Under the impact of AI, is a new round of "subprime mortgage crisis" coming?

The impact of AI is causing turmoil in the credit bond market, with emerging risk transmission paths similar to those of the subprime mortgage crisis: a sharp decline in loans in the software industry has led to the largest drop in the leveraged loan index in nearly three years, with CLO underlying assets amounting to $150 billion facing the risk of AI disruption. However, the current shock is still concentrated in the technology sector and has not yet evolved into a systemic wave of defaults

Concerns triggered by the disruption of artificial intelligence technology are rapidly spreading to the global credit bond market. From leveraged loans to collateralized loan obligations (CLOs), the asset sell-off across various sub-markets is raising investors' awareness of systemic credit bond cycles.

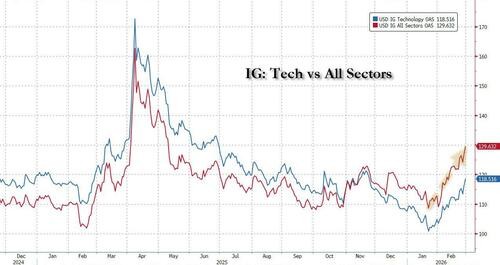

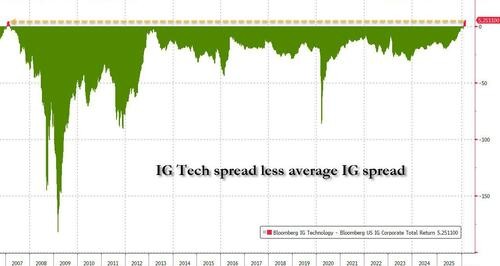

According to Bloomberg indices, the yield premium on comparable global debt has recently widened by nearly 4 basis points, marking the largest increase since early November last year. The investment-grade bond market, long regarded as a safe haven, is showing signs of pressure, with spreads on investment-grade tech stocks rapidly widening. For the first time since the global financial crisis, the robustness of the tech sector is considered to be lower than that of the broader investment-grade index.

Meanwhile, Wall Street institutions are warning that the default risk for highly leveraged borrowers in the AI and software industries is rising. Investor concerns have translated into actual sell-off actions, with leveraged loans in the tech sector underperforming the overall market. U.S. junk bond funds have also seen continued outflows in recent weeks, putting an end to the months-long rally in high-yield bonds.

Although the current volatility in high-rated credit indicators is relatively mild, the high correlation between private credit bonds and the public market means that once core industries like technology are hit, the default risk will quickly spread, affecting the broader global credit bond sector.

Latest market data shows that in February this year, the average price of the Bloomberg U.S. Leveraged Loan Index fell by 1.34%, marking the largest monthly decline since September 2022, primarily dragged down by loans in the software and services sector, leading to a significant amount of debt falling into poor condition. Meanwhile, JP Morgan warns that U.S. CLO asset pools, ranging from $40 billion to $150 billion, are facing the impact of AI disruption risks.

Investment-Grade and High-Yield Bond Spread Movements

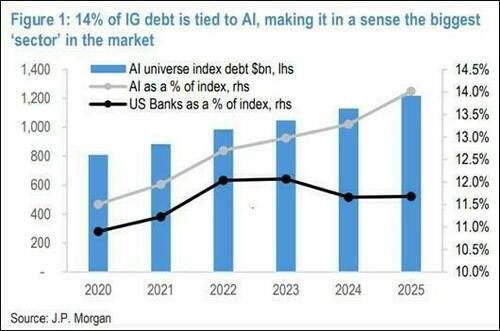

The investment-grade bond market, once seen as a safe-haven tool, is also showing rare cracks. According to JP Morgan data, companies related to AI currently account for 14% of the investment-grade index, with related debt rapidly swelling to $1.2 trillion, surpassing the U.S. banking sector to become the largest segment in the index. As the market comes under pressure, the spread between tech-related investment-grade bonds and the overall market index has significantly widened.

This credit bond crack is affecting the globe. According to Bloomberg indices, the yield premium on Asian investment-grade dollar bonds has recently seen the largest weekly increase since November last year. Clement Chong, head of fixed income credit research for East Asia, stated that valuations in the Asian market have tightened in sync with the U.S., making it unable to escape local volatility.

Junk Bonds and Leveraged Loan Market Under Pressure

As investor concerns about default risks in the software industry intensify, the higher-risk credit bond sector is at the forefront. Following several recent high-yield bond issuances, investors rushed to sell, putting pressure on junk bond prices According to LSEG Lipper data, U.S. junk bond funds have experienced consecutive weeks of outflows.

