After the historic crash, CME raises gold and silver trading margins again

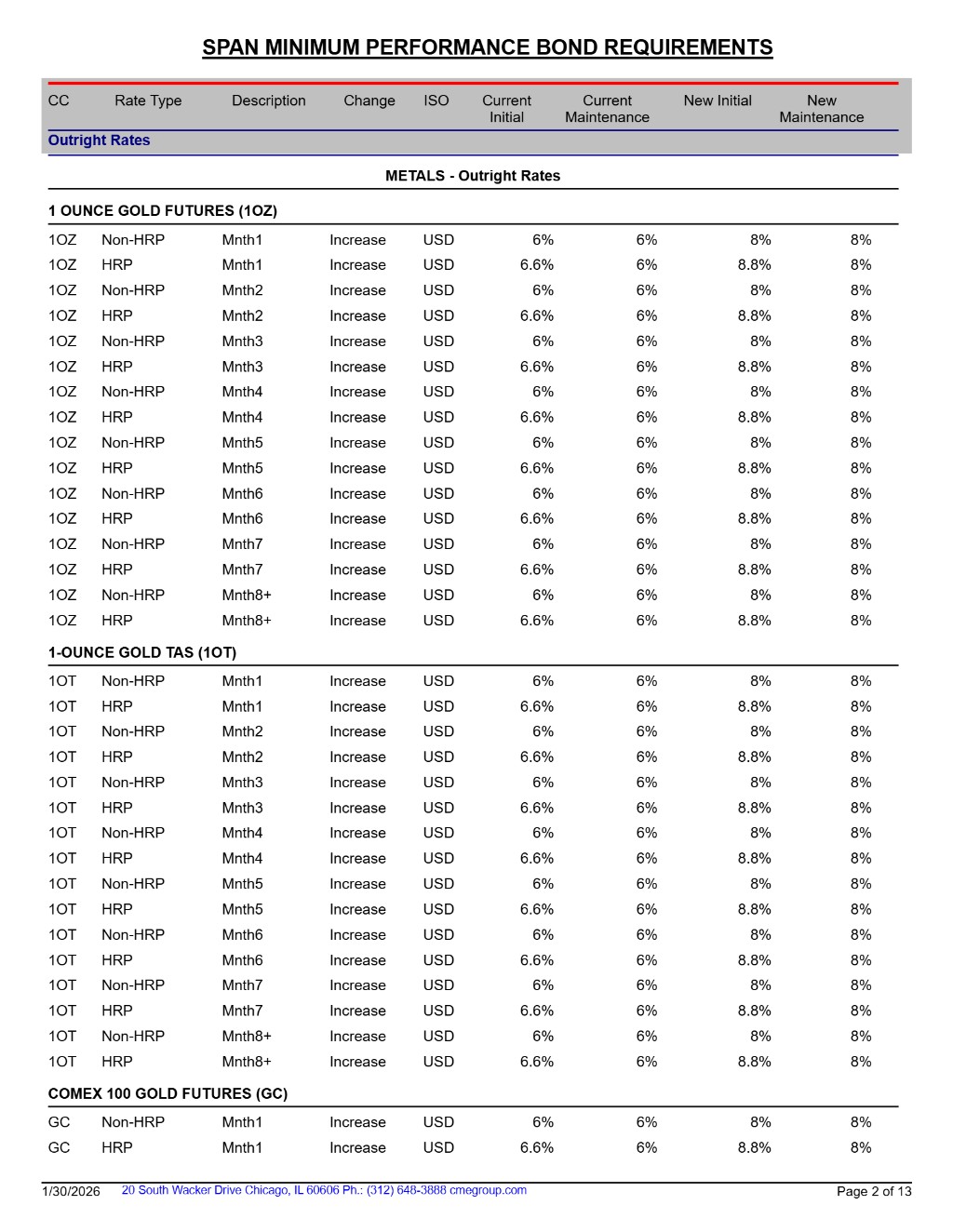

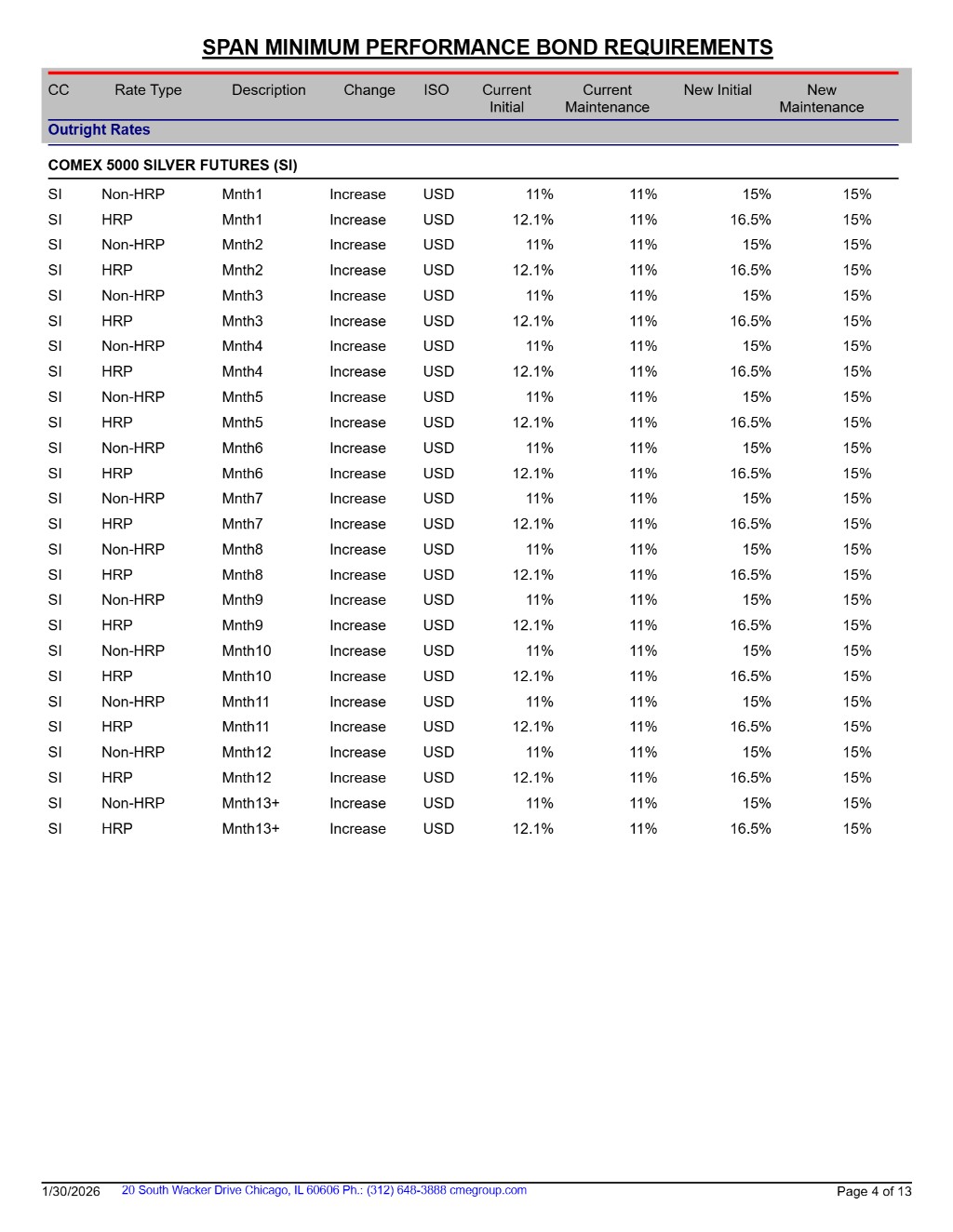

CME has once again significantly raised the margin requirements for precious metal futures: the gold margin rate has increased from 6% to 8%, and silver from 11% to 15%. The new rules will take effect after the market closes next Monday. This adjustment follows the recent reform of the "floating margin" mechanism, highlighting the exchange's intention to accelerate deleveraging and risk control in an environment of extreme volatility. The market is concerned about a repeat of the historical scenario in 1980 or 2011 where "the exchange's intervention led to a crash."

After the largest single-day drop in decades for gold and silver prices, the risk control measures of the exchanges were quickly implemented.

On Friday, the Chicago Mercantile Exchange Group (CME Group) announced that it would raise the margin requirements for Comex gold, silver, and other precious metal futures contracts.

CME stated in a press release that this adjustment is based on a "normal review" of market volatility, aimed at ensuring sufficient collateral coverage, and will officially take effect after the close of trading next Monday (February 2).

