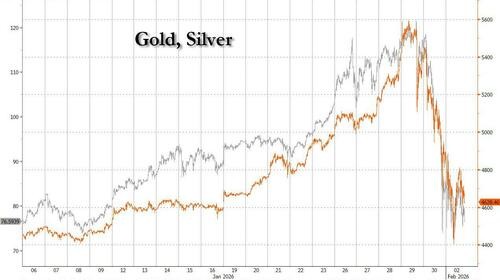

Gold and silver rebound, is it a "dead cat bounce" or a "bull market restart"?

Institutions are reducing positions due to extreme volatility and gold and silver breaking key trend lines, while retail investors are "bottom-fishing" in physical assets to form support. Whether the current rebound is a short-term "dead cat bounce" or a restart of the bull market depends on whether gold can stabilize above key resistance levels (such as around $5,100) and whether silver can break through the $92 resistance. The long-term bullish logic (central bank gold purchases, interest rate cut expectations, etc.) has not been overturned, but the market needs time to digest high volatility and rebuild technical structures

After experiencing a historic plunge and severe fluctuations, the gold and silver markets are at a critical crossroads. Despite a technical rebound in precious metal prices following a record sell-off, there remains a significant divide in the market over whether this is a temporary "dead cat bounce" or a recovery of a long-term bull trend. Institutional investors have significantly reduced their risk exposure due to extreme volatility, quantitative funds maintain a selling mode, while retail investors in the physical market show remarkable enthusiasm for "bottom fishing."

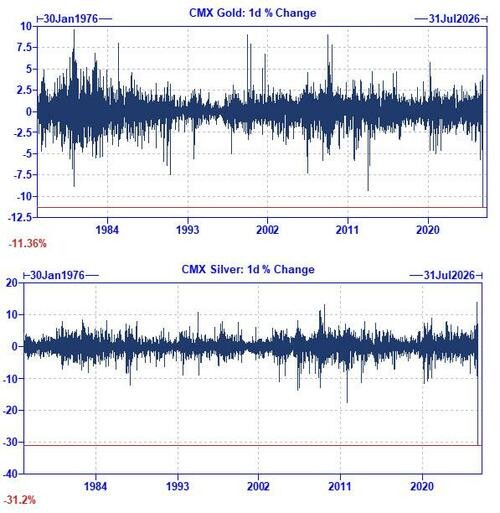

Recent market dynamics indicate that gold and silver prices are attempting to stabilize after a sharp correction. According to Goldman Sachs, this sell-off has exceeded previous extreme market conditions on certain indicators, with COMEX gold and silver recording their largest single-day declines since the early 1980s. Although prices have rebounded from their lows, volatility remains at a very high level, and options liquidity has at times dried up, indicating that the market structure remains fragile and may continue to face unstable bidirectional price fluctuations in the short term.

This turmoil has had a direct polarizing effect on market participants' sentiments. On one hand, Wall Street institutional traders are urgently reducing directional risk. Goldman Sachs' trading department noted that extreme volatility has made holding large positions "very uncomfortable," recommending a reduction in position sizes. On the other hand, demand in the physical market is exceptionally strong. According to Bloomberg, from Singapore to Sydney and to China's gold trading centers, a large number of retail investors are queuing up to buy gold bars and jewelry, attempting to take advantage of the price correction, and this strong retail buying has provided some support for gold prices.

Despite the unclear short-term outlook, mainstream institutions have not completely abandoned their long-term bullish views. Deutsche Bank reiterated its target price of $6,000 per ounce for gold, believing that macro drivers remain unchanged. Goldman Sachs' research department also maintains its forecast of gold prices reaching $5,400 by December 2026, citing continued central bank purchases and the potential for a Federal Reserve rate cut. The current market focus is on whether the resilience of physical demand is sufficient to offset the pressures from technical damage and institutional deleveraging.

Technical Damage and Quantitative Selling

From a technical perspective, the short-term outlook for precious metals still faces severe challenges. According to The Market Ear, gold recently fell below the 50-day moving average and the upward trend line during the turmoil, although the subsequent rebound pushed it back above the 21-day moving average, but clear resistance remains above. The initial resistance level is around $5,100, which roughly corresponds to the 50% retracement level of the previous large bearish candle (excluding shadows), and the 8-day moving average is positioned below it.

