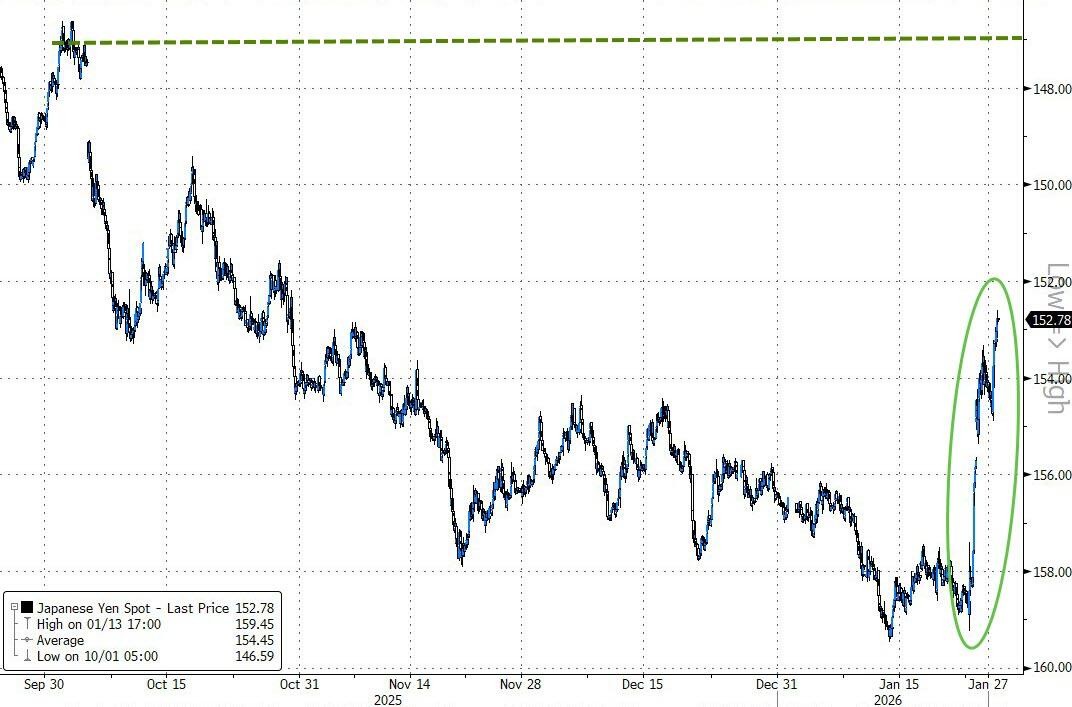

美元指數跌超 1%,創去年 4 月特朗普宣佈關税以來最大四日跌幅;日元三日累漲 4%,歐元和英鎊創 2021 年來新高,離岸人民幣近三年來首次盤中漲破 6.94;比特幣盤中漲超 2% 重上 8.9 萬美元。

美元指數:

- ICE 美元指數(DXY)在歐股早盤刷新日高至 97.286,歐股盤中轉跌後保持跌勢,美股尾盤跌破 96.00 至 95.60 下方,刷新 2022 年 2 月以來低位,日內跌逾 1.5%。

- 到週二匯市尾盤,美元指數處於 95.80 下方,日內跌逾 1.3%;追蹤美元兑其他十種貨幣匯率的彭博美元現貨指數日內跌近 1.1%,盤中刷新 2022 年 3 月以來低位,均創去年 4 月特朗普公佈對等關税以來最大四日跌幅。

美元指數創去年 4 月以來最大日跌幅

非美貨幣:

- 日元三連漲,三日累漲略超 4%,美元兑日元在歐股早盤刷新日高至 154.88,歐股盤中轉跌後保持跌勢,美股尾盤跌至 152.10,日內跌超 1.3%,刷新 2025 年 10 月末以來低位。

日元創去年 10 月末以來新高

- 歐元兑美元在美股盤後曾漲破 1.2080,日內漲 1.7%,自 2021 年 6 月以來首次升至 1.20;英鎊兑美元在美股盤後曾靠近 1.3870,刷新 2021 年 9 月以來高位。

- 離岸人民幣(CNH)兑美元在亞市盤中刷新日低至 6.9567,美股盤後曾漲至 6.9313,在連續兩日盤中漲破 6.95 後,自 2023 年 5 月以來首次盤中漲破 6.94,日內漲 175 點,北京時間 1 月 28 日 4 點 59 分,離岸人民幣兑美元報 6.9337 元,較週一紐約尾盤漲 151 點,三連漲。

加密貨幣:

- 比特幣(BTC)在美股早盤曾跌破 8.75 萬美元刷新日低,後很快重上 8.8 萬美元,美股尾盤逼近 8.93 萬美元刷新日高,較日低漲超 2000 美元、漲超 2%,美股收盤時處於 8.91 萬美元上方,最近 24 小時漲近 2%。

