Crushing expectations! Apple's revenue and iPhone sales hit record highs last quarter, with revenue in China surging nearly 40% | Earnings report insights

Apple's Q4 revenue growth rate doubled to 16% year-on-year, EPS increased by 18%, R&D expenditure exceeded expectations with a 32% increase, and iPhone revenue grew by 23%; service revenue increased by 14%, slightly below expectations, continuing to set a quarterly record high for three consecutive years; revenue from Mac and wearable devices decreased by 6.7% and over 2%, respectively; revenue from Greater China was 17% higher than analysts' expectations; Q1 revenue is expected to grow by 13%-16%. Cook stated that due to "unprecedented strong" demand, iPhone sales "set historical highs in all regional markets" during the quarter; Apple's active device installation exceeded 2.5 billion. After hours, Apple reversed its decline and rose, at one point increasing by over 2%

The financial report shows that sales of the iPhone 17 series exceeded Wall Street's expectations, helping Apple achieve a record high in revenue.

On Thursday, Eastern Time, November 29, Apple delivered a historic performance report: for the first fiscal quarter ending December 27 ("fourth quarter"), revenue grew 16% year-on-year, with iPhone sales revenue increasing 23% year-on-year, both nearly 4% and 9% higher than analysts' expectations, respectively, exceeding the company's growth guidance of 10%-12%; EPS earnings also set a record, exceeding analysts' expectations by more than 6%, and service revenue has consistently reached a new quarterly high for three years.

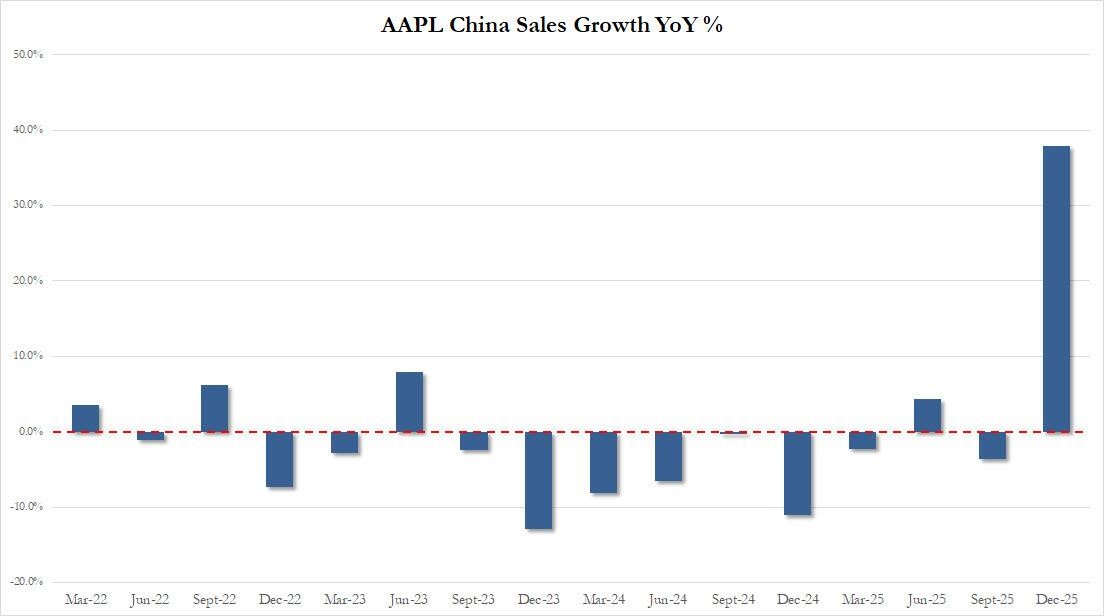

In the world's largest smartphone market, China, Apple saw a significant sales rebound. Revenue from the Greater China region turned from a year-on-year decline in the third quarter to a nearly 40% surge, nearly 20% higher than analysts' revenue expectations.

Apple CEO Tim Cook stated,

"In the fourth quarter, the company achieved an 'extraordinary record-breaking quarterly performance,' with revenue far exceeding the company's own expectations. Driven by unprecedented strong demand, the iPhone achieved its best quarterly performance ever, setting historical highs in all regional markets; the service business also achieved record revenue, growing 14% year-on-year."

Cook also mentioned that the number of active devices installed has exceeded 2.5 billion, "fully demonstrating the high satisfaction of customers with the world-class products and services we provide."

During the earnings call, Apple revealed that it expects revenue for the second fiscal quarter, which is the first quarter of this year, to grow by 13%-16%. This indicates that Apple is optimistic about performance growth following the year-end shopping season, with the best-case scenario showing year-on-year growth remaining flat compared to the fourth quarter.

