CPO Commercialization Accelerates: Scale-out Breaks Through 0 to 1, Will Scale-up Lead in Large-Scale Implementation?

CPO commercialization is accelerating, driven by industry leaders like NVIDIA and Broadcom. Western Securities believes that on the Scale-up (vertical expansion) side, leading manufacturers are leveraging vertical integration to drive implementation, with higher urgency for commercialization and critical supply-side capacity bottlenecks. On the Scale-out (horizontal expansion) side, CPO commercialization has achieved a "0 to 1" breakthrough, with penetration expected to rise gradually, though the commercialization pace remains relatively steady

To stand in the light, don't just stand there. In the CPO concept sector today, InnoLight and Zhongji Innolight hit ATH (All-Time Highs), VOGUE OPTICS hit its daily limit, and Zhongfu Circuit followed suit.

Co-packaged Optics (CPO) technology is moving from laboratories to large-scale commercial use. The power consumption and bandwidth bottlenecks brought about by the explosion of AI computing power are pushing this technology to the core of data center construction.

According to the latest in-depth report on the optical module industry released by the R&D center of Western Securities, the commercialization process of CPO has significantly accelerated with the promotion of leading manufacturers such as NVIDIA and Broadcom.

On the Scale-up side, since NVLink and other vertical expansion networks belong to proprietary closed systems, leading manufacturers have vertical integration capabilities to promote CPO implementation. The urgency for commercialization is higher, but the yield and capacity bottlenecks on the supply side are equally critical.

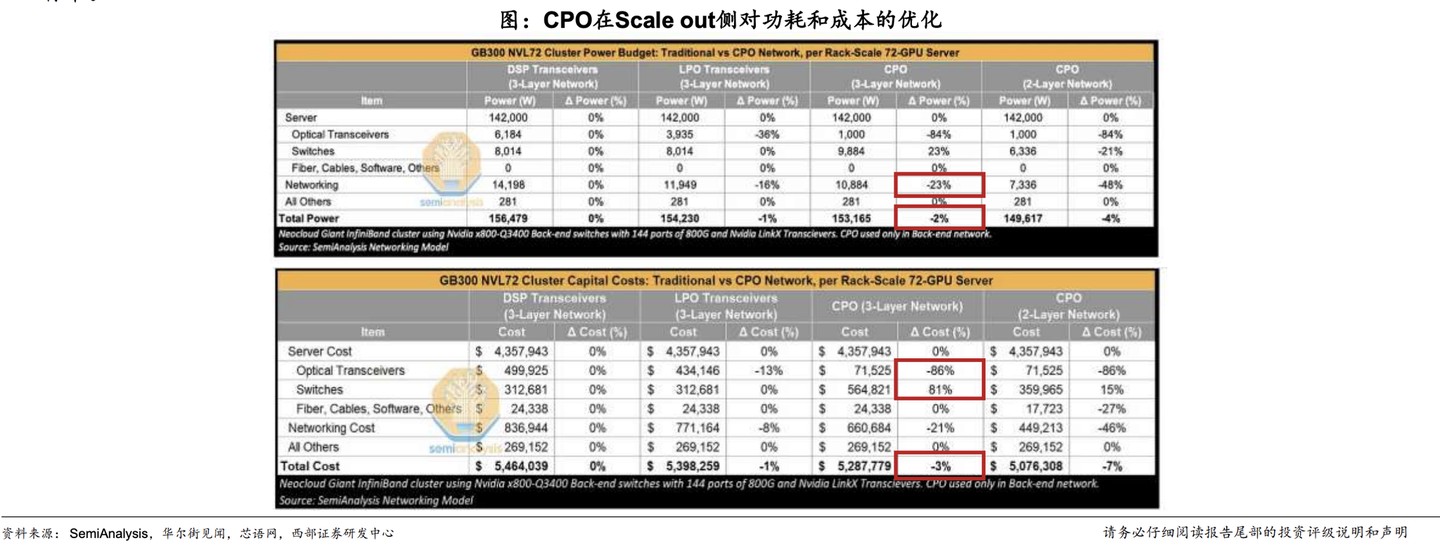

On the Scale-out side, CPO commercialization has achieved a 0-to-1 breakthrough, and its penetration rate is expected to gradually increase; however, the improvement in power consumption and cost is relatively limited (total power consumption optimized by only 2% and total cost optimized by only 3% in a three-layer network architecture), and the pace of commercialization is relatively steady.