- 以太坊(ETH)在歐股盤中跌破 2900 美元刷新日低,美股盤中拉昇,尾盤曾逼近 3020 美元刷新 1 月 22 日以來高位,較日低漲超 4%,美股收盤時處於 3010 美元上方,最近 24 小時漲超 4%。

美消費者信心遜色,美債收益率刷新日低,後長短債收益率走勢分化,收益率曲線趨陡。

美國諮商會消費者信心公佈後,美國 10 年期基準國債收益率在美股早盤曾下破 4.21% 刷新日低,後震盪上行,到債市尾盤時約為 4.24%,日內升約 3 個基點,在連降兩個交易日後反彈。

對利率前景更敏感的 2 年期美債收益率在美國消費者信心數據發佈後下破 3.57% 刷新日低,到債市尾盤時約為 3.57%,日內降約 2 個基點,在週一收平後重回上週五的下行勢頭。

長短期美債收益率表現不一,短債收益率下行,長債收益率反彈

歐洲國債價格總體回落,收益率回升。到債市尾盤,英國 10 年期基準國債收益率約為 4.52%,日內升 3 個基點;基準 10 年期德國國債收益率約為 2.87%,日內升 1 個基點。

原油反彈,尾盤一度漲超 3%。

國際原油期貨:

- 歐股早盤刷新日低時,美國 WTI 原油跌至 60.14 美元,日內跌 0.8%,布倫特原油跌至 65 美元,日內跌 0.9%,歐股盤中轉漲後美股午盤加速上行。

- 到美股午盤時段原油收盤時,週一回落的美油和布油刷新將近四個月來收盤高位。WTI 3 月原油期貨收漲 1.76 美元,漲幅超過 2.90%,報 62.39 美元/桶;布倫特 3 月原油期貨收漲 1.98 美元,漲幅將近 3.02%,報 67.57 美元/桶。

- 美股尾盤,原油的盤中漲幅擴大到 3% 以上,美油刷新日高至 62.63 美元,較週一收盤漲約 3.3%,布油漲至 67.78 美元,較週一收盤漲逾 3.3%。

美國 WTI 原油自 1 月中以來首次重上 62 美元

美國汽油和天然氣期貨:

- 週一回落的 NYMEX 2 月汽油期貨收漲近 2.5%,報 1.8652 美元/加侖;週一大漲近 29% 的 NYMEX 2 月天然氣期貨收漲超 2.26%,報 6.9540 美元/百萬英熱單位,六連漲。

黃金連續六日收創歷史新高,現貨黃金一度漲超 3%;盤中期銀曾跌超 10%、現貨白銀一度漲超 9%。倫銅回落超 1%。

黃金:

- 紐約黃金期貨在亞市早盤刷新日低至 5004.5 美元,日內跌逾 1.5%,美股早盤轉漲。到美股午盤期金收盤時,COMEX 2 月黃金期貨收漲 0.1 美元,報 5082.6 美元/盎司,六連漲且連續六個交易日刷新收盤最高紀錄。

- 黃金美股午盤拉昇,美股尾盤連續第七個交易日創盤中歷史新高時,紐約期金漲至 5188.8 美元,日內漲近 2.1%,全天處於漲勢的現貨黃金漲至 5187.37 美元,日內漲近 3.6%。

現貨黃金亞市早盤轉漲,美股尾盤拉漲、漲幅擴大到 3% 以上

白銀:

- 連續三個交易日收創新高的紐約期銀回落,COMEX 3 月白銀期貨收跌 8.27%,報 105.957 美元/盎司,週二亞市盤初刷新日低至 102.9 美元,日內跌 10.9%,歐市早盤刷新日高至 113.55 美元時,日內跌幅收窄到 1.7%,美股早盤跌幅曾擴大到 9% 以上,尾盤跌幅收窄到 4% 以內。

- 現貨白銀在亞市盤初轉漲後保持漲勢,歐股早盤漲至 113.4586 美元,日內漲逾 9.3%,還未逼近週一漲至 117 美元上方刷新的盤中最高紀錄,美股早盤時曾跌至 106 美元下方,日內漲幅曾收窄到不足 1.5%,午盤漲幅擴大,美股尾盤時重上 112.00 美元、日內漲超 8%。

現貨白銀週一盤中漲超 10% 後一度抹平漲幅,週二歐股盤中曾漲超 9%,美股早盤時漲幅曾收窄到不足 2%,尾盤時漲幅超過 8%

倫敦基本金屬期貨:

- 兩連漲刷新兩週來高位的倫銅回落超 1%。倫鎳跌近 2%,繼續跌離上週五刷新的一年半來高位。倫錫反彈超 1%,還未逼近上週五五連漲所創的收盤最高紀錄。

- LME 期銅收跌近 1.5%,報 13006 美元/噸。LME 期鎳收跌 1.9%,報 18169 美元/噸。LME 期錫收漲約 1.2%,報 54878 美元/噸,上週五報 56816 美元創歷史新高。