Citi's latest commodity outlook: In a bull market scenario, gold prices at $6,000, copper at $15,000, and aluminum aiming for the $4,000 mark

Citigroup believes that gold has shifted from "cost pricing" to being determined by wealth reallocation and supply rigidity, potentially reaching $6,000 in a bull market scenario; copper and aluminum have become core carriers for AI and energy transition: copper, under the constraints of data centers, inventory, and supply, points to $15,000/ton in a bull market scenario; aluminum, due to China's production capacity limits, power constraints, and structural demand growth, is seen as the most certain bullish asset in the medium term, with an optimistic target approaching $4,000/ton

In the latest annual commodity outlook report released by Citigroup's commodity research team, the focus is on two contradictions: on one hand, precious metal prices are "decoupling" from mining costs, with profit margins soaring to levels not seen in decades; on the other hand, while basic metals still have short-term tailwinds, the real mid-term stories are concentrated on copper, aluminum, and the narratives surrounding electricity and AI behind them.

According to news from the trading desk, Citigroup analysts Max Layton and others have a core judgment on gold: the pricing anchor is undergoing a structural shift: gold prices are no longer dominated by marginal mining costs, but are determined by the scale of global nominal spending on gold and the highly inelastic supply capacity. Given the limited elasticity of mineral supply, recycling, and stockpiling, the price itself becomes the only clearing mechanism. The physical gold market is too small, meaning that even a very small proportion of wealth reallocation can only be balanced through a significant price increase, thus gold is transforming from a "safe-haven tool" into a macro asset reflecting changes in global wealth structure.

In the "bull market scenario" set by Citigroup, the price centers for gold, copper, and aluminum will be significantly elevated: gold could reach $6,000 per ounce, copper could rise to $15,000 per ton, and aluminum could approach $4,000 per ton.

The rise of gold to "decoupling from costs" instead turns hedging into a high-risk action

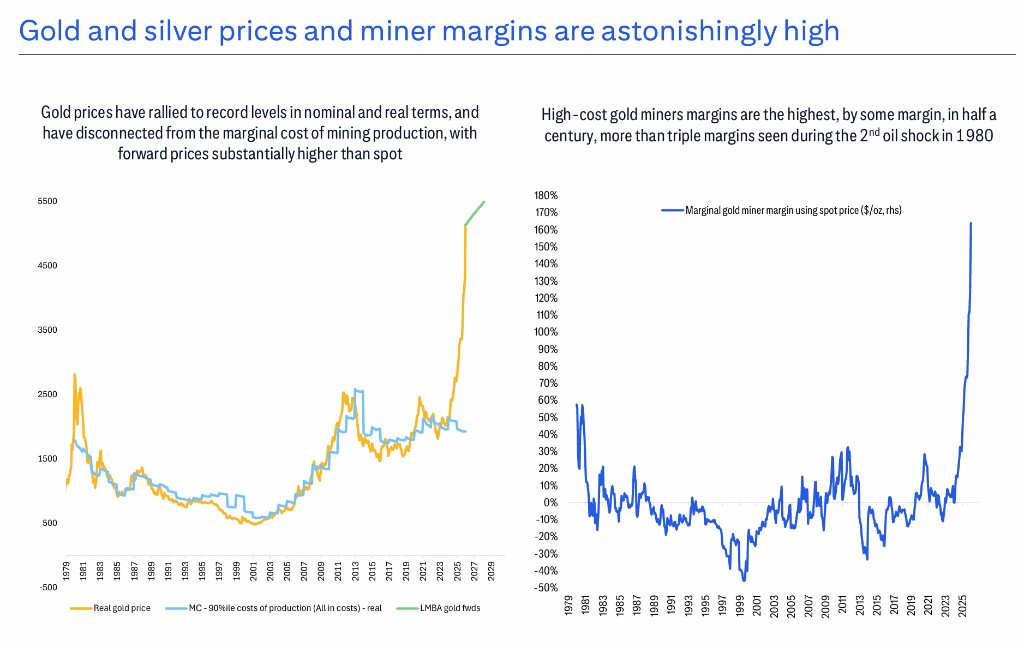

The report first presents an intuitive fact: gold prices have reached new highs both nominally and in real terms, and there is a clear divergence from marginal mining costs, with forward prices significantly higher than spot prices. The result is that the profit margins of high-cost gold mines have surged to "the highest in half a century," even more than three times higher than the profit margins of mining companies during the "second oil crisis" in 1980.

In this profit state, many companies instinctively react by "locking in profits." Citigroup's reminder is sharp: historically, the issues with corporate and sovereign hedging have mostly not been due to the "hedging" itself, but because they sold off the upside, especially "over-sold the upside." This can expose companies/sovereigns to risks during cost inflation and when production falls short of expectations; it can also trigger conflicts in shareholder demands for upside exposure, and even lead to cash margin call pressures.