After the financial report was released, Apple's stock price, which had initially dropped nearly 3% in after-hours trading, rose over 2% before giving back more than half of its gains. Commentators noted that there were no significant announcements or highlights during the earnings call.

Analysts believe that the overall data from Apple's financial report is positive, but the market hopes to see a clearer path and monetization timeline for the company in AI, especially in large models, edge inference, and the reimagining of Siri. Additionally, fluctuations in the costs of key components like memory and geopolitical risks in the supply chain remain potential variables affecting Apple's mid-term gross margin.

Fourth quarter revenue growth rate doubled year-on-year, EPS showed double-digit growth both year-on-year and quarter-on-quarter, R&D expenditure exceeded expectations by 32%

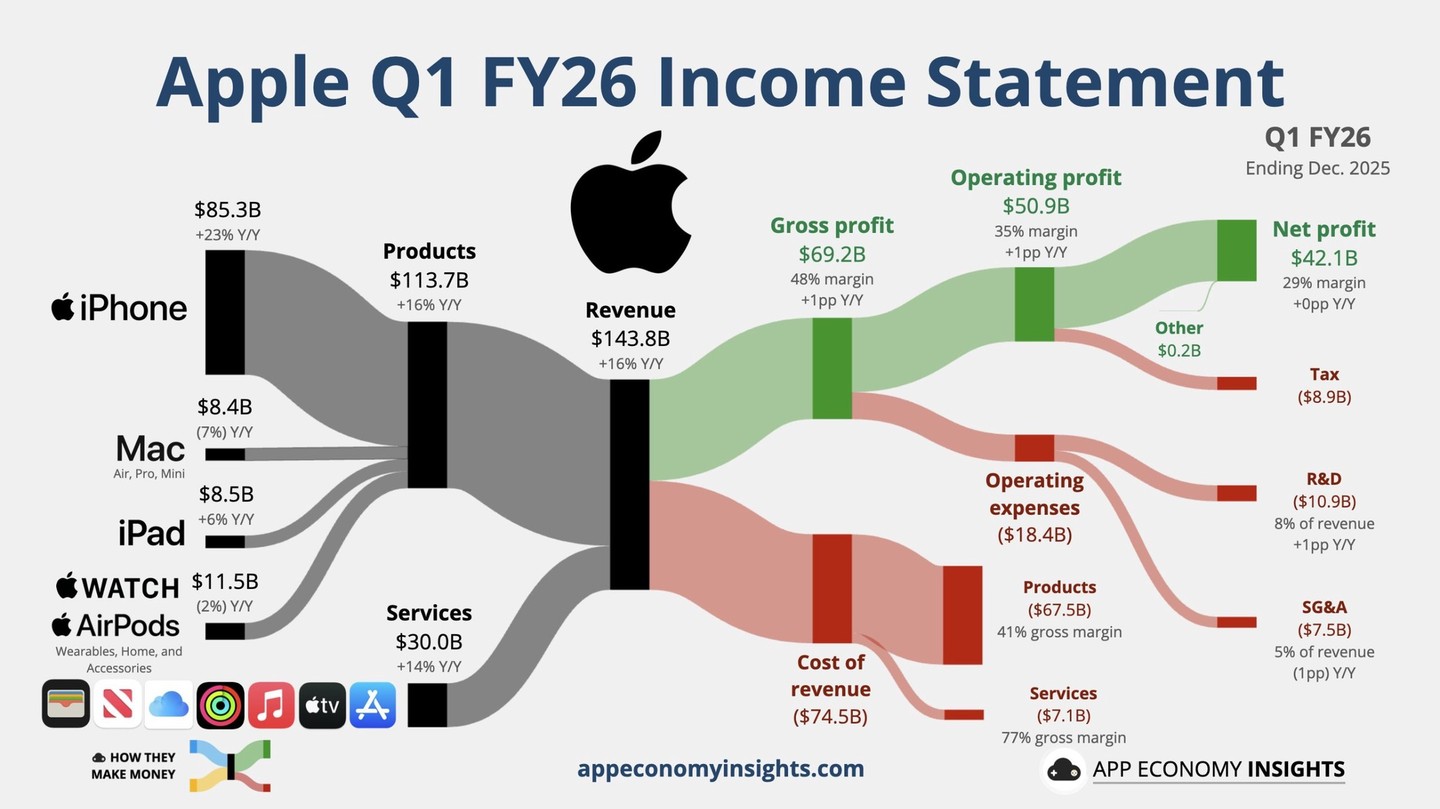

Apple announced that total revenue for the fourth quarter was $143.76 billion, with the year-on-year growth rate nearly doubling from about 8% in the third quarter to nearly 16%, while analysts expected $138.4 billion. The diluted earnings per share (EPS) for the fourth quarter was $2.84, with the year-on-year growth rate slowing from nearly 91% in the third quarter to 18%, but showing a quarter-on-quarter growth of 53.5%, with analysts expecting $2.68

The double-digit increase in EPS indicates that Apple has achieved higher profitability not only due to revenue growth but also because of its product mix and high-margin services.

