For the third consecutive week, there has been a significant inflow of funds into commodities, highly concentrated in precious metals and agricultural products

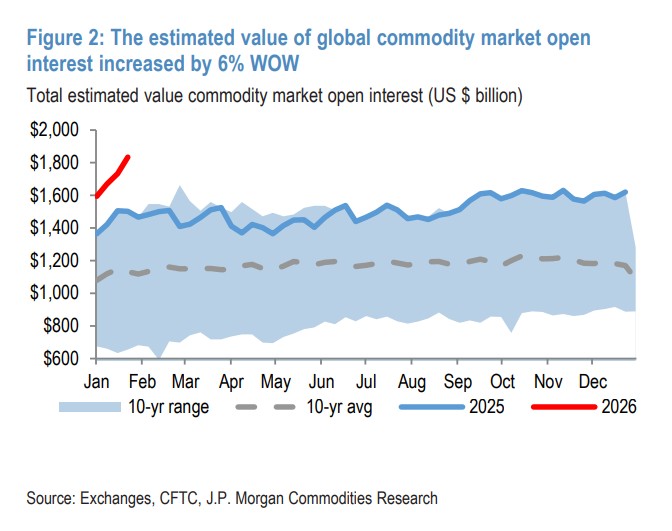

JP Morgan's latest report shows that global commodity markets have seen significant inflows of funds for the third consecutive week. As of January 23, the total value of open interest has risen to approximately $1.83 trillion, setting a new historical high. The flow of funds is highly concentrated in the precious metals and agricultural sectors, with net inflows of $21.5 billion and $8.9 billion, respectively, with gold being the primary source of incremental growth. Additionally, extreme cold weather has driven U.S. natural gas prices to surge by 70%

Global capital is continuously increasing its investment in the commodity market, and the flow is rapidly "focusing."

According to the Wind Trading Desk, JP Morgan's global commodity research report released on January 27 shows that driven by large-scale capital inflows for the third consecutive week and rising prices of precious metals and natural gas, the total value of open interest in the global commodity market has reached a historical high.

In the week ending January 23, 2026, the valuation of open interest in the global commodity market grew nearly 6% week-on-week (an increase of approximately $101 billion), reaching $1.83 trillion.

The report points out that this round of scale expansion is mainly driven by sustained net capital inflows combined with rising prices, with precious metals and agricultural products becoming the most concentrated areas for capital absorption.

Continuous net inflow of funds for the third week, with precious metals and agricultural products showing the most significant capital attraction

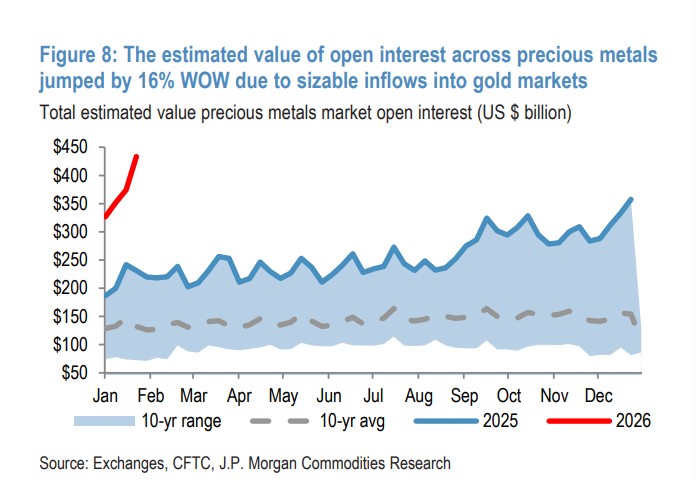

The precious metals sector is the absolute main force of capital inflow for the week.

The net inflow scale of the global commodity futures market contracts is approximately $36 billion, showing a high concentration among various assets. Among them, the precious metals sector recorded a net inflow of $21.5 billion in contracts, while gold attracted a net inflow of approximately $15.8 billion, significantly higher than silver, platinum, and palladium.

In terms of prices, the report shows that gold prices rose approximately 8% during the week, and silver prices rose approximately 14%, creating a positive resonance between prices and capital.

Therefore, as of the week ending January 23, the value of open interest in the precious metals market increased significantly by 16% (approximately $59 billion) to $433 billion, making it the single largest contributing sector for the week.

JP Morgan's commodity strategy team points out that current precious metal investors' positions are close to a phase high, but the structural logic of gold remains relatively clear, and they continue to be more optimistic about gold compared to silver.

Silver remains susceptible to sudden, destructive pullback risks. While such volatility may have some contagion effect on gold prices, it will mainly be repriced through the rebound of the gold-silver ratio, providing a buying opportunity for gold, as gold continues to have a clearer and more bullish structural logic.

