Goldman Sachs warns: The current market is just "unstable stability," and credit "cockroaches" are scarier than crude oil

Goldman Sachs warns that the current market appears calm on the surface, but there are undercurrents. The pressure in the credit market is mainly concentrated in the financial sector, especially among institutions related to private credit. Credit spreads have widened by 39 basis points, indicating weak performance of financial bonds. Compared to the energy sector, the credit performance of the financial sector is more fragile. The market is transitioning from the "shock" pricing phase to the "economic impact" pricing phase, and the "cockroach effect" of private credit may be a deeper concern

As the situation in the Middle East stirs the commodity markets, the credit market is quietly undergoing a more concerning divergence. Goldman Sachs' credit strategy team has issued a warning that beneath the surface calm of the current market, there are undercurrents, and this "steady state" is essentially not stable.

Compared to the volatility in the stock and commodity markets, the credit market has shown unusual resilience over the past three weeks—stocks have only retreated about 5% from historical highs, and the widening of credit spreads has also been quite limited.

However, Goldman Sachs strategists Reid Zhou and his credit strategy team believe that the market is transitioning from a "shock" pricing phase to an "economic impact" pricing phase, and the current calm resembles a stalemate rather than true stability.

It is noteworthy that the main pressure in the credit market does not come from the energy sector but is concentrated in the financial sector, particularly institutions related to private credit. Bonds associated with Blue Owl, FS KKR, and private credit funds have performed the worst, with financial bond spreads widening by 39 basis points this year.

This signal has raised alarms among market participants: behind the noise of oil price fluctuations, the "cockroach effect" of private credit may be a deeper concern.

Credit Divergence: Financial Sector Pressure Far Exceeds Energy

According to Bloomberg, the expansion of U.S. credit spreads began before the outbreak of the current Middle Eastern conflict, and a significant characteristic of this round of credit sell-off is its high consistency across industries and ratings.

The only exception is not energy but finance. The spreads on bonds from financial services companies have widened by 39 basis points this year, with issuers related to Blue Owl, FS KKR, and private credit funds showing the weakest performance.

The credit performance of the energy sector has actually been relatively strong this year, but its outperformance was mainly concentrated in February—before the conflict erupted. This sharply contrasts with the stock market: in the stock market, the energy sector has significantly outperformed other sectors since the conflict began.

Specific data shows that among BBB-rated U.S. dollar bonds, the spread difference between the energy and financial sectors was only 2.4 basis points at the beginning of the year, which had widened to 13.5 basis points before the conflict erupted on February 26, and has now further expanded to 18.5 basis points. The continued pressure on private credit is becoming the most dangerous variable in the entire credit market.

"TACO Game": Market and Policy Watching Each Other

Goldman Sachs' team summarizes the current market stalemate as a "which came first, the chicken or the egg" problem.

The market has adopted "TACO" (Trump Always Chickens Out) as an expectation anchor, thus not selling off significantly; on the other hand, the policy side is also remaining inactive because the market has not yet experienced large-scale turmoil.

Goldman Sachs points out: "We are in an extremely delicate steady state, but the background is highly unstable; this is a game where whoever moves first loses."

The strategy team believes that this steady state may last longer than expected, but it is ultimately transitional. The market's volatility in interest rates has rapidly climbed from the 10th percentile historically to nearly the 70th percentile, reflecting the rapid digestion of the shock phase; However, the widening interest rate spread remains relatively restrained, and the flow of funds is basically balanced.

Triple Vulnerability of Stability: Fund Flow, Positioning, and Irreversible Damage

Goldman Sachs analyzed the inherent vulnerabilities of the current stability from three dimensions.

First, the fundamental support still exists, but position pressure is accumulating. The current credit fundamentals still provide support, and the overall issuance of new bonds has been fully digested by the market, with full-return buying remaining in place. At the same time, CTA strategies have de-risked, and some hedging positions have been unwound, alleviating the degree of valuation and position crowding. However, this also means that once the next round of risks arrives, investors' cushion will be thinner.

