Tonight's Federal Reserve decision, pausing interest rate cuts has become a consensus, but is Powell following a dovish script?

The Federal Reserve's decision to pause interest rate cuts in this meeting is no longer in doubt; the real contention lies in whether the pause is "dovish" or "hawkish." Both Morgan Stanley and Bank of America expect Powell to release dovish signals. If the wording "the scope and timing of further adjustments" is retained, it means the easing window remains open, indicating a "dovish pause"; if it changes to "when considering any adjustments to the target range," it points to a longer period of inaction, constituting a "hawkish pause."

The market has fully digested the expectation that the Federal Reserve will maintain interest rates at 3.50-3.75% in this meeting, with the focus shifting to whether this will be a "dovish pause" or an "hawkish pause."

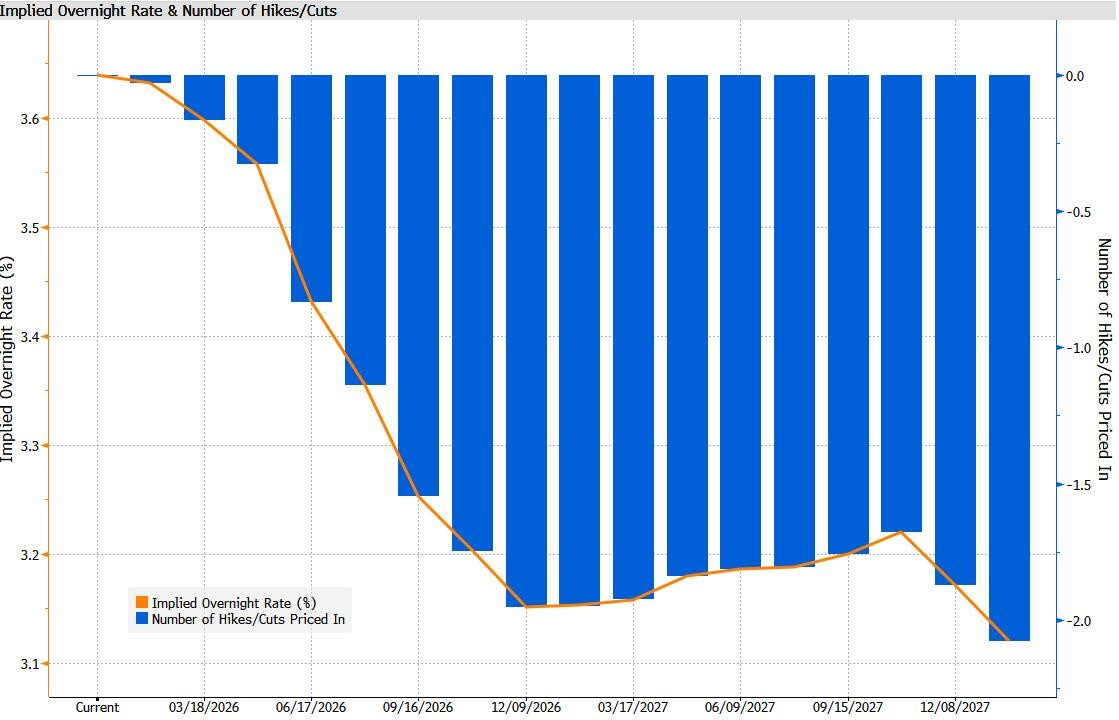

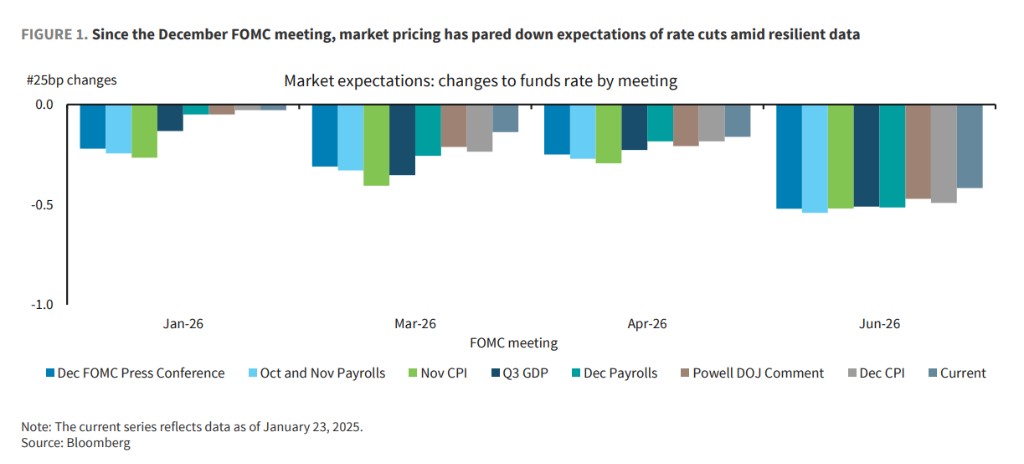

For investors, the key lies in whether Powell will retain the forward guidance for rate cuts and how to assess the distance between the current policy stance and the neutral interest rate. With the unemployment rate dropping to 4.4% and economic activity remaining robust, the market has pushed back the expectation for the first rate cut of the year to July, with an annual rate cut priced at only 45 basis points. There are still significant divisions within the committee, and Governor Miran is expected to cast another dissenting vote.

Rate cut pause is a certainty, market focuses on forward guidance

According to the latest surveys from Bloomberg and Reuters, all economists surveyed unanimously expect the Federal Reserve to keep interest rates unchanged at this meeting, with 58% of economists anticipating rates will remain unchanged throughout the first quarter. The money market is currently pricing in a rate cut of about 45 basis points by the end of the year, with the first 25 basis point cut potentially implemented as early as July.

Goldman Sachs described this meeting in its preview report as "uneventful," expecting no adjustment to the federal funds rate, with only minor adjustments to the statement and very few clues about the future policy path.

Morgan Stanley explicitly expects the Federal Reserve to convey a "dovish pause" signal—recent stabilization in the labor market and robust economic activity data are the main driving factors for pausing rate cuts, but confidence in a decline in inflation later this year will lead the Fed to retain a dovish inclination.

Minor adjustments in statement wording release key signals

Institutions generally expect several adjustments in the statement. Morgan Stanley anticipates that the committee will upgrade its assessment of economic growth from "moderate" to "solid." More importantly, it is expected that the Fed will remove the wording about "increased downside risks to employment"—since the choice to pause rate cuts logically implies that concerns about the labor market have eased.