In the fourth quarter, gross profit was $69.23 billion, a year-on-year increase of 19%, exceeding analysts' expectations of $65.5 billion. Operating profit was $50.852 billion, nearly a 19% year-on-year increase, demonstrating strong operating leverage.

In terms of expenses, R&D spending in the fourth quarter grew by 32% year-on-year to $10.887 billion, surpassing analysts' expectations of $10.14 billion, while sales and administrative expenses also increased. Total operating expenses for the quarter were $18.38 billion, a year-on-year increase of 19%, higher than analysts' expectations of $18.18 billion.

The increase in R&D is related to investments in AI, software, and systems, which will raise operating expenses in the short term but will help maintain product and ecosystem competitiveness in the long term.

Regarding cash flow and shareholder returns, Apple disclosed that it generated nearly $54 billion in operating cash flow in the fourth quarter, returning approximately $32 billion to shareholders through buybacks and dividends, indicating a strong short-term cash return. The company also announced a dividend of $0.26 per share.

On the cash flow and balance sheet front, Apple is in a very robust state, providing a backing for the company in new products, AI investments, or acquisitions, while also reducing liquidity risks from short-term external uncertainties.

From the "beat-and-raise" paradigm, the fourth quarter was truly a "strong season" for Apple, characterized by both scale and cash returns. The market will place greater emphasis on "structural momentum"—whether the iPhone lifecycle, service stickiness, and the sustainability of AI and new hardware routes can continue.

iPhone and Services Drive Growth; Mac and Wearable Device Revenue Declines

The financial report shows that Apple's total revenue from products such as phones, computers, and wearables in the fourth quarter was $113.74 billion, a year-on-year increase of over 15.6%, exceeding analysts' expectations of $107.69 billion.