At the same time, the CPO switch supply chain is highly fragmented, with lasers, ELS modules, optical-electrical testing, and other segments involving multiple suppliers. It is recommended to focus on segments with clear divisions of labor that have already participated in joint R&D with CPO switch manufacturers or have order expectations, such as high-power CW light sources and FAUs.

Core Advantages and Practical Shortcomings of CPO

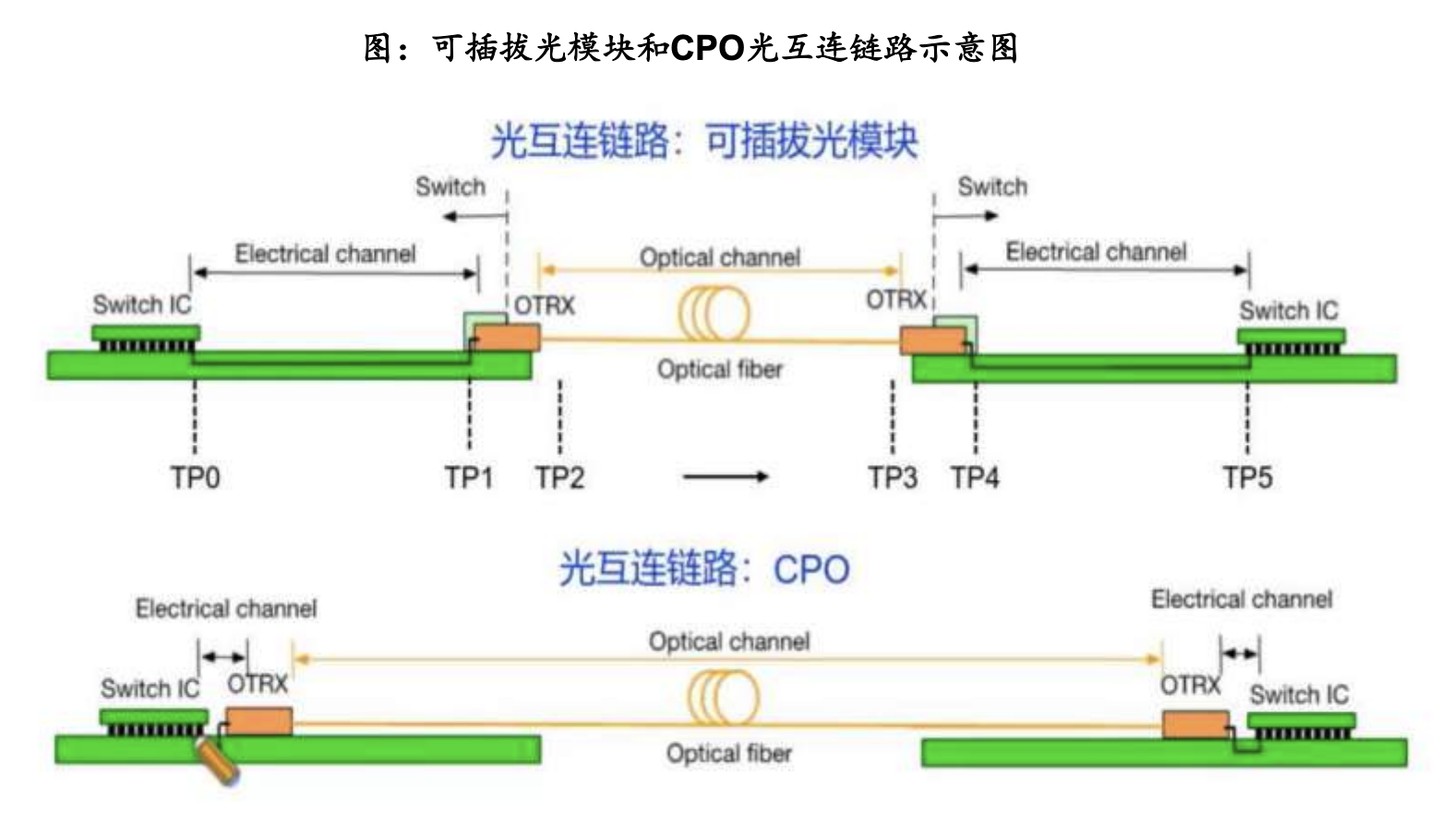

CPO (Co-packaged Optics) fundamentally alleviates the bottlenecks of traditional data center network architectures by integrating optical engines and switch ASIC chips on the same substrate.