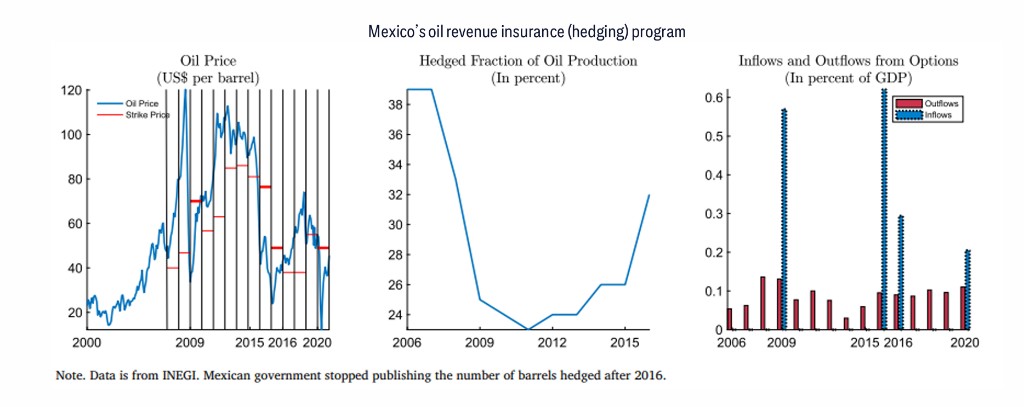

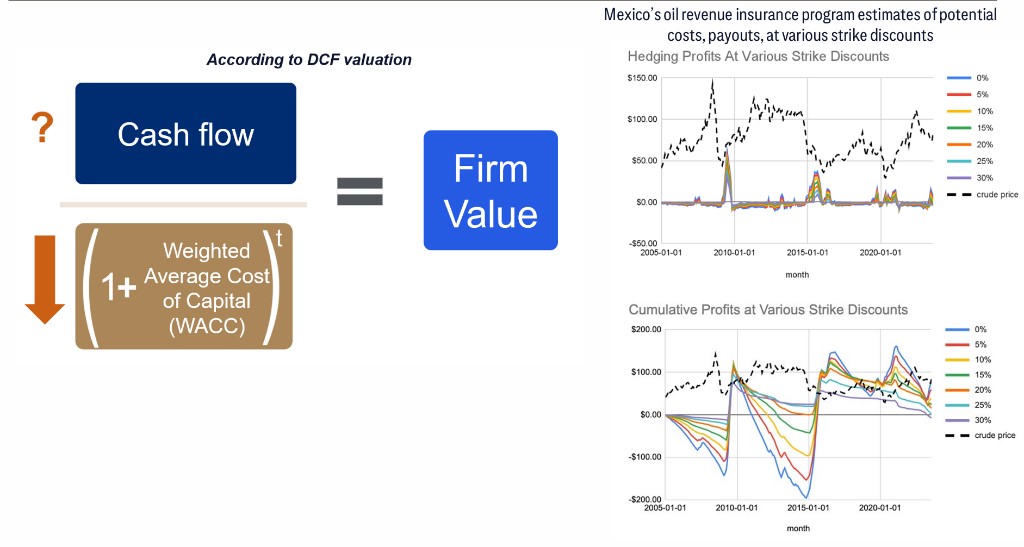

The report spends considerable space discussing Mexico's oil revenue insurance-style hedging: reducing income volatility through rolling insurance payments rather than selling off price upside potential. The cited academic research conclusion is that Mexico has not encountered significant hedging issues in the past 20 years while achieving lower income volatility; the IMF and academic studies also mention that this has led to lower sovereign debt costs and welfare gains.