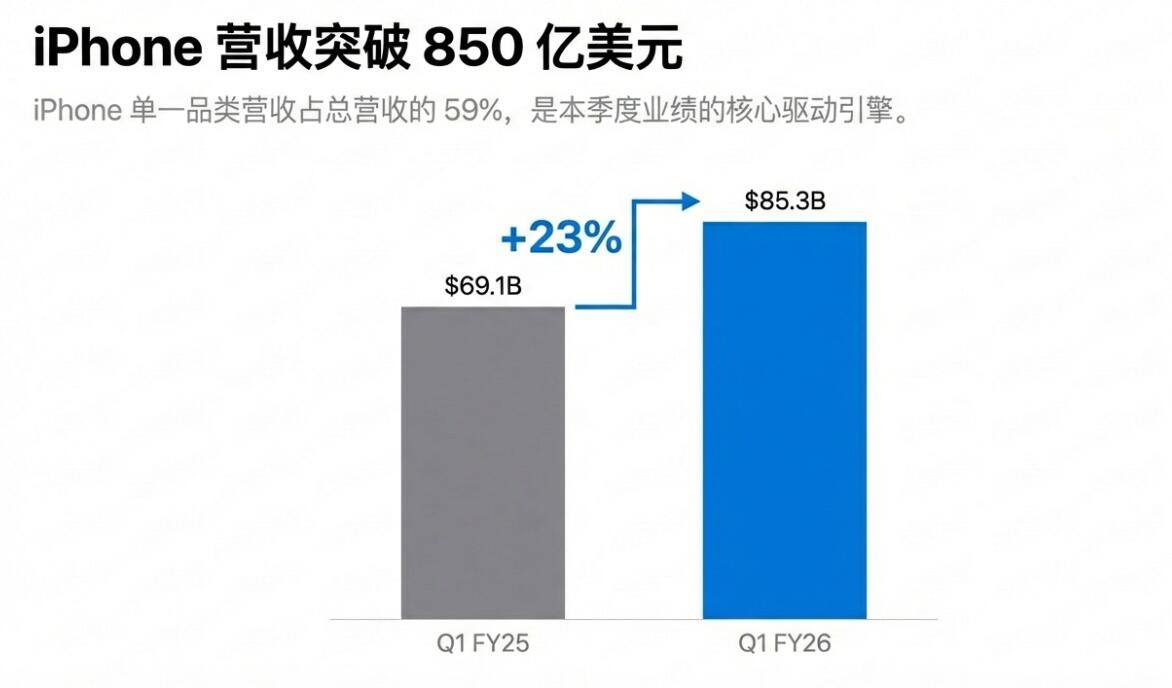

Among hardware products, iPhone revenue in the fourth quarter was $85.27 billion, accounting for nearly 60% of total revenue, becoming the largest engine of overall growth. The year-on-year growth rate of 23% was almost four times that of the third quarter, far exceeding analysts' expectations of $78.31 billion, justifying Apple's claim of the "best iPhone quarter ever."

iPad revenue was nearly $8.6 billion, a year-on-year increase of about 6.3%, with growth far exceeding the third quarter's 0.03%, and analysts' expectations of $8.18 billion Both Mac and wearable devices performed poorly. In the fourth quarter, Mac revenue was nearly $8.39 billion, a year-on-year decline of nearly 6.7%, which was over 8% lower than analysts' expectations of $9.13 billion, while analysts expected a year-on-year increase of about 1.6%.

Due to supply delays and competitive pressure, growth in wearable devices was limited in the fourth quarter. The combined revenue from wearables, home, and accessories in the quarter decreased by 2.2% year-on-year to approximately $11.49 billion, which was over 5% lower than analysts' expectations of $12.13 billion, while analysts expected a year-on-year increase of about 3.3%.

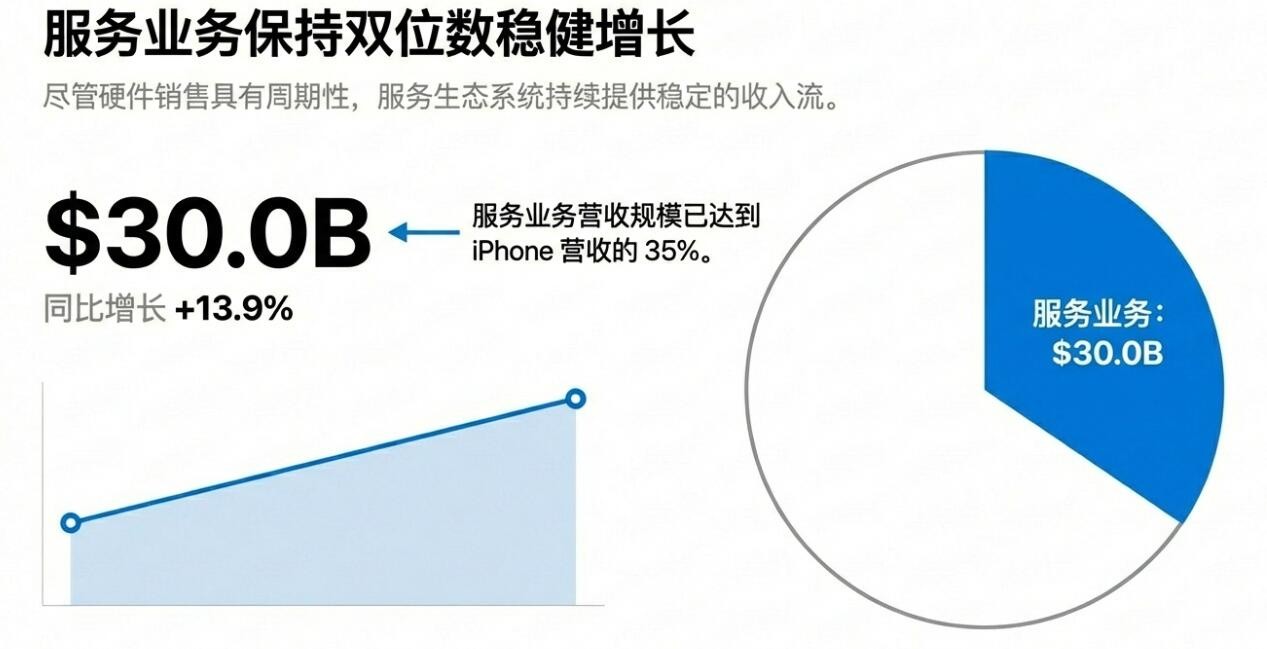

In the fourth quarter, service revenue was approximately $30.01 billion, a year-on-year increase of 14%, slightly below analysts' expectations of $30.02 billion. The high marginal characteristics of services amplified the impact on EPS.