Barclays holds a similar view, expecting the statement to mention that "job growth has slowed over the past year, and the unemployment rate has risen slightly," but will remove the wording "recent indicators are consistent with these developments." Regarding inflation, although recent core PCE data has been relatively mild, due to distortions caused by the government shutdown, the statement is still expected to maintain the wording "inflation has risen in recent months and remains elevated."

The most critical aspect of forward guidance is that the market expects to retain the wording "when considering further adjustments to the target range," which suggests that a dovish inclination remains, constituting a "dovish pause." If it reverts to "when considering any adjustments to the target range," it would imply a longer pause, constituting a "hawkish pause."

Powell's Press Conference: Three Key Focus Areas Worth Noting

Bank of America Securities points out that relative to the recent repricing of interest rates, Powell's press conference may lean dovish. Analysts will focus on three aspects:

Labor Market Assessment: The market will closely watch whether Powell emphasizes the December unemployment rate falling to 4.4% or downplays it as just a one-month data point. Equally important is whether Powell will reiterate his tolerance for a slight increase in the unemployment rate. In the December press conference, Powell stated that the policy stance after a 75 basis point rate cut should "be able to stabilize the labor market or allow the unemployment rate to rise only one or two tenths."

Inflation Trend Analysis: Market reactions will depend on whether Powell emphasizes the December core PCE year-on-year tracking data of about 3% or the ongoing housing deflation and tariff-driven inflation being below expectations. Citigroup expects the core PCE to be 2.8% in the fourth quarter of 2025, lower than the median forecast of 3.0% in the December SEP.

Neutral Rate Judgment: Investors should pay attention to Powell's comments on the neutral rate. In December, Powell stated that the policy rate "is within a reasonable estimate range of the neutral rate." Any changes in wording regarding the neutral rate or a greater emphasis on the productivity improvement story will be noteworthy.

Political Pressure May Become an "Unsustainable Issue"

"New Federal Reserve Communications" Nick Timiraos points out that while the Federal Reserve is in a wait-and-see mode, the White House is exerting unprecedented political pressure on the Fed.

This month, the U.S. Department of Justice launched a criminal investigation into Powell. Last week, the Supreme Court heard oral arguments on whether Trump has the authority to dismiss Fed Governor Cook, with several justices expressing skepticism about the president's power in this regard.