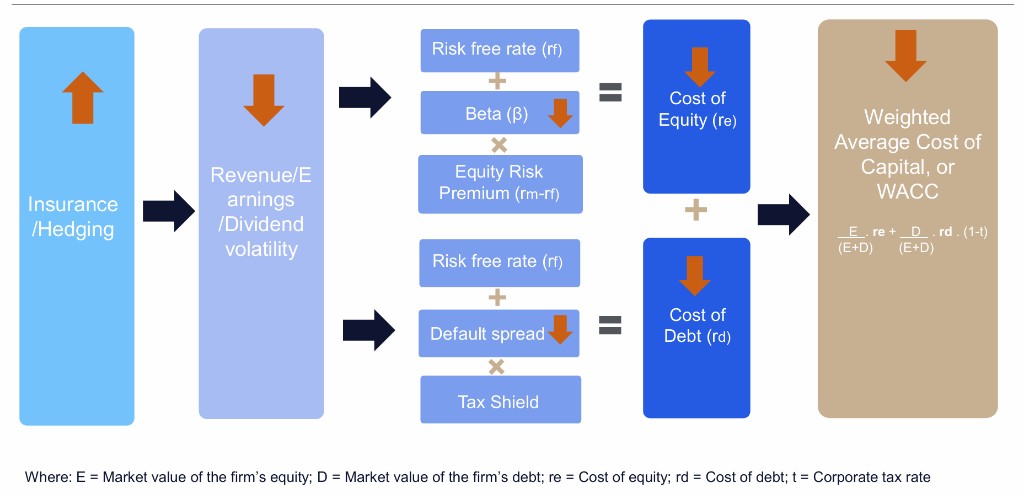

Citigroup translates this logic to the corporate side: if insurance/hedging is used to cut off the transmission of "commodity volatility - profit volatility," it can theoretically reduce the probability of default and the probability of equity loss, thereby lowering the cost of capital (beta, WACC) and increasing valuation. The cost is also laid out: insurance is not free. The report mentions that part of the insurance premium can be offset by selling a limited call spread—the key is "limited," to avoid unlimited upside selling.

Citigroup translates this logic to the corporate side: if insurance/hedging is used to cut off the transmission of "commodity volatility - profit volatility," it can theoretically reduce the probability of default and the probability of equity loss, thereby lowering the cost of capital (beta, WACC) and increasing valuation. The cost is also laid out: insurance is not free. The report mentions that part of the insurance premium can be offset by selling a limited call spread—the key is "limited," to avoid unlimited upside selling.

Citigroup does not present insurance as a holy grail. The report clearly states that the impact of hedging/insurance on cash flow may be uncertain in both the short and long term. The Mexican project reduces volatility in the long term while "ultimately having no cost"; however, the same does not hold for gold—because over the past 25 years, gold has risen from about $300/ounce to about $4000/ounce, and long-term upward trends can make "locking in" expensive. Even the Mexican model itself sees cash flow switch between positive and negative phases: in years when oil prices are high and then fall (such as 2009/2015/2020), cash flow is positive, while in intermediate phases it may be negative.

Under the new gold pricing mechanism, can household wealth transfer push gold prices to $6000?

Citigroup emphasizes that gold rising to "beyond cost" does not mean that gold prices are "distorted." On the contrary, the pricing mechanism of gold is changing.