Its core advantages are reflected in three dimensions:

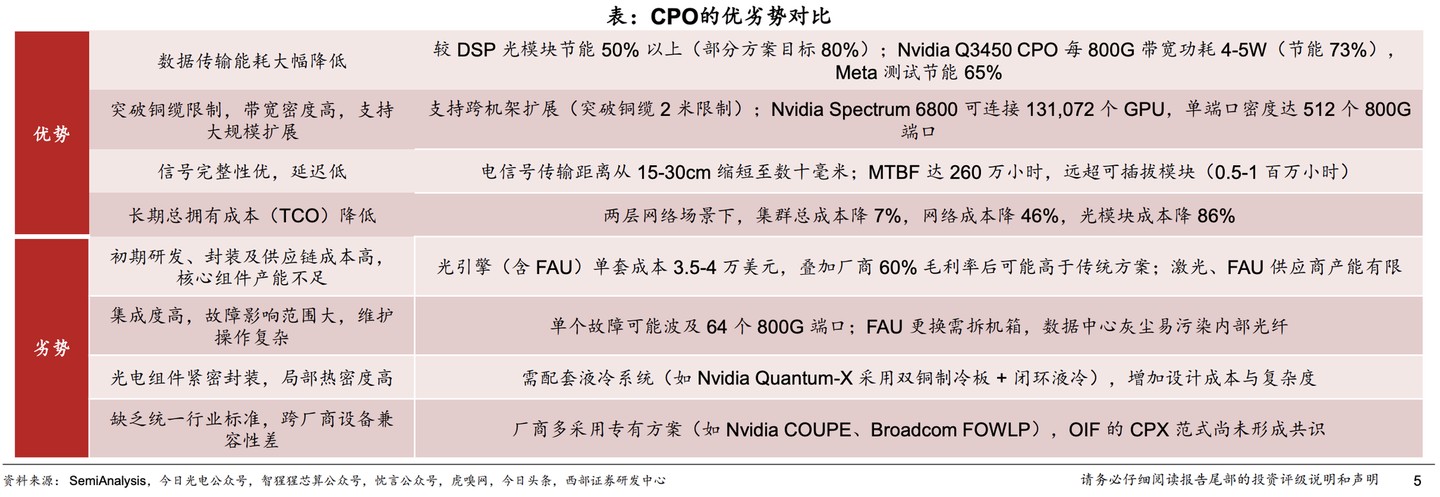

First, it significantly reduces power consumption, saving more than 50% compared to DSP optical modules; NVIDIA's Q3450 CPO consumes only 4-5W per 800G bandwidth, a saving of 73%;

Second, it breaks through copper cable limitations to support cross-rack expansion; NVIDIA Spectrum 6800 can theoretically connect 131,072 GPUs;

Third, signal integrity is significantly improved, with the electrical signal transmission distance shortened from 15-30 cm to tens of millimeters, and an MTBF (Mean Time Between Failures) of 2.6 million hours, far exceeding the 500,000-1 million hours of pluggable modules.

In the long term, in a two-layer network scenario, the CPO solution can reduce the total cluster cost by 7%, network costs by 46%, and optical module costs by 86%.

However, CPO is not without its costs. The cost of a single optical engine set is as high as $35,000-$40,000; high-density integration brings severe heat dissipation challenges, requiring supporting liquid cooling systems; due to the fixed integration of optical engines and main chips, a failure usually requires replacing the entire board, resulting in poor maintainability and flexibility.

Furthermore, the lack of unified industry standards leads to poor cross-vendor compatibility; there is currently no interoperability consensus between NVIDIA's COUPE solution and Broadcom's FOWLP solution.