Analysts generally expect that Powell may face numerous questions on politically related topics during the press conference, but he is likely to respond with "no comment" and reiterate the Fed's position of independence from political pressure in monetary policy decisions.

Bank of America Securities clearly states, "More politically oriented questions may take center stage in the press conference, but Chairman Powell is likely to avoid providing answers."

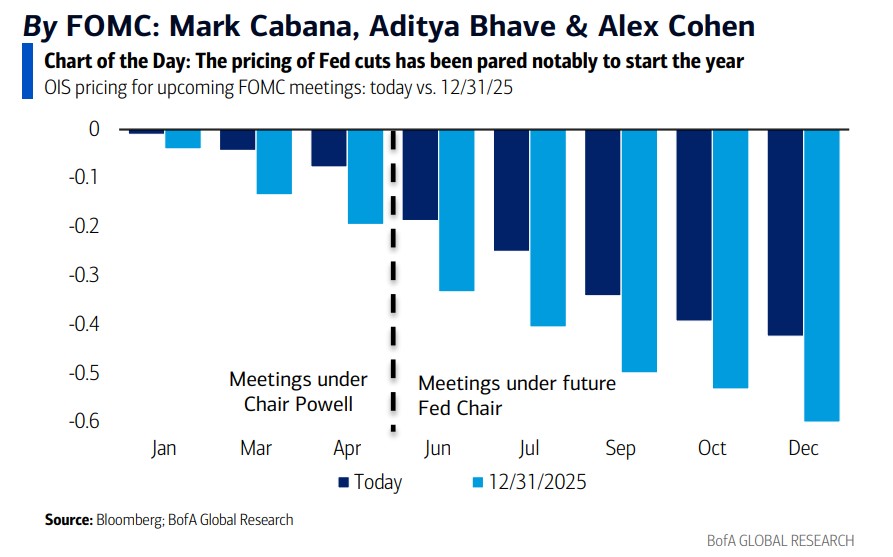

Interest Rate Cut Path This Year: Significant Discrepancies Remain

There are significant discrepancies among institutions regarding the interest rate cut path this year. Goldman Sachs expects to cut rates by 25 basis points in June and September, bringing the rate down to 3.00-3.25%. Barclays expects two cuts in June and December. Citigroup anticipates a total of 75 basis points cut in March, July, and September.

Morgan Stanley points out that of the 19 Federal Reserve officials at the December meeting, 12 expected at least one more rate cut this year, but that cut faced opposition from two officials, and some supporting the cut had reservations. This means the threshold for further rate cuts has been raised, and the Fed leadership likely hopes to form a stronger consensus than in December last year.

Timiraos analyzes that to cut rates before mid-year, it would almost certainly have to be accompanied by a deterioration in the labor market, as the pace of inflation decline may not be sufficient to persuade skeptical officials before then. Over the past 18 months, inflation has made little substantial progress.

Market Impact: Limited Volatility as the Baseline Scenario

Regarding market impact, institutions generally expect limited price fluctuations from this meeting.

Bank of America Securities stated, "The U.S. interest rate market has relatively limited expectations for the January FOMC meeting. The market has essentially fully priced in a hold at 3.5-3.75%." The institution anticipates that, aside from the standard fluctuations following the statement and press conference, this meeting may produce limited net price action.

In the foreign exchange market, Bank of America noted that during the FOMC meeting that kept rates unchanged in this cycle, the performance of the euro/dollar was mostly contained within a range of about plus or minus 0.2%, with an average essentially at 0%. "Unless there is a significant surprise—which seems unlikely—this meeting may produce limited net price action."

It is noteworthy that this meeting is expected to see at least one dissenting vote, from Federal Reserve Governor Stephen Miran, who has advocated for more aggressive easing policies at every meeting since joining the committee last September. The institution expects him to vote in favor of a 25 or 50 basis point rate cut. This will mark the fifth consecutive meeting with a dissenting vote, highlighting the significant divisions within the committee.

Additionally, Governors Bowman and Waller may also vote in favor of a rate cut, as their concerns about the labor market are greater than those of some colleagues.

Timiraos specifically pointed out that Waller's voting stance will be closely watched. He is one of the candidates being considered by Trump to replace Powell. If he votes in favor of a rate cut, it would enhance his competitive prospects; however, if he chooses to vote with the majority of officials to maintain rates, while it may strengthen his professional image as an independent voice, he could potentially lose the opportunity to become the Fed Chair