China Life Property & Casualty Insurance 2025: Net profit doubles, underwriting turns profitable

China Life Property & Casualty Insurance Company Limited (hereinafter referred to as "China Life P&C")'s 2025 report card is a sample on "balancing act." Just

China Life Property & Casualty Insurance Co., Ltd. (hereinafter referred to as "China Life P&C")'s 2025 report card is a sample of "balancing act."

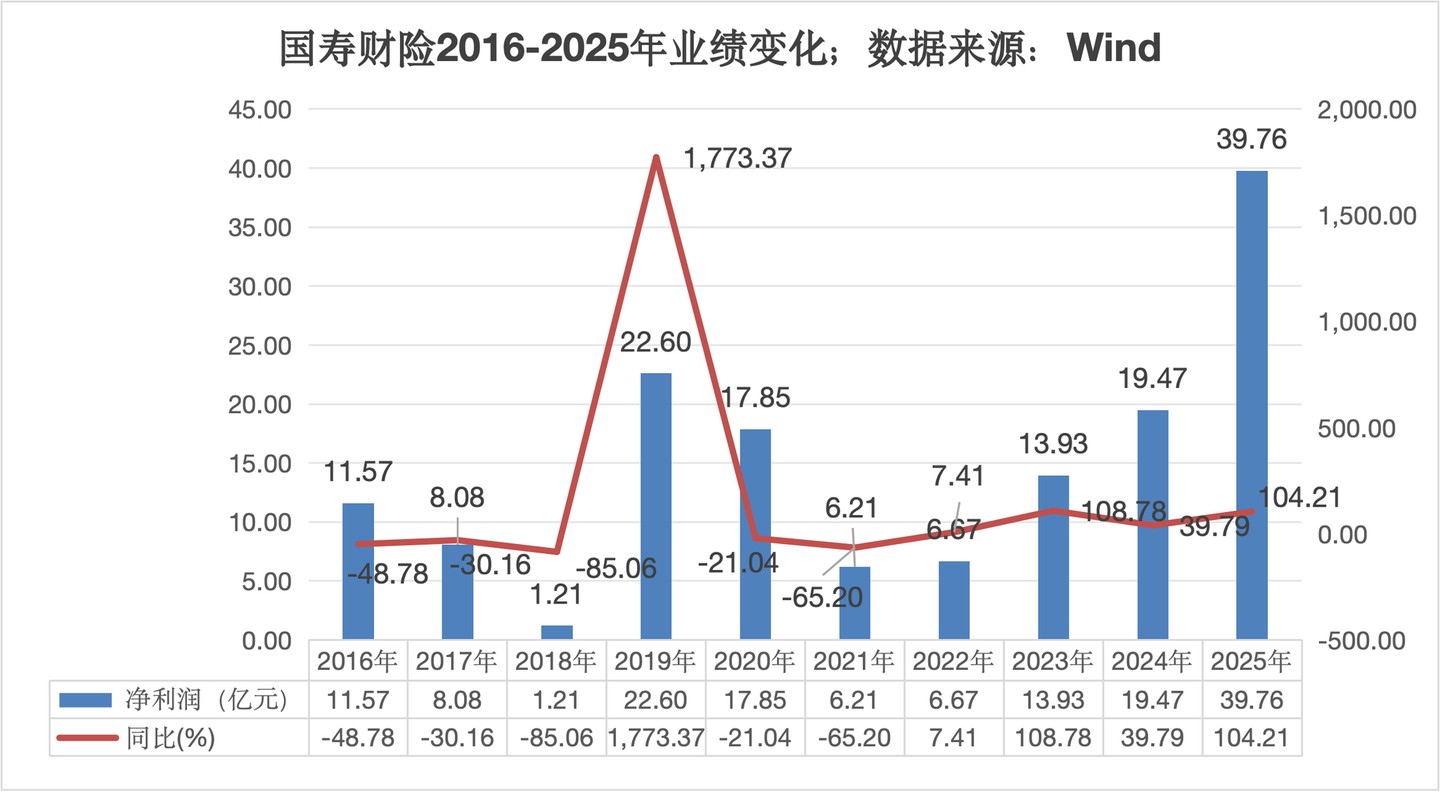

In the recently disclosed 2025 fourth quarter solvency report, China Life P&C delivered a net profit of 3.976 billion yuan for the entire year.