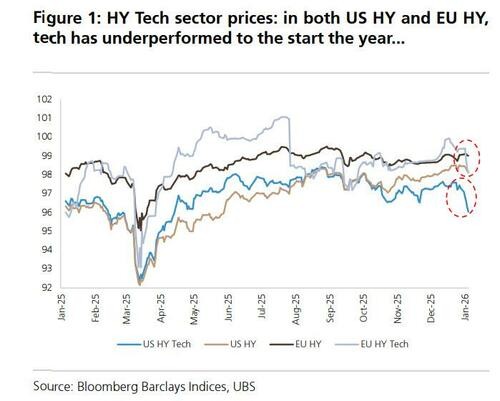

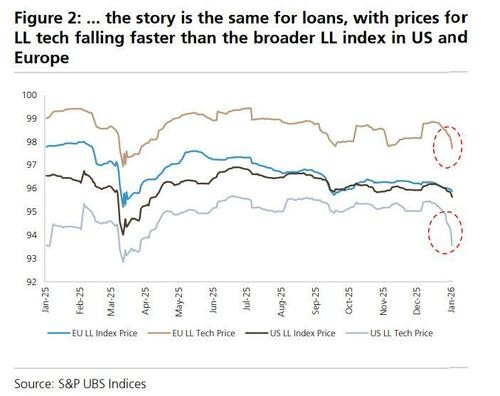

In addition, the leveraged loan market in the technology sector is also showing weakness, with declines exceeding those of broader leveraged loan indices in the U.S. and Europe. A series of recent events in the credit bond market, such as the collapse of the UK mortgage company Market Financial Solutions, as well as the bankruptcies of First Brands Group and Tricolor Holdings, have further intensified concerns about the loosening of underwriting standards for credit bonds, leading to speculation about assets being re-pledged.

The Spread Risk of Private Credit Bonds to the Public Market

Deeper market concerns revolve around the systemic contagion risk potentially triggered by private credit bonds. UBS has warned that due to borrowers frequently obtaining dual financing in both private and syndicated loan markets, there is a high overlap in issuers and industry exposure between the two. Data shows that the service and technology sectors account for 15% to 20% of leveraged loan portfolios, a proportion that is highly consistent with the characteristics of the private credit bond market.

UBS credit strategist Matthew Mish pointed out that the top 20 direct lending institutions not only dominate the asset management scale of private credit bonds but also hold significant positions in business development companies (BDCs), leveraged loans, and high-yield bonds. This close interconnectivity means that if the AI shock leads to a surge in default rates in sectors like software, the contagion effect will quickly spill over into the public market, resulting in wider spreads and impaired liquidity, thereby posing a substantial test to the capital adequacy ratios of global banks and insurance companies during economic downturns.

In his report, Matthew Mish summarized that while the private credit bond market has not yet fully fallen into crisis, the seeds of a crisis have already been sown. The key trigger will be shocks to important industries such as software. Due to issues like high leverage, industry concentration, and limited transparency in information disclosure in the private market, accurately assessing macro risks has become extremely difficult. Investors need to closely monitor leading indicators such as default rates and valuation changes to guard against potential systemic risks.

The Leveraged Loan Market is Rapidly Cooling

Leveraged loans, as an important source of financing for companies below investment grade, are bearing the brunt of the initial pressure from the AI shock. According to Bloomberg, concerns about traditional business models being disrupted by AI have led to a significant impact on borrowers that heavily rely on software businesses. As loan prices fall to multi-month lows, the number of new loans in the U.S. has also plummeted to its lowest level since May of last year.

JP Morgan strategists point out that refinancing risks in the software sector are intensifying. Data shows that approximately $51 billion of software debt rated B- or below will mature in 2028, with another $50 billion maturing in 2029. Due to the current limited capacity of the private credit bond market to absorb syndicated assets, these debts will face severe refinancing challenges in the future.

CLO Asset Pools Sound the AI Risk Alarm

The underlying asset risks of leveraged loans are directly transmitting to structured products. Previously, the release of Anthropic PBC's powerful Claude chatbot triggered a sell-off in software loans, prompting CLO managers to urgently reassess their AI exposure in their portfolios. According to JP Morgan analysis, approximately $40 billion to $150 billion of CLO loans are facing disruption due to their exposure to industries highly correlated with AI risks.

JP Morgan strategist Rishad Ahluwalia stated that in addition to focusing on the software industry itself, investors should consider the broader impact of AI disruption on the overall credit risk of CLOs. Strategists noted that while economists expect the penetration of AI into the economy to be gradual, the over-leveraging of financial markets in the AI sector could trigger uncomfortable expectations resets