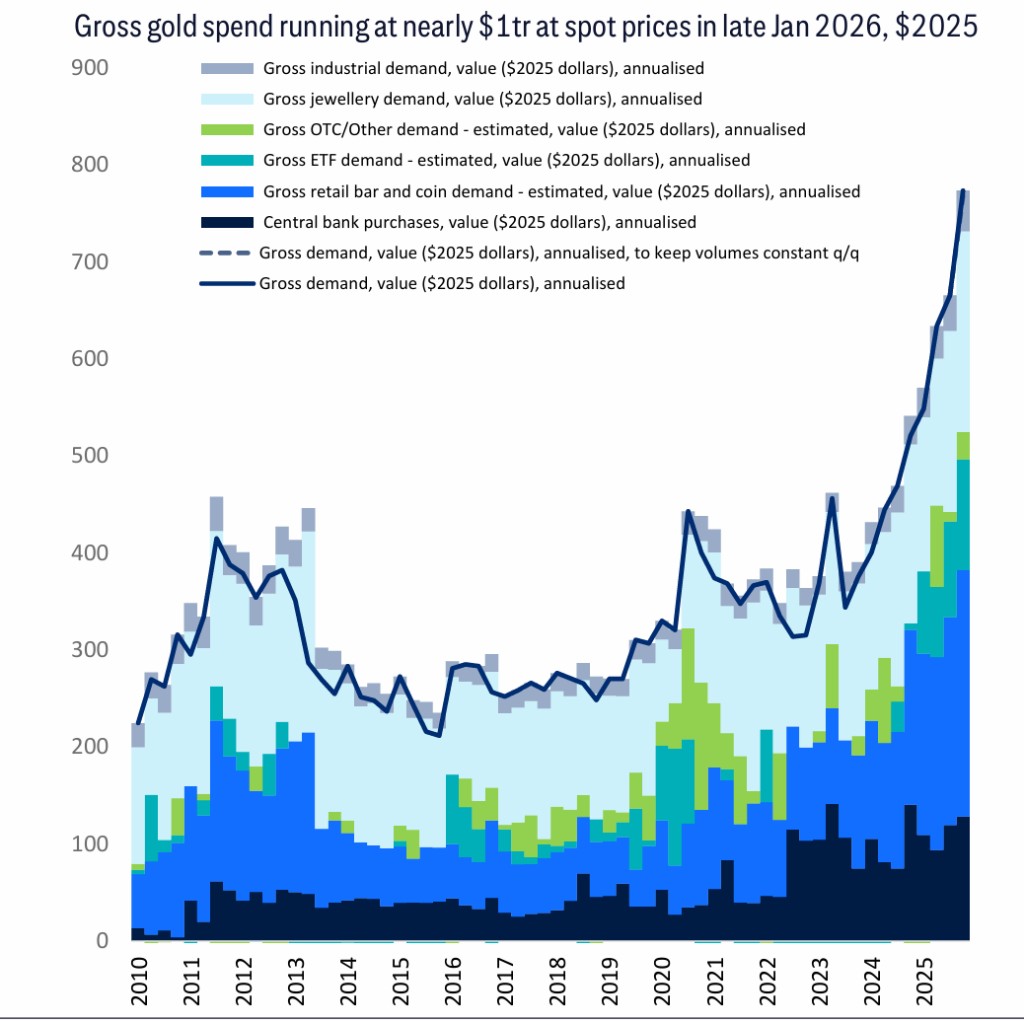

The report breaks down gold prices simply: Gold price ≈ Total dollar expenditure on buying gold ÷ Gold supply (mining supply + stock sales). In late January, annualized calculations based on spot prices, and adjusted to 2025 constant prices, show that global "total expenditure on buying gold" is close to $1 trillion.

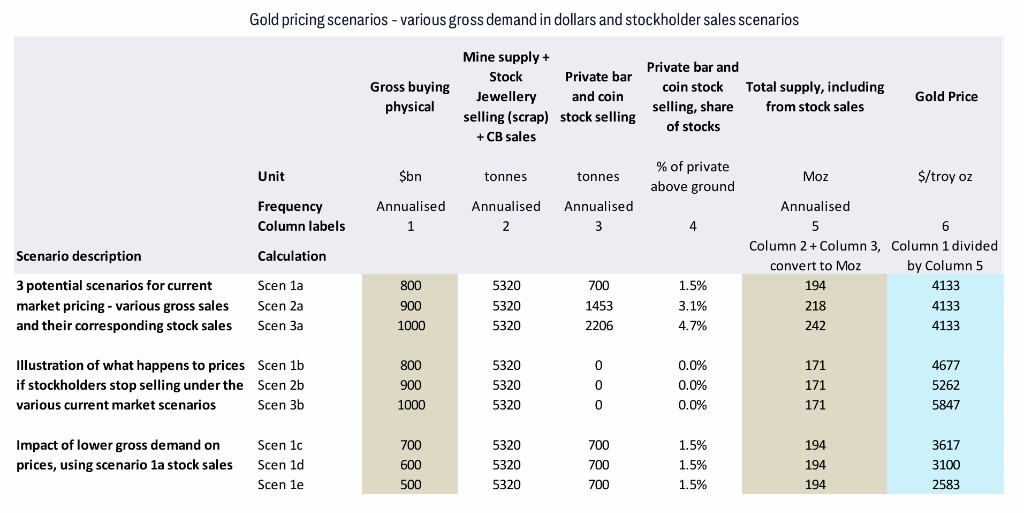

Citigroup also uses scenario tables to explain that "the same price can be explained by different combinations": under different combinations of total expenditure on buying gold and different stock sale ratios, the same gold price level can be derived; once stockholders stop selling, under the assumption of the same buying expenditure, the derived gold price will jump significantly (the levels provided by Citigroup range from about $4677/ounce to about $5847/ounce).

The risk checklist supporting "buying on dips" is quite diverse yet specific: concerns about currency "devaluation/vulnerability" triggered by sovereign debt and high interest costs (especially in the U.S.), geopolitical risks (involving Russia, Iran, Venezuela, NATO, and Russia-Ukraine), worries about the long-term impact of AI, insufficient investment channels in China coupled with high savings, and the emergence of new gold buying vehicles opening up incremental markets (Costco, stablecoins, crypto-related products).

The risk checklist supporting "buying on dips" is quite diverse yet specific: concerns about currency "devaluation/vulnerability" triggered by sovereign debt and high interest costs (especially in the U.S.), geopolitical risks (involving Russia, Iran, Venezuela, NATO, and Russia-Ukraine), worries about the long-term impact of AI, insufficient investment channels in China coupled with high savings, and the emergence of new gold buying vehicles opening up incremental markets (Costco, stablecoins, crypto-related products).