Multiple Technology Routes in Parallel, Transitional Solutions with Different Emphases

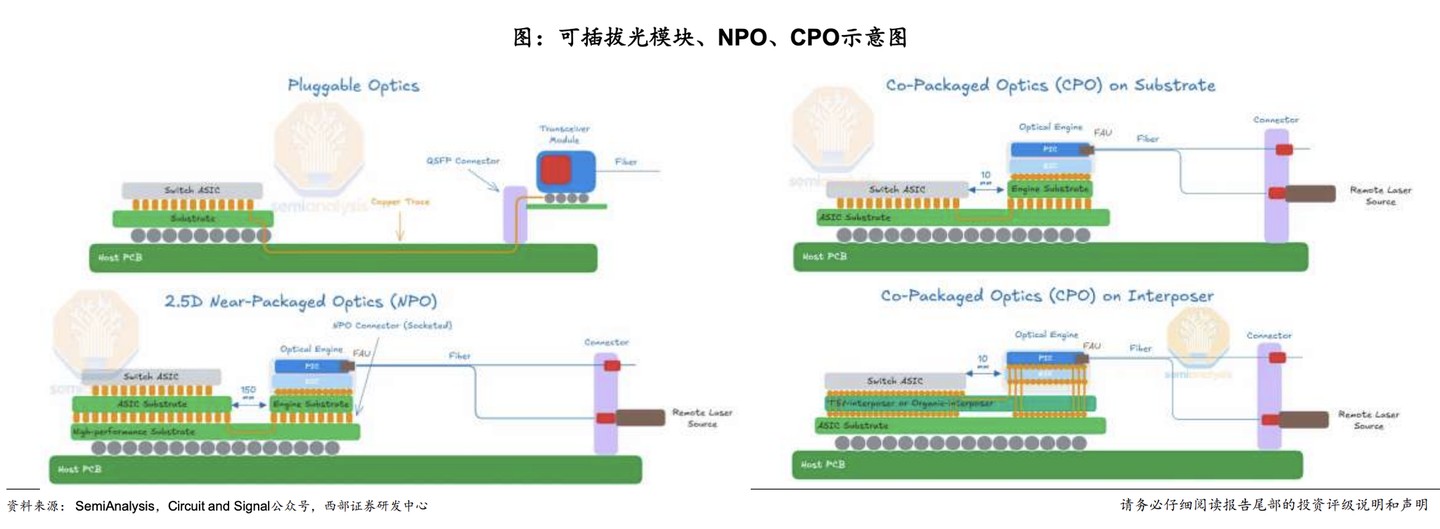

Currently, the industry is not betting solely on the CPO route but is evolving with multiple technology solutions in parallel, forming a technology spectrum from pluggable to co-packaged.

LPO (Linear Pluggable Optics) removes the DSP chip from traditional transceivers and transfers signal processing to the host-side ASIC, achieving reductions in power consumption, cost, and latency. However, its transmission distance is limited, and system compatibility poses challenges.

NPO (Near-Packaged Optics) is positioned as "built-in pluggable." Compared to CPO, it offers advantages such as pluggable optical engines, compatibility with PCB boards, no consumption of advanced packaging resources, and suitability for large-scale mass production, though it has some disadvantages in power consumption and latency. It is considered an important transitional solution for CPO.