Energy and Agricultural Products: Weather factors dominate natural gas, with agricultural products seeing inflows across the board

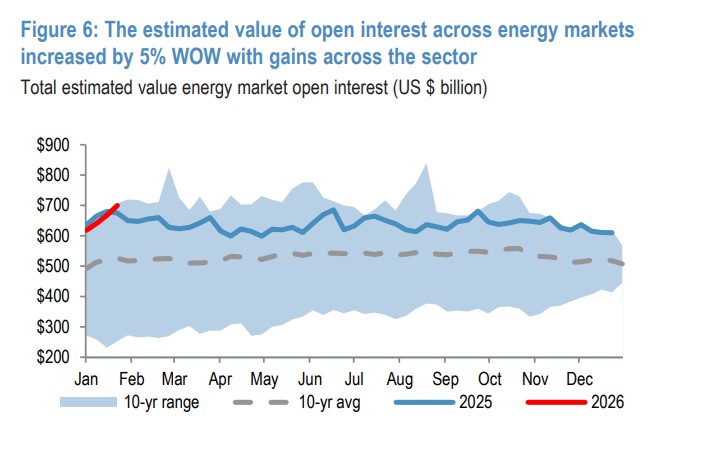

In the energy market, the value of open interest increased by 4.8% week-on-week (an increase of $32 billion) to $700 billion.

Among them, the crude oil and refined oil market saw a net inflow of approximately $8 billion, and in the context of a temporary easing of geopolitical risks, short-term supply disruptions still provide support for prices In contrast, the natural gas market is showing "price-driven expansion." The report indicates that despite a net outflow of approximately $2.5 billion in natural gas contracts that week, the Henry Hub natural gas price in the U.S. surged by about 70% in a week against the backdrop of a persistent cold wave in North America and Europe, leading to a significant increase in the value of open contracts.

The research report points out that European natural gas inventory levels are historically low for this time of year, and the rebound in heating demand is an important backdrop for the rapid price increase.

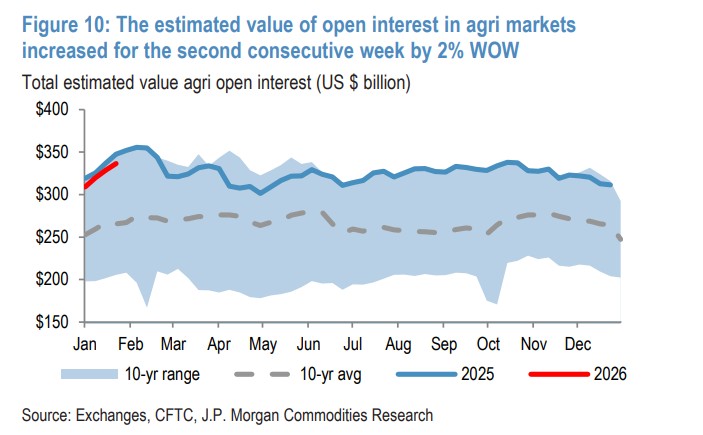

The agricultural sector also attracted funding. Data shows that the value of open contracts in the global agricultural market increased by 2.4% week-on-week to approximately $337 billion. This growth was driven by a net inflow of $8.9 billion in contracts across the sector, with price increases in grains, oilseeds, and livestock markets offsetting price declines in the soft commodities market.

Base Metals: Increased Copper Inventory Pressures Fundamentals

The value of open contracts in the base metals market increased by 2% week-on-week to $258.4 billion.

However, in terms of capital flow, the sector overall showed a net outflow (outflow of $400 million). Although copper and lead recorded an inflow of $2 billion, this was offset by an outflow of $2.4 billion from other varieties within the sector.

JP Morgan analysts expressed caution regarding the high copper prices, noting that the fundamentals are becoming more challenging. The report mentioned: "Before the Chinese Lunar New Year (February 17), inventory accumulation is above normal levels, and the COMEX/LME arbitrage at the front end of the curve has reversed."

Overall Investor Positions Stabilizing, but Structural Adjustments Are Obvious

From the perspective of investor net positions, as of January 20, the global commodity futures market's net long position was approximately $195 billion, essentially flat week-on-week.

Structurally:

-

The net long position in precious metals remains high at approximately $130.6 billion;

-

The energy sector remains net short, but the short position has narrowed to about $9.6 billion, mainly due to improvements in European natural gas holdings;

-

Net longs in base metals and agricultural products have both slightly declined.

The research report also warns that some varieties' short-term momentum indicators are approaching the "overheated" zone, indicating that buying momentum may experience a temporary slowdown.

The above exciting content comes from [Chasing Wind Trading Platform](https://mp.weixin.qq.com/s/uua05g5qk-N2J7h91pyqxQ).

For more detailed interpretations, including real-time analysis and frontline research, please join the【 [Chasing Wind Trading Platform ▪ Annual Membership](https://wallstreetcn.com/shop/item/1000309)】

[](https://wallstreetcn.com/shop/item/1000309)