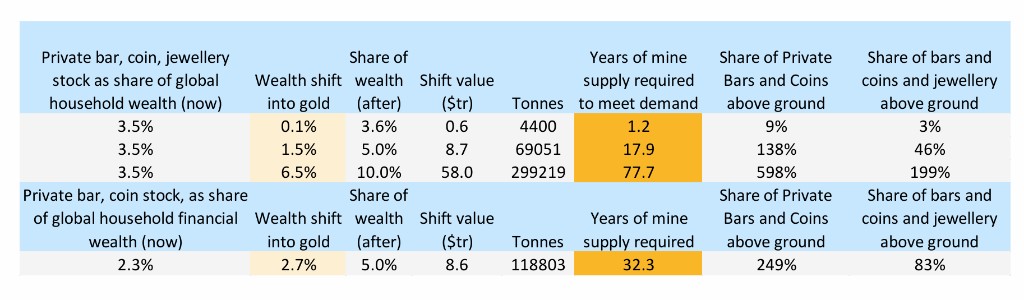

The most aggressive and impactful page of the report uses supply elasticity to refute the notion of "wealth smoothing migration": the current value of gold supply is only about 0.1% of global household wealth. This means that if household wealth shifts 0.1% (one-thousandth) towards gold, theoretically, "mineral supply would need to double" to meet the demand.

Further extrapolation: if global households increase their allocation to gold from a long-term average of 3.5% to 5% (an increase of 1.5 percentage points), the demand would equate to 18 years of mineral supply, nearly half the "accumulated stock of jewelry and gold bars and coins throughout human history." Citigroup directly states: this wealth migration cannot be resolved by production, but only by price—under this 1.5 percentage point migration scenario, the gold price would need to rise to about $6,000 per ounce, which is roughly consistent with its 'bull market scenario.'

However, the report also adds a boundary condition that is easily overlooked: at current prices, the private sector's stock of gold bars, coins, and jewelry is about $20 trillion, which is equivalent to approximately 6% of global household financial wealth.

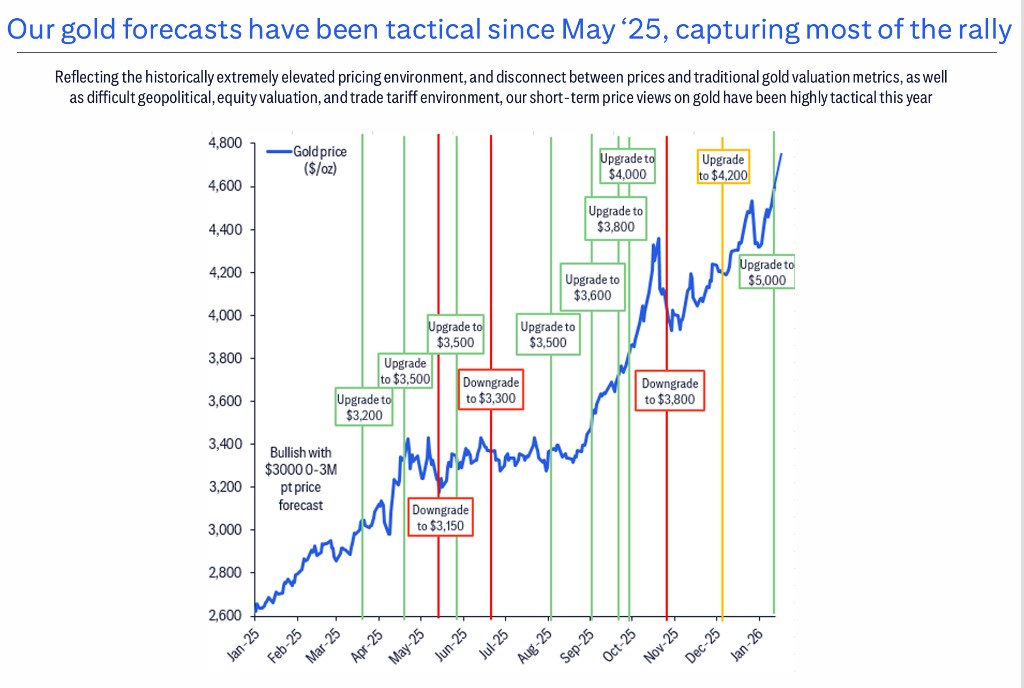

It is noteworthy that Citigroup's attitude towards gold in the report is not unidirectionally bullish. On the contrary, the research team repeatedly emphasizes that current gold prices are at "historical extreme ranges," and future trends will increasingly depend on marginal changes in capital flows and risk variables.

