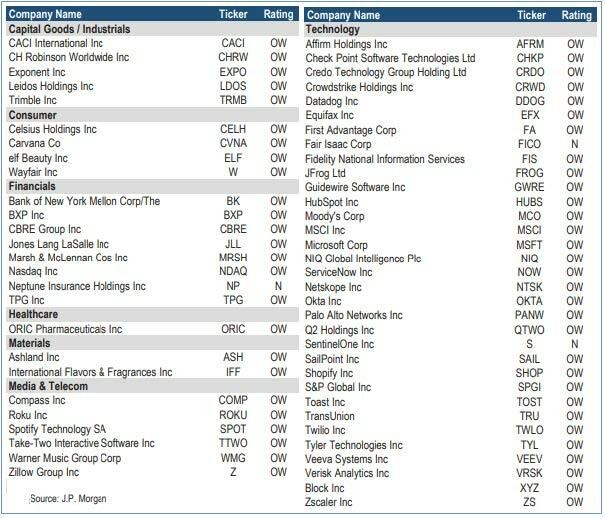

JPMorgan Trading Desk: The "sell first, ask questions later" AI sell-off in U.S. stocks is about to end, it's time to buy the dip in software stocks

The team is seizing the upcoming rebound opportunity by strategically investing in undervalued software stocks that have been mistakenly sold off and assets that are "immune to AI disruption."

In recent weeks, the core trading logic of the U.S. stock market has been simplified into a suffocating narrative—“AI substitution risk.” This extreme fear of being “replaced by AI” has triggered severe turbulence in the financial and industrial sectors, leading to a frenzy of capital flowing into semiconductors while software stocks are indiscriminately “sold first and asked questions later.”

However, the latest report from the JP Morgan trading desk on February 17 suggests that this extreme emotional outburst is nearing its end. The team is positioning itself to capitalize on the upcoming rebound by reversing the layout of software stocks that have been unfairly punished and assets that are “immune to AI disruption”:

“Although the short-term market pattern remains unchanged, the narrative of ‘AI substitution’ is nearing its end, which means the bottom-fishing window for large tech stocks has opened.”

The market is overreacting across multiple sectors

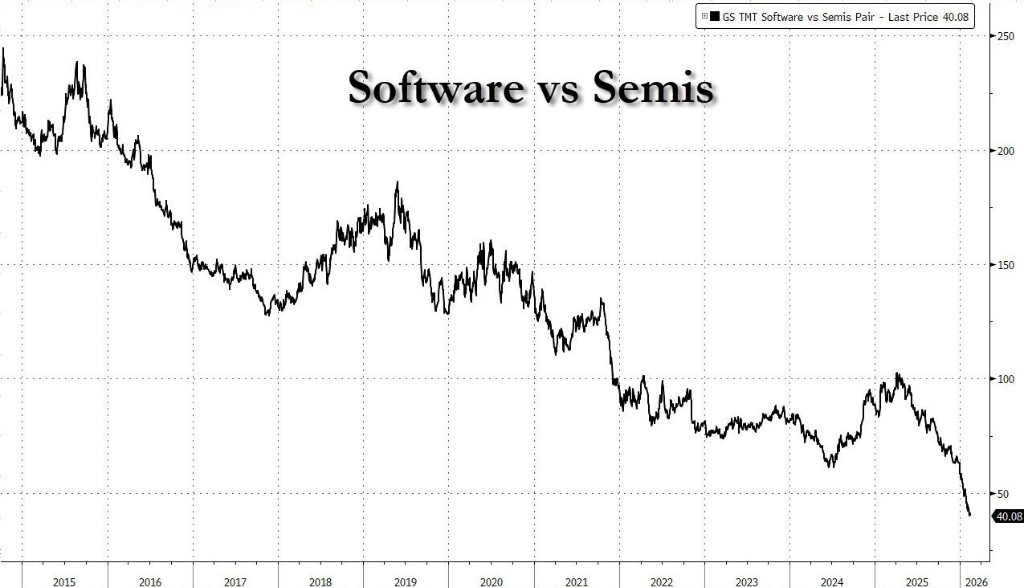

The JP Morgan positioning intelligence team has observed that the current U.S. stock market shows a crowded positioning in the semiconductor sector at +4 standard deviations (+4z), while the software sector is deeply entrenched in a low at -3.5 standard deviations (-3.5z), with the positioning difference between the two sectors reaching a historical extreme.