Overall, in the fourth quarter, Apple relied on iPhone and service business, with a significant increase in iPhone sales driven by the synergy of high-end flagship upgrades (or channel restocking) and holiday promotions, but the growth elasticity of other hardware categories was limited. Investors need to assess whether the strength of the iPhone is a seasonal window (holiday demand, upgrade rhythm) or a structural improvement, such as AI features/software bundling driving long-term upgrades.

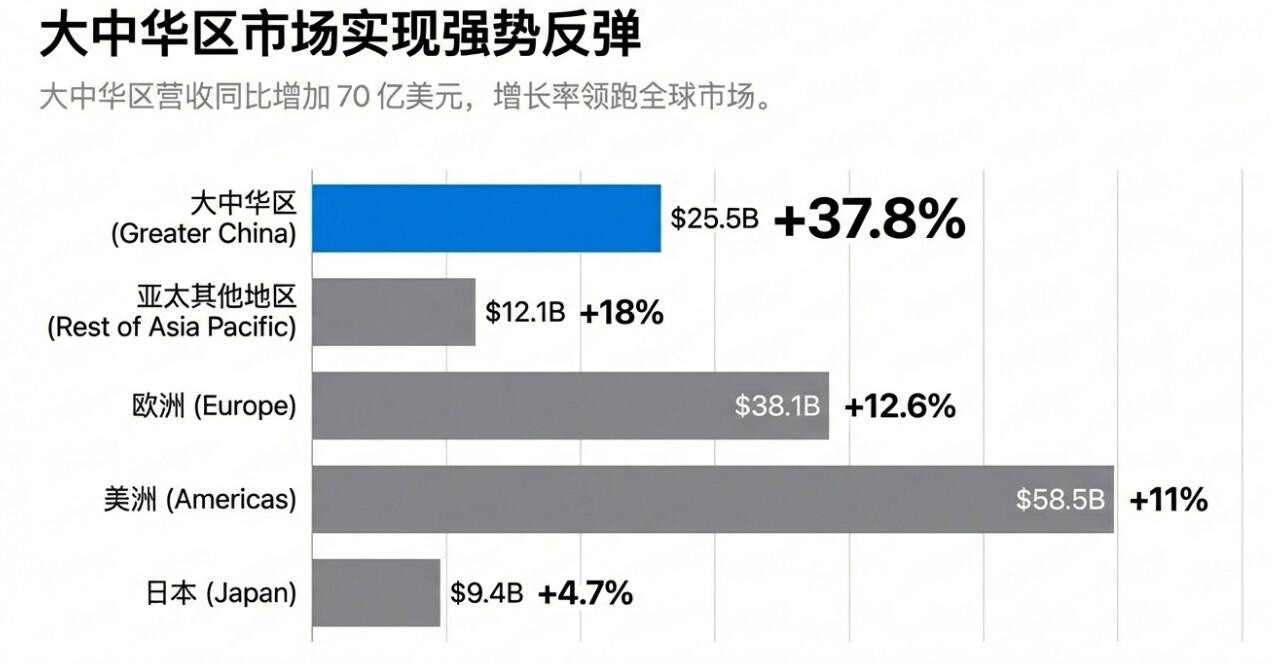

Greater China Becomes a Highlight, Only Americas Revenue Below Expectations Among Major Markets

From a regional market perspective, Greater China became a highlight in the fourth quarter, contributing significantly to Apple's revenue growth for the quarter.

In the fourth quarter, Apple recorded revenue of $25.53 billion in Greater China, which was 17% higher than analysts' expectations, with a year-on-year growth of 37.9%, reversing the unexpected year-on-year decline of 3.6% in the third quarter. Wall Street expected Greater China's fourth-quarter performance to rebound, but the growth rate was far below Apple's financial report performance. Analysts expected revenue in this market to be $21.82 billion, equivalent to a year-on-year growth of 17.9%.

Apple also recorded growth in other major markets in the fourth quarter, with only the performance in the Americas falling short of Wall Street expectations. Among them:

- Revenue in the Americas was $58.53 billion, a year-on-year increase of 11%, while analysts expected $59.06 billion;

- Revenue in Europe was $38.15 billion, a year-on-year increase of 13%, while analysts expected $36.82 billion;

- Revenue in Japan was $9.41 billion, a year-on-year increase of 4.7%, while analysts expected $9.24 billion.

The strong rebound in Greater China alleviated previous concerns about Apple's weak performance in the Chinese market, but attention needs to be paid to whether sustained growth can be maintained in the coming quarters under a high base, i.e., whether there are one-time restocking or promotional factors driving the growth.