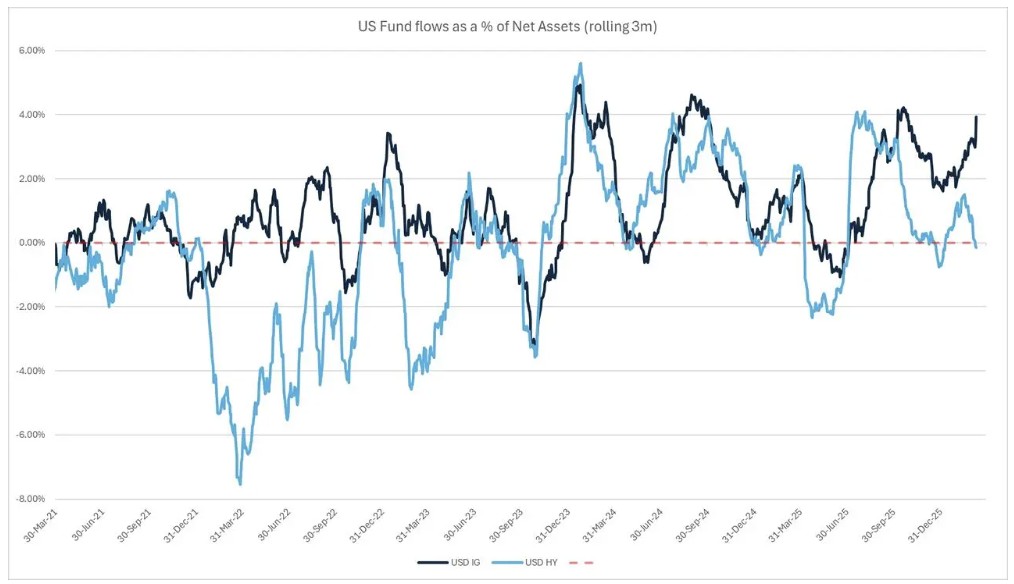

Second, the risk of capital outflow from high-yield bonds is rising. Recently, there have been signs of capital outflow from high-yield bonds. If the outflow continues, credit beta will accelerate downward attachment. Goldman Sachs specifically pointed out that under the circumstances where previous hedging positions have been unwound, investors' vulnerability to a new round of spread widening is increasing.

Third, some damage is irreversible. Even if there are policy concessions in the future, the credit market will not simply return to the state before the conflict. Goldman Sachs believes that any phase of rebound may be gradually digested in the medium term, although this process will unfold in a more controllable manner rather than a rapid reversal.

Goldman Sachs' Trading Strategy: Short Basis, Sell Volatility

Based on the above judgments, Goldman Sachs' credit strategy team provided specific positioning recommendations.

First, shorting the basis (going long futures, shorting spot) is seen as an optimal strategy that accommodates multiple scenarios: if the market experiences a short squeeze rebound, the futures side should outperform the spot due to leverage squeeze (basis narrowing); if the spread enters a second round of widening, forced selling will put pressure on the spot, underperforming the futures (basis also narrows).

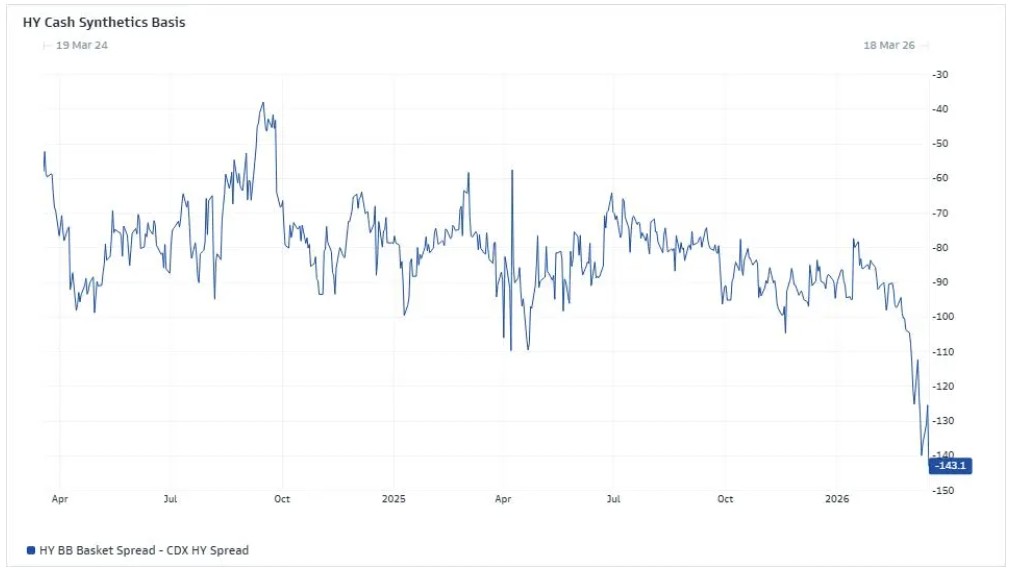

In terms of specific varieties, Goldman Sachs prefers high-yield bonds over investment-grade bonds. One suggested reference combination is to short the high-yield BB basket GS2BATAS swaps while going long CDX HY45. Compared to establishing a short position by shorting HYG through securities lending, using basket tools to construct short positions incurs lower costs.

In terms of volatility strategy, Goldman Sachs continues to favor selling credit volatility, which can be achieved through at-the-money straddles or STS strategies. Given that recent volatility has surged from below the 10th percentile to nearly the 70th percentile, the team prefers to use single-option directions combined with long gamma positions in the spot market instead of straddles, to capture non-linear returns while controlling costs Risk Warning and Disclaimer

The market has risks, and investment should be cautious. This article does not constitute personal investment advice and does not take into account the specific investment goals, financial situation, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances. Investment based on this is at one's own risk