Since the beginning of the year, the return from going long on semiconductors and shorting software has reached approximately 34.9%. This rift stems from a linear thinking among investors: AI computing power is the only winner, while traditional software will be completely disrupted.

In the latest report, JP Morgan's sector analysts conducted an in-depth analysis of this AI sell-off, concluding that there is a clear overreaction in multiple areas of the market:

1. Software Industry: The “Negative Logic” That Is Hard to Disprove

Analyst Mark Murphy points out that the current dilemma is that software companies find it difficult to “prove their innocence”—that is, to demonstrate that AI will not disrupt them in the coming years. Although industry growth has slowed due to macroeconomic headwinds, considering that valuations have significantly retracted, investors are advised to adopt a “barbell strategy”: on one hand, allocate to top software companies with strong free cash flow (FCF) support, while on the other hand, avoid overvalued targets.

2. Wealth Management and Life Sciences: Profit Expansion vs. Recent Risks

Last week, large bank stocks (JP2LBK index) fell by 6%, and merger brokers plummeted by 7%. However, the fundamental feedback is starkly opposite: loan growth is strong, and the merger and IPO pipeline is robust. Analyst Rob O’Dwyer believes that the market underestimates the value of “relationships” in wealth management. In fact, for wealth management firms, AI is more likely to be a tool for enhancing profit margins rather than a killer of client relationships.

In the life sciences tools sector, this is currently a field with clearer risks. CRO companies (such as MEDP) have acknowledged that pharmaceutical clients' internal use of AI to enhance productivity may reduce the demand for outsourcing services. This may be one of the few sectors where the negative logic of AI holds true 3. Logistics Transportation: The Panic of AI "Disintermediation"

The logistics sector has been a major victim of the recent AI panic. The announcement by competitor Algorhythm Holdings that its AI platform SemiCab can significantly enhance freight scheduling efficiency (one operator can manage 2,000 orders, four times that of traditional brokers) led to a 25% plunge in the stock price of American freight giant CHRW, dragging down global peers like DSV and DHL by about 10%.

JPMorgan analyst Alexia Dogani is skeptical about this. She pointed out that freight forwarding involves complex physical infrastructure integration, and the current level of digitization is extremely low. While AI can improve efficiency, it cannot achieve complete "disintermediation" in the short term due to physical barriers.

4. Japanese Market: AI Will Not Replace Outsourcing in the Short Term

The same logic applies to the Japanese IT services market.

Analyst Matthew Henderson noted that large Japanese enterprises are heavily reliant on system integrators (SIers) and face a severe talent shortage. In this structural stalemate, AI will not replace outsourcing; rather, it will become a tool to alleviate talent shortages and enhance SIers' profit margins.

Bottom Fishing in Software Stocks?

JPMorgan's trading team wrote in a report that although the short-term market landscape remains unchanged, the narrative of "AI replacement" is nearing its end, which means the bottom-fishing window for large tech stocks has opened. The specific trading strategies recommended by the team are as follows:

-

Core Themes: Continue to be optimistic about AI/TMT, global growth restart, international market opportunities, and dollar depreciation trades.

-

Hedging Risks: Recommend going long on oil and energy stocks to hedge against geopolitical risks; buy volatility; short momentum factors.

-

Self-Operation: The trading desk is executing a long strategy, going long on a basket of stocks that are "severely mispriced and immune to AI disruption."