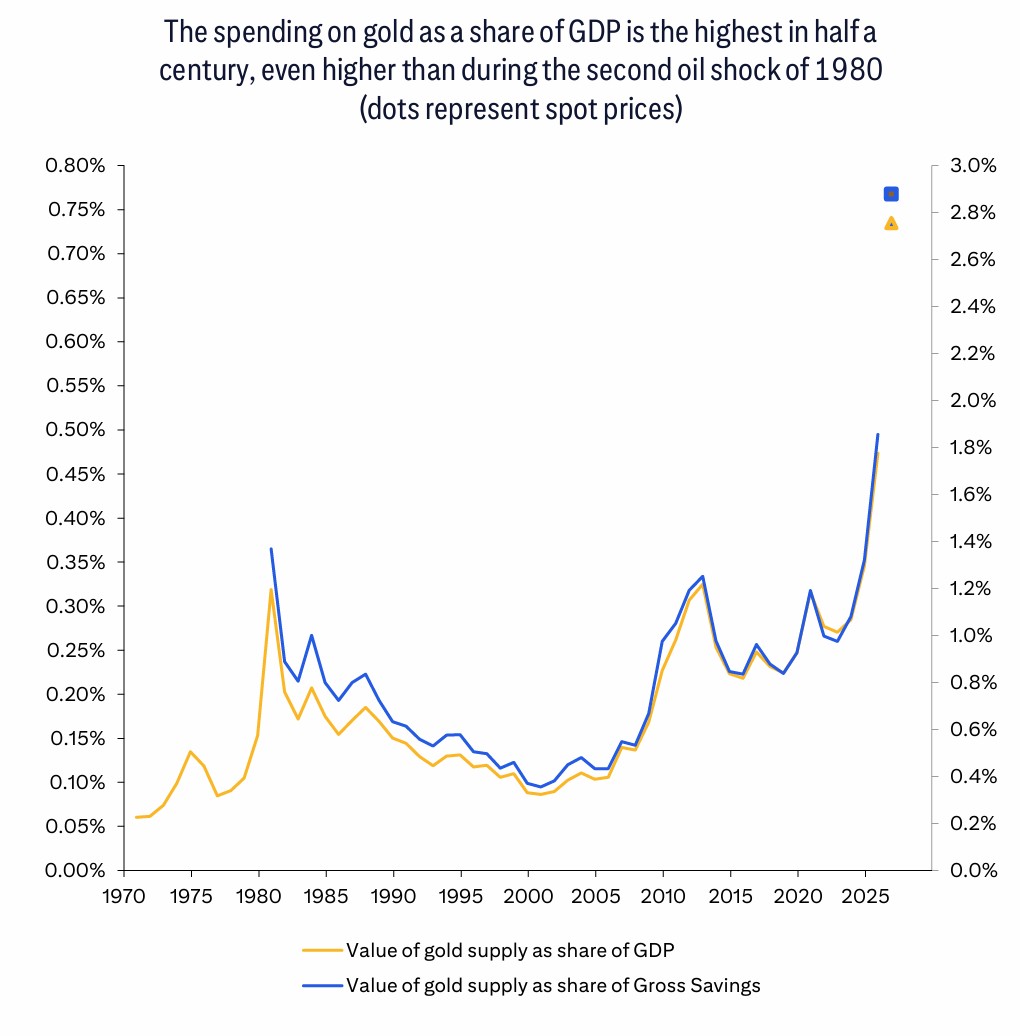

Citigroup provides a more "sustainability stress test" perspective: at around $5,100 per ounce, global gold expenditure accounts for about 0.73% of GDP and approximately 2.9% of total global savings, one of the highest levels in 55 years of data. Looking solely at household jewelry and investment demand, net expenditure accounts for about 5–6% of household savings (the report assumes household savings of about $9–10 trillion); gross expenditure estimates even reach 10–11%. Citigroup's conclusion is straightforward: this is very high and unlikely to be sustainable in the long term.