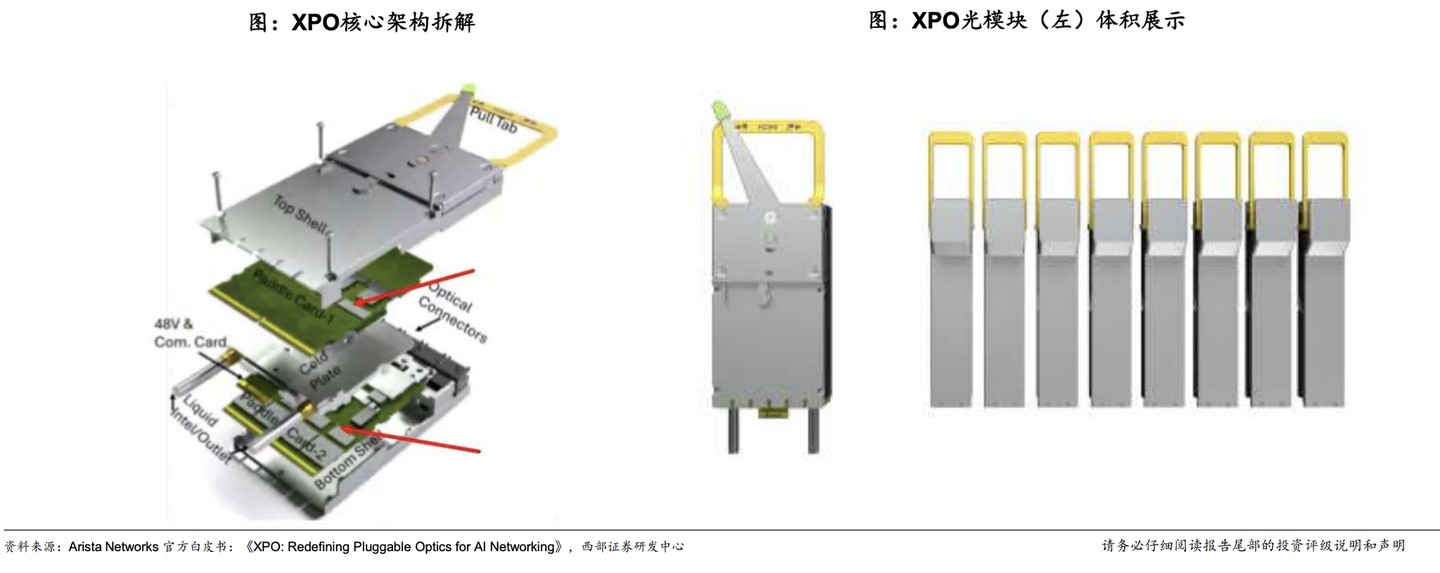

XPO (Extreme Density Pluggable Optics) represents an aggressive evolution of the pluggable route. In March 2026, Arista officially announced the establishment of the XPO MSA, aiming for a form factor of 64 channels with a single module bandwidth of 12.8Tbps, supporting a cold plate heat dissipation capacity of up to 400W per module. This achieves approximately a 4x density increase compared to 1600G-OSFP optical modules and combines high bandwidth, native liquid cooling, and pluggable operational features.