Compared to the net profit level of 1.948 billion yuan in 2024, this figure achieved a year-on-year doubling growth.

However, beneath the surface of the significant increase in net profit, the core logic driving performance is not the rapid expansion of premium scale, but rather a strong recovery on the investment side and the difficult turnaround to profitability on the underwriting side.

Data shows that in 2025, China Life P&C achieved insurance business revenue of 112.834 billion yuan, a slight increase of about 1.5% compared to 111.183 billion yuan in 2024.

In the context of slowing premium growth, the restoration of profitability has become particularly crucial.

Changes on the underwriting side are the focus of market attention.

In 2024, China Life P&C fell into an underwriting loss due to a comprehensive cost ratio (COR) of 100.48%. A year later, this indicator was reduced to 99.56%, returning below the breakeven line of 100%.

This means that for every 100 yuan of premium income, China Life P&C transformed from a loss of 0.48 yuan last year to a profit of 0.44 yuan, and although the profit margin remains tight, this small turnaround is quite difficult in the current context of deepening reforms in auto insurance and frequent natural disasters.

Breaking down the cost structure reveals that this improvement is largely due to cost control.

The report shows that in 2025, China Life P&C's comprehensive expense ratio was 25.41%, down more than 1 percentage point from 26.49% the previous year, while the comprehensive claims ratio rose slightly from 73.99% to 74.15%.

Under the pressure of rising claims rigidity, reducing expenses to exchange for underwriting profits has become a necessary choice for China Life P&C.

If the improvement on the underwriting side is about tightening spending, then the explosion on the investment side is the real "decisive factor" for profit doubling.

In 2025, China Life P&C's financial investment return rate reached 4.77%, significantly higher than 2.94% in 2024 and also notably better than its average level of 2.53% over the past three years.

In the absence of growth in premium scale, a nearly 5% investment return rate has become the absolute mainstay for enhancing profits.

However, it should also be noted that this profit model, which heavily relies on investment income, often faces sustainability challenges in an environment of increased volatility in the capital markets.

In terms of capital replenishment, China Life P&C has not slowed down its "blood replenishment" efforts due to the rebound in profits.

In the fourth quarter of 2025, the company successfully issued 4.5 billion yuan in capital replenishment bonds, a move that directly drove its actual capital at the end of the quarter to increase by 2.832 billion yuan compared to the previous quarter.

As of the end of 2025, China Life P&C's comprehensive solvency adequacy ratio was 218.33%, and the core solvency adequacy ratio was 184.38%, both remaining above the regulatory red line For a property insurance company with a scale of hundreds of billions, sufficient capital is not only the baseline for regulatory compliance but also a "safety cushion" to cope with future business fluctuations and potential risks.

On the personnel front, China Life Property Insurance will welcome a new leader in 2025.

Reports indicate that Li Zhuyong has been appointed as chairman since April 2025, having previously served as vice president of PICC Group. Meanwhile, the collaboration between president Huang Xiumei and the new executive team will determine the strategic direction of this insurance giant in the future.

It is worth noting that compliance pressure remains ever-present.

In just the fourth quarter of 2025, China Life Property Insurance's branches received 26 administrative penalty notices, with a total fine amounting to 5.3095 million yuan. The reasons for the penalties continue to focus on industry chronic issues such as "untrue financial business data" and "false underwriting and claims."

How to maintain performance growth while further strengthening internal control compliance remains a challenge that management must face.

Overall, 2025 for China Life Property Insurance is a battle about "returning"—returning underwriting to profitability and returning investment to value. However, under the dual pressure of thin underwriting profits and investment fluctuations, finding a more robust internal growth driver may be a more worthy consideration than simply doubling net profits