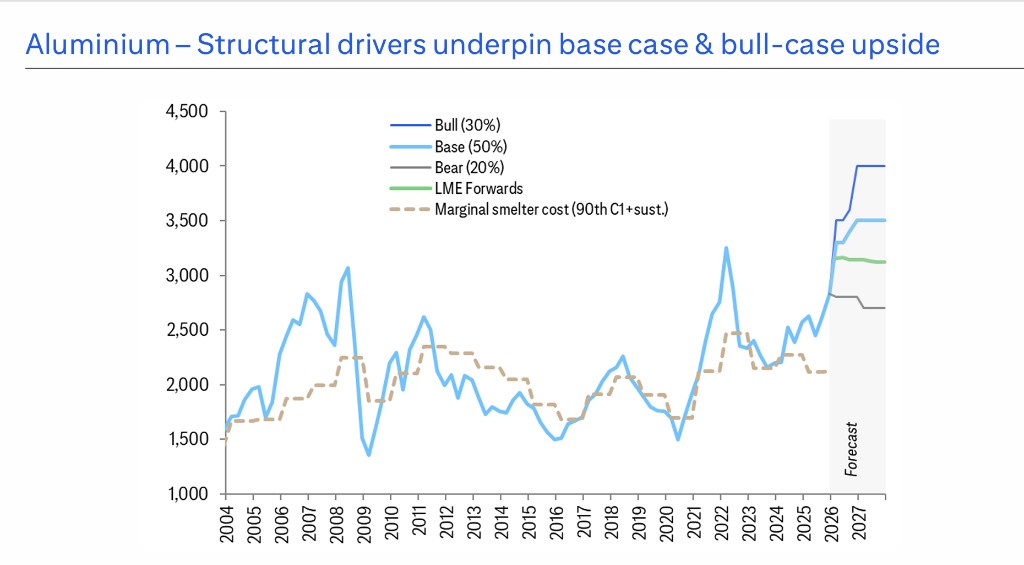

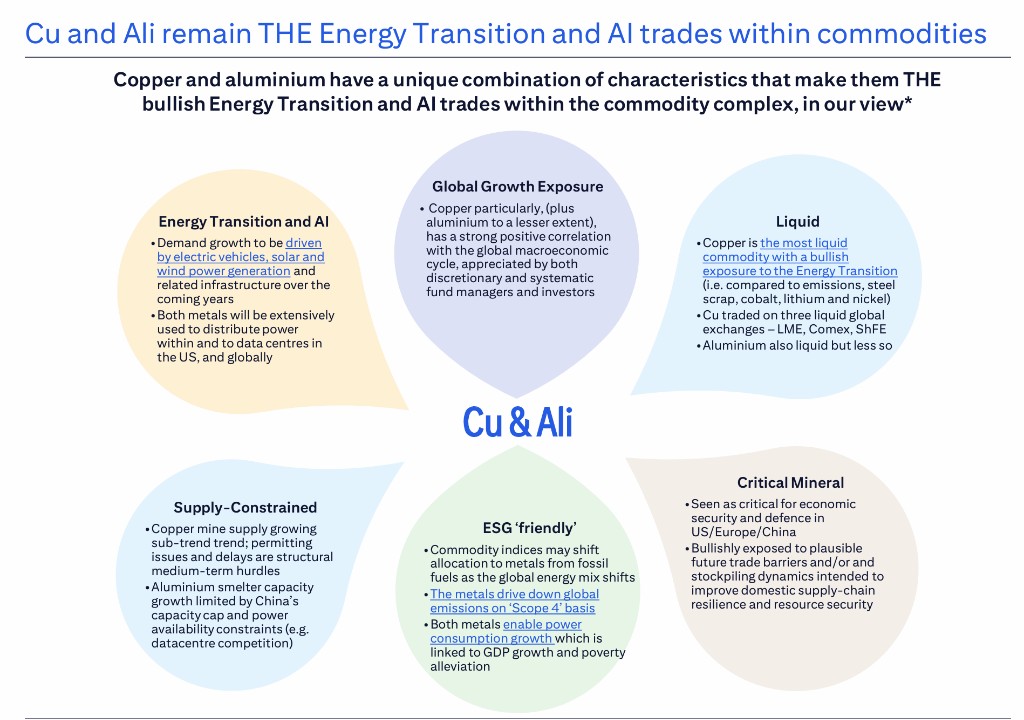

Base Metals: Mid-term Bets Leaning More Towards Aluminum, Targeting $4,000

In the realm of base metals, it is noteworthy that robots may be an underestimated variable in metal demand. Citigroup points out that both humanoid and non-humanoid robots are essentially "metal-intensive terminals" that heavily rely on electricity, lithium, copper, and aluminum.

Citi cites calculations indicating that if the robotics industry accelerates its expansion over the next decade, its demand for electricity and metals could reach several times the current global supply. The report also notes that China's output in the service robot sector has shown significant acceleration, a trend that may have a nonlinear impact on metal demand in the medium to long term.

From a strategic perspective, Citi acknowledges that the recent upward momentum in metals (and many hard assets) may still have inertia in the short term, but compared to early December, the team's confidence in whether "spot logic can still support in the longer term" has decreased.

Aluminum is viewed by Citi as a structurally stronger bullish variety. Due to the cap on China's electrolytic aluminum production capacity, power constraints, and competition for electricity from data centers and power infrastructure, Citi believes that the supply elasticity of aluminum is long-term limited, while the demand side continues to benefit from the restructuring of the energy system.

In terms of target prices, Citi sets a 2026 average price benchmark of $3,650/ton, a bull market price of $4,000/ton, and a bear market price of $2,800/ton. The core logic is that in the medium term, there is a structural bullish outlook, with supply constrained by China's production capacity limits and power restrictions (competition for electricity from data centers), while demand benefits from energy transition and growth in the robotics industry; the baseline scenario sees supply and demand roughly balanced, with weak demand in a bear market leading to price declines.