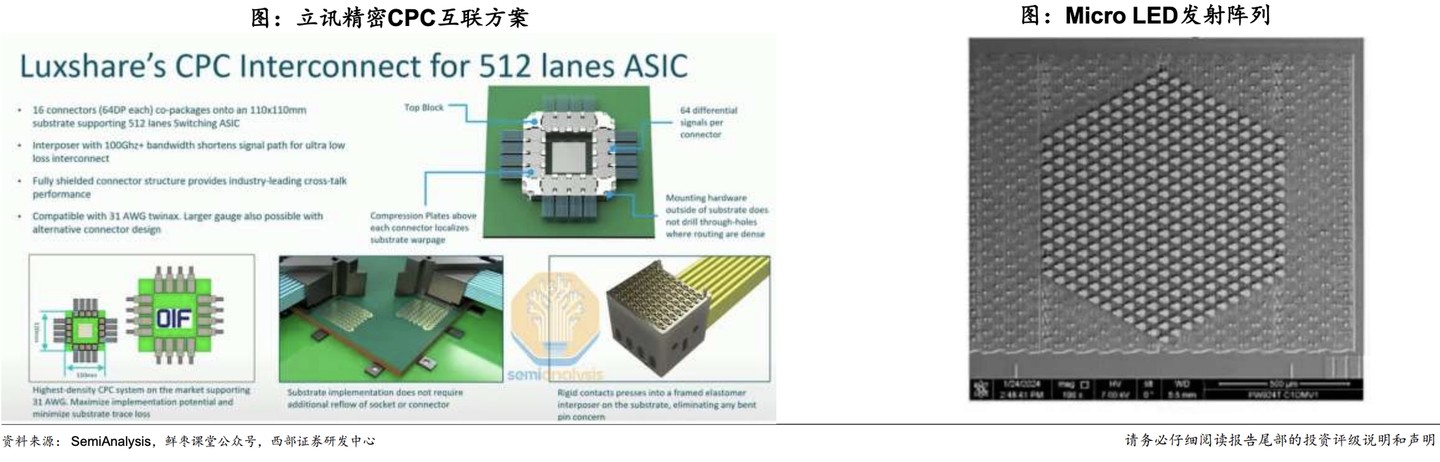

In addition, the CPC (Co-Packaged Copper) solution promoted by Luxshare Precision offers critical advantages in signal integrity by routing twin-axial copper cables directly from the packaging substrate, potentially providing a viable path for 448G SerDes deployment;

MicroLED CPO achieves higher density transmission through parallel optical emission by integrating micron-level light-emitting diode arrays with CMOS driver circuits, representing a more long-term technological exploration direction.

Considering supply chain maturity and performance advantages, the overall cost-effectiveness advantage of CPO compared to NPO and pluggable solutions is currently not obvious, and customer acceptance needs to be improved. Key variables to observe subsequently are: the iteration of switch chips and SerDes channels, and the dynamic comparison between NPO's mass production yield and the total cost of CPO.