The technical recovery for silver appears to be even more difficult. Although silver prices have also rebounded, the trend is described as "quite weak." Silver is currently still constrained by the 21-day moving average above, with resistance around $92, and there is still a significant distance to retrace to the 50% level of the plunge candle (approximately the $100 area). The Market Ear points out that **silver volatility remains around 85%, suggesting an average daily fluctuation of up to 5.5%, and such extreme volatility requires a longer time to "cool down." **

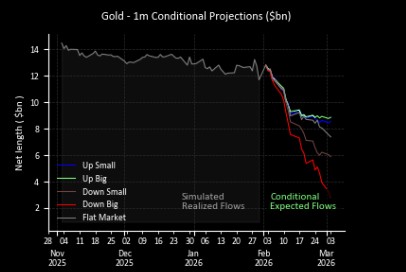

In addition, the movements of quantitative funds have intensified the downward pressure. According to Goldman Sachs' predictive model, Commodity Trading Advisor (CTA) strategies have shifted to sell or maintain sell modes for both gold and silver. Data from Menthor Q also shows that the silver market has experienced aggressive forced selling. Although high volatility may attract some strategies that sell volatility in search of enhanced returns, thereby stabilizing the market in the short term, gold prices may need time to consolidate before a new directional trend emerges.

Institutional Hedging and Risk Exposure Adjustment

In the face of unprecedented volatility, institutional investors have adopted a more cautious defensive posture. Goldman Sachs commodity trader Kim stated that the department has significantly reduced directional risk exposure. While the mid-term structural trading logic still exists, the rapid front-loading of investment demand has led to a price increase that is too fast, making the current holding of a large number of beta assets concerning. Kim pointed out that the volatility market has become misaligned, with the front-end volatility curve being very expensive, and advised investors to significantly reduce position sizes when trading, as the nominal value and volatility represented by "one ounce of gold" have far exceeded that of a year ago.

Jay Hatfield, Chief Investment Officer of Infrastructure Capital Advisors, noted that the market had shifted to momentum trading rather than fundamental trading weeks ago, and this crash is the result of a momentum collapse. Dominik Sperzel, trading director at Heraeus Precious Metals, admitted that this is the craziest market he has seen in his career; gold should be a symbol of stability, but such extreme volatility clearly deviates from that characteristic.

The "Bottom-Fishing" Frenzy in the Physical Market

In stark contrast to the caution of institutions, retail investors in the global physical market have shown a strong willingness to buy. According to Bloomberg, on the Monday following the plunge in gold prices, there were queues at the headquarters of United Overseas Bank (UOB) in Singapore as people rushed to buy gold bars, with products from well-known brands like MKS PAMP SA quickly selling out.

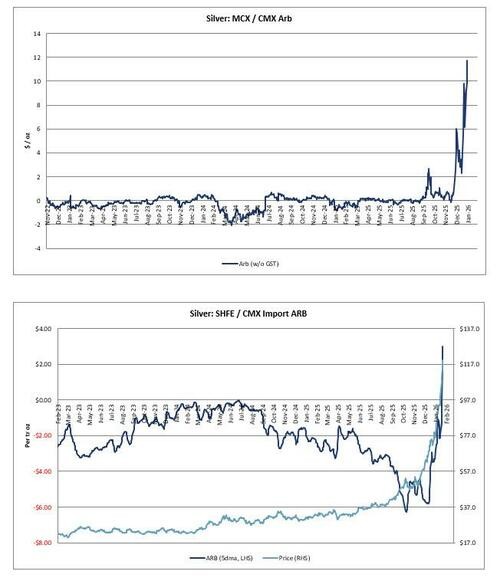

Similar scenes occurred in Sydney and Thailand. In Sydney, long queues formed outside ABC Bullion stores, despite investors suffering losses the previous Friday, some still viewed this as a good entry opportunity. In Thailand, Thanapisal Koohapremkit, CEO of Globlex Securities, stated that the local market continues to maintain a buying trend, with investors tending to hold positions and wait In China, the traditional consumption peak approaching the Lunar New Year has provided support for the market. Liu Shunmin, the risk manager of Shenzhen Guoxing Precious Metals Company, pointed out that a large number of bargain hunters have rushed in to purchase gold jewelry and gold bars over the past two days. However, the buying interest in the silver market is relatively weak. Goldman Sachs analysis indicates that physical buying in China and India has been an important driver of the previous rebound, the recovery of retail interest will be a key signal for market stabilization.

Long-term Bullish Logic Remains Unchanged

Despite facing a sharp setback in the short term, major financial institutions' long-term structural bullish view on gold remains unchanged.

Goldman Sachs commodity researcher Struyven maintains its forecast of a gold price of $5,400 by the end of 2026. This forecast is based on three core assumptions: central banks will continue to purchase gold at an average rate of 60 tons per month; the Federal Reserve will cut interest rates twice in 2026; and the private sector's allocation to gold will remain stable. Struyven emphasized that due to the uncertainty of global macro policies (such as the fiscal sustainability of developed markets), it is unlikely to be fully resolved by 2026, and with the low proportion of gold in investment portfolios, there is a high possibility that the private sector will further diversify investments into gold, which means that price risks still lean towards the upside.

Deutsche Bank also stated in a report on Monday that it will stick to its forecast of gold reaching $6,000 per ounce. Market views suggest that the core driving forces behind the rise in gold prices—including the unpredictability of Trump’s policies and investors' concerns about currency and sovereign bonds leading to "currency devaluation trades"—have not changed due to the price correction