Margin Requirements Raised Across the Board, Significantly Higher than Previous Levels

According to the latest arrangements disclosed by CME:

Gold Futures:

-

Non-high-risk accounts: Margin ratio raised from 6% of the current contract value to 8%

-

High-risk accounts: Raised from 6.6% of the current contract value to 8.8%

Silver Futures:

-

Non-high-risk accounts: Raised from 11% to 15%

-

High-risk accounts: Raised from 12.1% to 16.5%

In addition, the margin requirements for platinum and palladium futures have also been increased.

This means that investors participating in precious metal futures trading will need to invest more cash or equivalent assets to maintain the same size positions.

A Continuation of Previous "Floating Margin" Reforms

It is worth noting that this increase is not an isolated event, but a continuation of a series of recent risk control upgrades by CME.

Wallstreetcn reported that in mid-January, CME had just completed an important mechanism adjustment: changing the margin calculation method for gold, silver, platinum, and palladium contracts from a fixed amount to a dynamic floating ratio based on the nominal value of the contract.

At that time, the reference ratios for some non-high-risk accounts were:

-

Gold approximately 5%

-

Silver approximately 9%

After this round of sharp declines, the actual execution ratios have been quickly raised to the range of 8%—16.5%, significantly increasing the capital occupation level.

This mechanism change is highly impactful in the current volatile market.

Under the old mechanism, the margin was a fixed dollar amount; under the new mechanism, the margin fluctuates with price and volatility. This means that during market turmoil, the system will automatically require higher collateral For traders, this not only means increased instability in capital occupation but also that during periods of high volatility, leverage will be forcibly reduced.

Margin will no longer just be a static risk control tool, but an "automatic deleveraging mechanism" that expands in sync with price and volatility.

On Friday, spot silver plummeted 31% in a single day, and gold fell 11%. For the recently battered long positions, the higher margin requirements coming into effect on Monday are akin to "salting the wound."

Exchanges Choose "Risk Control First"

CME stated that this adjustment was made after a routine assessment of market volatility.

Recently, the precious metals market has experienced rare and severe fluctuations: previously, gold and silver prices surged rapidly, followed by a historic level of sharp decline, with volatility significantly rising.

In this context, the direct effects of raising margins are:

-

Increasing leverage costs.

-

Compressing the margin for error in high-frequency, heavily leveraged trading.

-

Reducing the probability of settlement risk spreading within the system.

Exchanges have traditionally raised margins during sharp rises, falls, or extreme volatility in contracts, but this action occurring after a sharp decline further reinforces its risk firewall attribute.

The Ghost of History: Exchange Actions Often Mark Turning Points in Markets

Veteran traders on Wall Street are no strangers to this scene.

Wall Street Insights mentions that historical data shows when exchanges begin to intensively limit leverage by raising margins, it often marks the end of a frenzied market or the beginning of a sharp adjustment.

-

2011 Silver Price Crash: In 2011, as silver approached the historical high of $50 per ounce, CME raised margins five times in just nine days. This series of "cooling" measures forced a large-scale deleveraging in the futures market, leading to a nearly 30% drop in silver within weeks, followed by a multi-year bear market.

-

1980 Hunt Brothers Collapse: A more famous case is "Silver Thursday" in 1980. At that time, CME issued targeted "Silver Rule 7," strictly limiting leverage, which, combined with the Federal Reserve's interest rate hikes, directly broke the funding chain of the Hunt brothers who attempted to manipulate silver prices, causing silver to crash from $50 to $10.

Real Impact on the Market: Increased Pressure on Small Players

From a market structure perspective, raising margins does not directly determine price direction but profoundly affects the structure of participants and liquidity patterns.

Higher margin requirements mean:

-

Traders with weaker capital strength and reliance on high leverage may be forced to reduce positions or exit the market.

-

Market liquidity may further contract in the short term.

-

Volatility may actually be amplified in extreme cases.

CME also acknowledges that such adjustments may marginally squeeze out some traders who cannot quickly replenish margin.

Multiple actions this month, global exchanges tightening simultaneously

Looking at a longer timeline, CME's recent actions are not isolated.

-

Earlier this week, CME raised margin requirements for silver, platinum, and palladium futures due to price increases.

-

In the domestic market, the Shanghai Futures Exchange has also raised the price fluctuation limits and margin ratios for precious metal contracts.

In the context of significant amplification of global precious metal volatility, a consensus is forming at the exchange level: prioritize suppressing systemic risk rather than indulging in leverage expansion