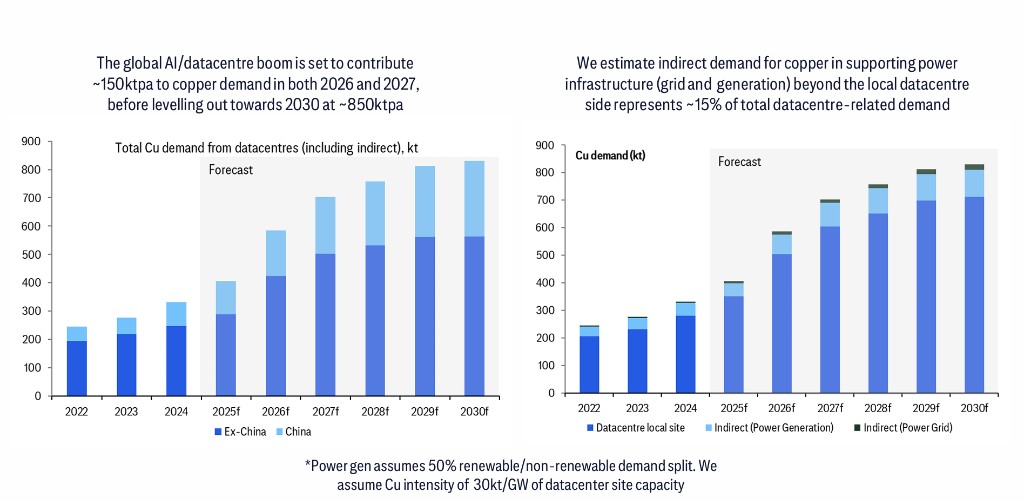

Copper: AI Data Centers' Increment Over Two Years, Bull Market Scenario Expected to Reach $15,000

Citi has a clear framework for copper:

- If the construction of AI data centers continues to accelerate, it could bring about an additional 150,000 tons/year of copper demand in 2026/2027; however, data centers currently account for only 1.5% of global copper consumption, and it is expected to only reach 2.4% by 2027, so this clue will diminish marginally after 2027.

- In terms of price, Citi sets the baseline scenario for copper prices in 2026 at an average of about $13,000/ton for the year, believing that this price level can achieve a "fragile but maintainable balance" between constrained supply, increased recycling, and expanding demand. In a more optimistic scenario, influenced by factors such as a soft landing in the U.S., a weaker dollar, increased resource security stockpiling, shortages in mine/scrap supply, and the implementation of U.S. copper import tariffs, there is potential for copper prices to reach $15,000/ton.

- In terms of supply and demand, Citi describes the 2026 market as "close to balance but slightly lacking": refined copper deficit of 56,000 tons.

The real variable, Citigroup names as scrap copper: its "Call on Scrap" framework believes that at $1,000/ton, scrap copper supply will increase by about 150,000 to 200,000 tons/year. However, Citigroup also left a note of uncertainty: the high prices in April/May 2024 triggered a significant destocking response in scrap copper, and it is uncertain whether this round of price increases can replicate a similar scale of "release"—this is also a path to a bullish scenario.

The real variable, Citigroup names as scrap copper: its "Call on Scrap" framework believes that at $1,000/ton, scrap copper supply will increase by about 150,000 to 200,000 tons/year. However, Citigroup also left a note of uncertainty: the high prices in April/May 2024 triggered a significant destocking response in scrap copper, and it is uncertain whether this round of price increases can replicate a similar scale of "release"—this is also a path to a bullish scenario.

The report also highlights "U.S. tariffs and inventory" separately: the team expects U.S. net imports to be below normal in the coming months, gradually digesting the surplus inventory accumulated in the U.S. by 2025; there remains a "potential 15% (2027) and 30% (2028)" tariff risk in the price spread, but its baseline judgment is that either no tariffs will be imposed, or they will be implemented in phases under S232 with zero tariff exemptions for key partners.

Other Metals: Nickel is more about emotional recovery, Zinc follows the surplus logic, Tin looks at supply disruptions

- Nickel: The report attributes the recent rebound more to "short covering," meaning that market confidence in the downside is weakening, but this does not equate to a new consensus on sustainable upward movement; under the baseline scenario, the average price in 2026 is about $17,000/ton.

- Zinc: Citigroup predicts that the refined zinc market will enter an "expanding surplus" in 2026-2027, with prices possibly strengthening in the short term, but supply growth will exceed demand.

- Tin: In a bullish scenario, "scarcity pricing" may occur, with prices soaring to around $55,000/ton and then falling back to a more sustainable $45,000/ton by the end of 2026, while emphasizing that net long positions in funds have become relatively high, supply from Myanmar (Wa State) may gradually recover by 2026, and the convenience yield at multi-month lows indicates that there is currently no sign of inventory tightness.