The stock price of PE giants continues to plummet, with "storm center" Blue Owl's stock price halving in a year, having fallen below its "initial public offering price."

Affected by the investor redemption wave and concerns over the impact of AI on software companies, Blue Owl's stock price fell below the $10 listing price on Tuesday, having plummeted approximately 50% over the past 12 months. The company permanently closed the redemption channel for its retail debt fund and sold assets to survive, leading to a collective decline in the stock prices of private equity giants such as Blackstone and Apollo. Wall Street moguls warn that the private equity market is facing a "reshuffling," and the risk management model overly concentrated in a single industry is facing severe challenges

Due to intensified investor redemption waves and concerns about the potential impact of AI technology on software companies, Blue Owl Capital, a private credit giant managing over $300 billion in assets, has seen its stock price continue to plummet, falling below its IPO price, highlighting the severe liquidity challenges facing the private capital market.

On Tuesday, March 4, Blue Owl's stock price dropped as much as 9% to $9.73, falling below the $10 pricing at which it went public through a SPAC transaction in 2021. Over the past 12 months, the asset management company's stock price has cumulatively fallen by about 50%, significantly shrinking its market capitalization.

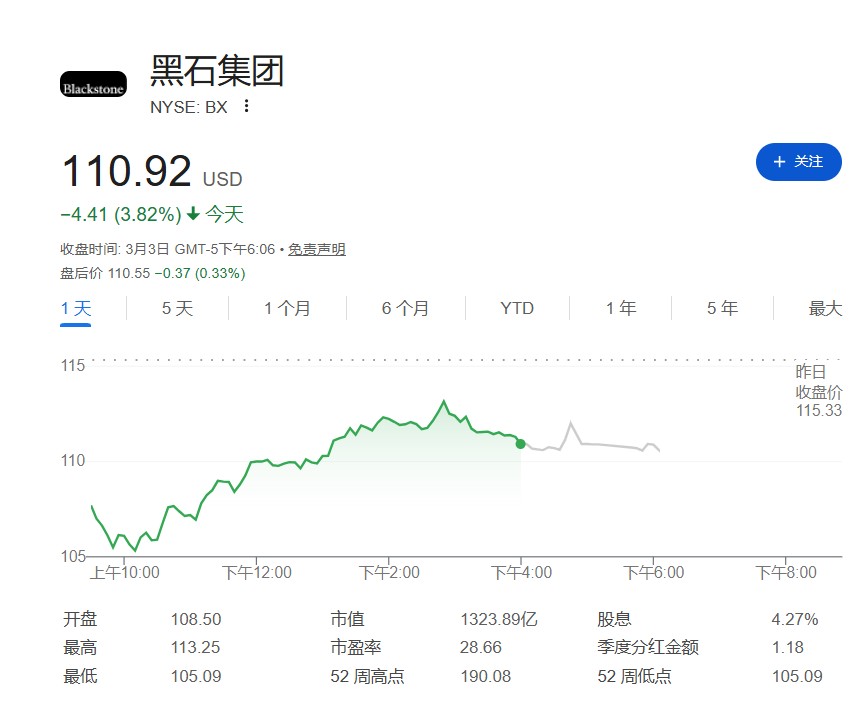

Panic quickly spread throughout the industry, leading to a collective decline in the stock prices of private equity giants. On Tuesday, Blackstone's stock price fell nearly 9% at one point, ultimately closing down nearly 4%, while Apollo Global Management dropped 6% and KKR fell 4%, all significantly exceeding the broader market decline. Previously, Blackstone's $82 billion private credit fund Bcred disclosed a net outflow of $1.7 billion in the month ending March 2.

Blue Owl positions itself as "one of the largest lenders" to software companies supported by private equity. Its flagship technology fund, Blue Owl Technology Finance (OTIC), concentrates up to 56% of its assets in software and technology service companies, far exceeding the average level of similar funds.

Under the impact of AI, the risk of software defaults is increasingly high. As Blue Owl permanently restricts cash withdrawals from its first private retail debt fund, market concerns about investment tools heavily invested in tech loans and facing liquidity constraints are rapidly escalating.

Redemption Wave Spreads, Industry Giants Under Pressure

Investor redemption requests for private credit funds have surged in recent months. In addition to Blue Owl, industry competitors, including Blackstone, have not been spared. The accelerated outflow of funds directly reflects the market's deep unease about the loan values of tech companies in the unlisted market.

According to Apollo, loans to mid-sized tech companies accounted for nearly one-third of all private loans over the past decade, with a higher proportion of 40% in private equity transactions. These loans are often supported by private equity groups, and now these software companies are facing direct threats from advancements in AI technology.

Last week, publicly listed private credit funds managed by KKR, Apollo, and BlackRock also experienced declines. According to the Financial Times, these funds reported an increasing number of non-performing loans in their portfolios and were forced to cut dividends to cope with declining interest income and asset impairments.

Liquidity Crisis, Blue Owl Forced to "Cut Off Its Arm to Survive"

The crisis at Blue Owl began to emerge last fall. At that time, its retail credit fund named OBDC II closed its redemption channel, planning to merge with a larger listed vehicle. However, reports indicated that the deal would expose investors to direct paper losses, and it was quickly halted after media exposure.

Last month, Blue Owl made a shocking decision to permanently restrict cash withdrawals from the fund, abandoning plans to reopen redemptions this quarter. The company announced that it would prioritize providing liquidity to all shareholders proportionally through quarterly capital allocation.

To address the crisis, Blue Owl conducted a $1.4 billion sale of credit assets involving three of its funds, with $600 million coming from its retail credit fund. Although the company was able to sell about one-third of the fund's assets at close to par value, this policy shift has completely exposed the significant risks faced by individual investors pouring into liquidity-constrained instruments.

Wall Street Warns of Approaching "Shakeout" Moment

Blue Owl was founded by Wall Street veterans Doug Ostrover and Marc Lipschultz, and its assets under management once soared to $307 billion. Today, this once-hot institution is seen as a bellwether for the market. Economist Mohamed El-Erian likened Blue Owl's crisis to the "canary in the coal mine" before the 2008 financial crisis. Orlando Gemes, Chief Investment Officer of hedge fund Fourier Asset Management, also warned, "The alarms we see in private credit are strikingly similar to those in 2007."

In the face of industry turmoil, Apollo CEO Marc Rowan issued a stern warning at a Bloomberg-hosted conference on Tuesday, pointing out that the private market is about to undergo a "shakeout." He emphasized that there will be a severe divergence in the performance of fund managers in the future.

"There will always be underwriting errors," Marc Rowan stated bluntly, "but the question is, who are the good risk managers and who are not? If you have 30% of your portfolio concentrated in one industry, and that industry is being disrupted by technology, then you are not a good risk manager."