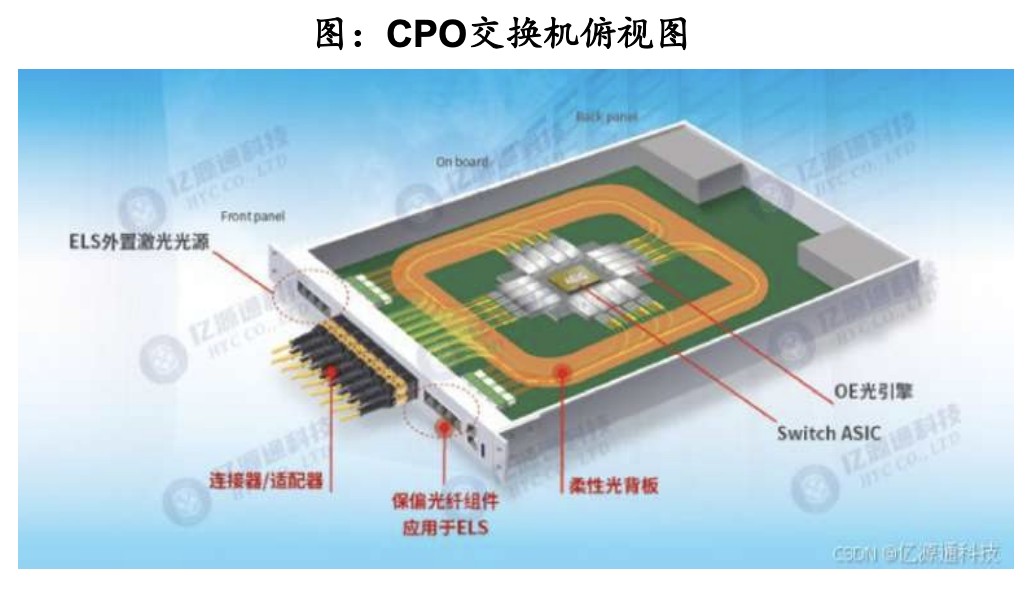

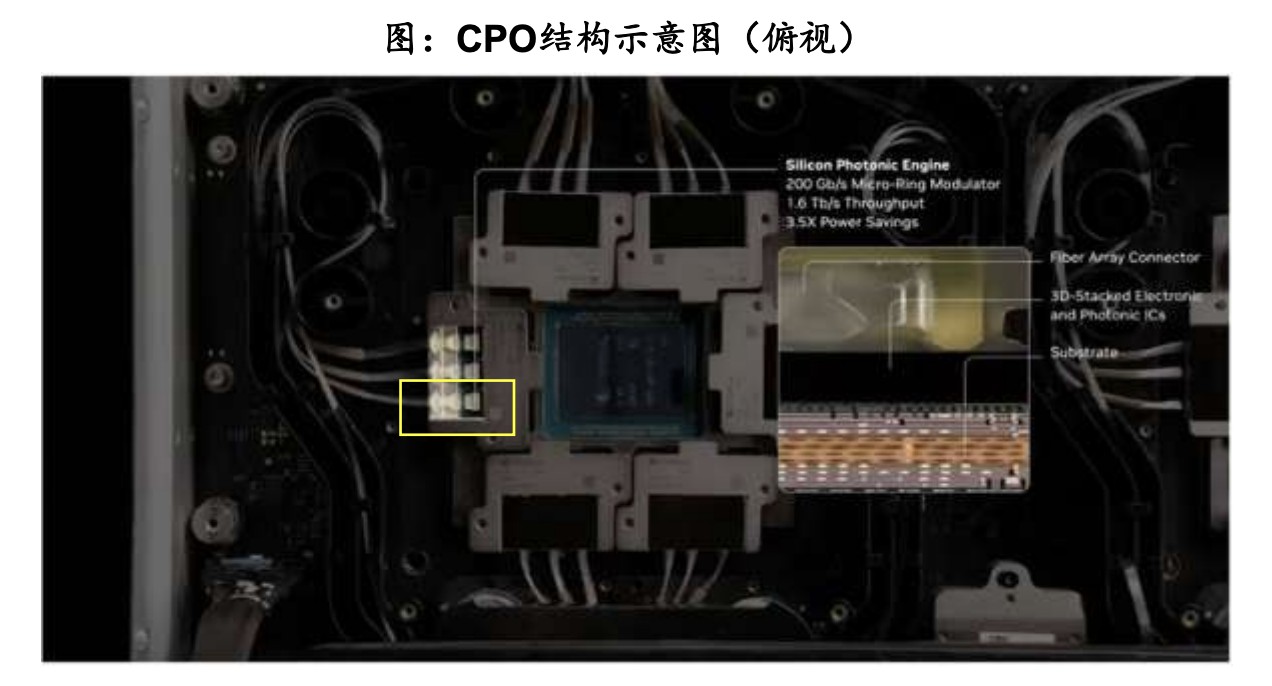

Full Disassembly of NVIDIA's CPO Switch Structural Components

Using NVIDIA's Quantum X800-Q3450 IB CPO switch as a sample, this section provides a system-level disassembly of CPO core structural components and manufacturing challenges. First, the switch configuration is as follows:

The switch is equipped with 4 Quantum-X800 ASIC chips manufactured using TSMC's 4nm process, with a single chip bandwidth of 28.8T, a total bandwidth of 115.2T, and 107 billion transistors.

The optical side is equipped with 72 1.6T optical engines, which are removable optical sub-assemblies in groups of three. Each optical engine corresponds to 8 single-channel 200Gbit/s Micro Ring Modulators (MRMs).

The laser source uses 18 ELS modules, totaling 144 continuous-wave (CW) DFB laser chips, each with an output power of approximately 300-350mW.

A total of 1,440 optical fibers are used at the transmit and receive ends, with 1,152 used for transmitting/receiving and 288 for polarization-maintaining fibers, corresponding to 144 single-mode MPO ports and 36 polarization-maintaining MPOs.

There are four core manufacturing stages:

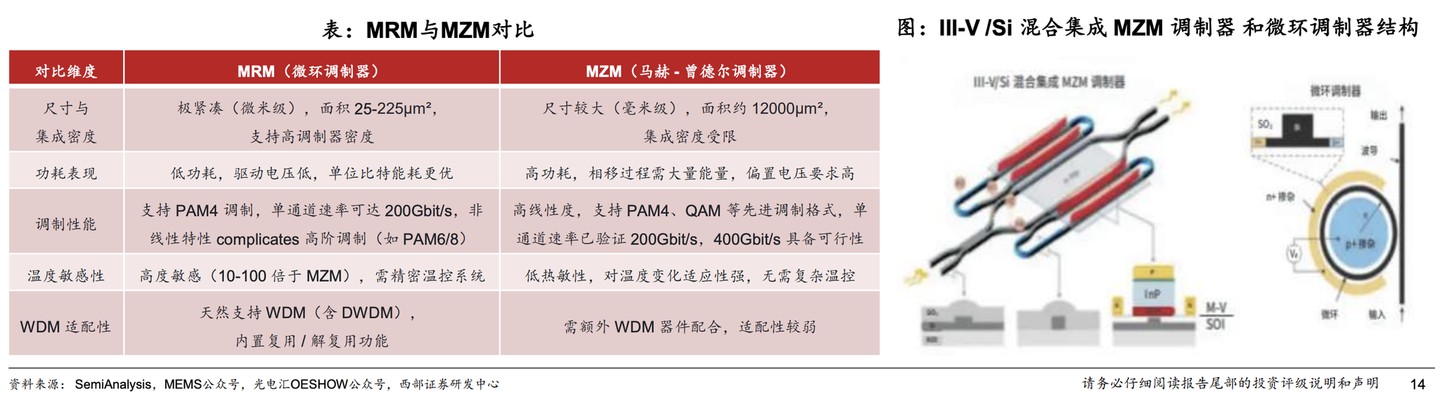

Micro Ring Modulator (MRM): Compared to Mach-Zehnder Modulators (MZMs), MRMs are extremely compact (area 25-225μm²), have low power consumption, and naturally support WDM. However, they are highly temperature-sensitive (about 10-100 times more than MZMs), requiring a precise temperature control system. Their non-linear characteristics also pose challenges for higher-order modulation.

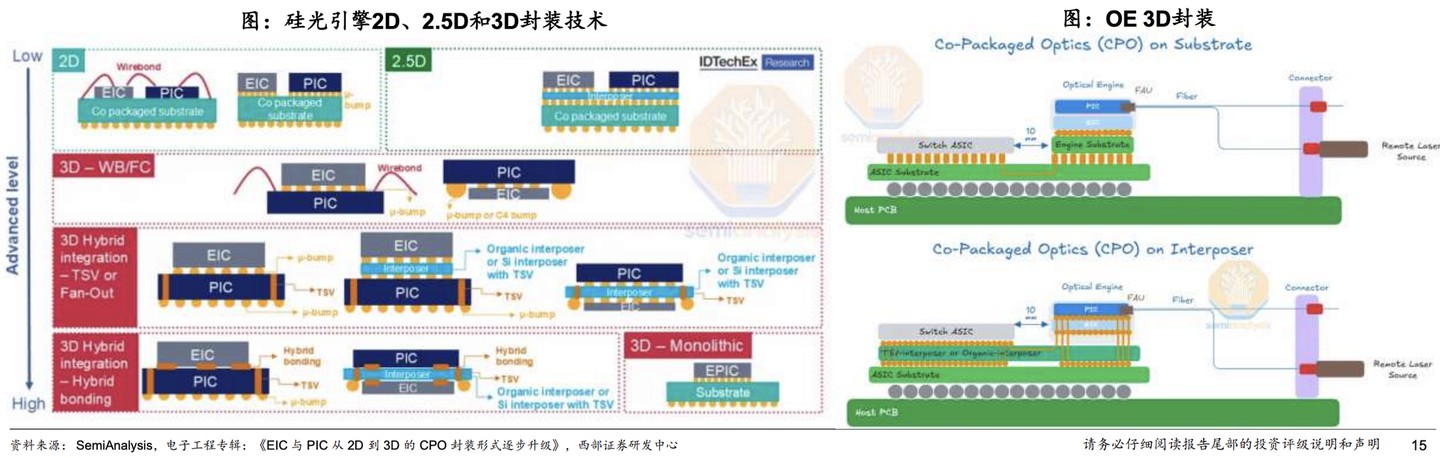

PIC and EIC Packaging: Evolving from 2D and 2.5D to 3D packaging. 3D packaging uses vertical interconnects to achieve shorter transmission distances and higher integration. However, process complexity and yield pressure increase significantly, making it a hot topic and challenge in current CPO technology research.

OE and ASIC Chip Packaging: Taking NVIDIA's Spectrum-X Photonics switch chip packaging as an example, its substrate size reaches 110mm×110mm, far exceeding the 70mm×76mm of the Blackwell architecture. During the packaging process, 36 known-good optical engines must first be fixed to the substrate via flip-chip bonding, followed by interposer module bonding. Yield control is extremely difficult, and as the interposer size increases, warpage issues become more prominent.

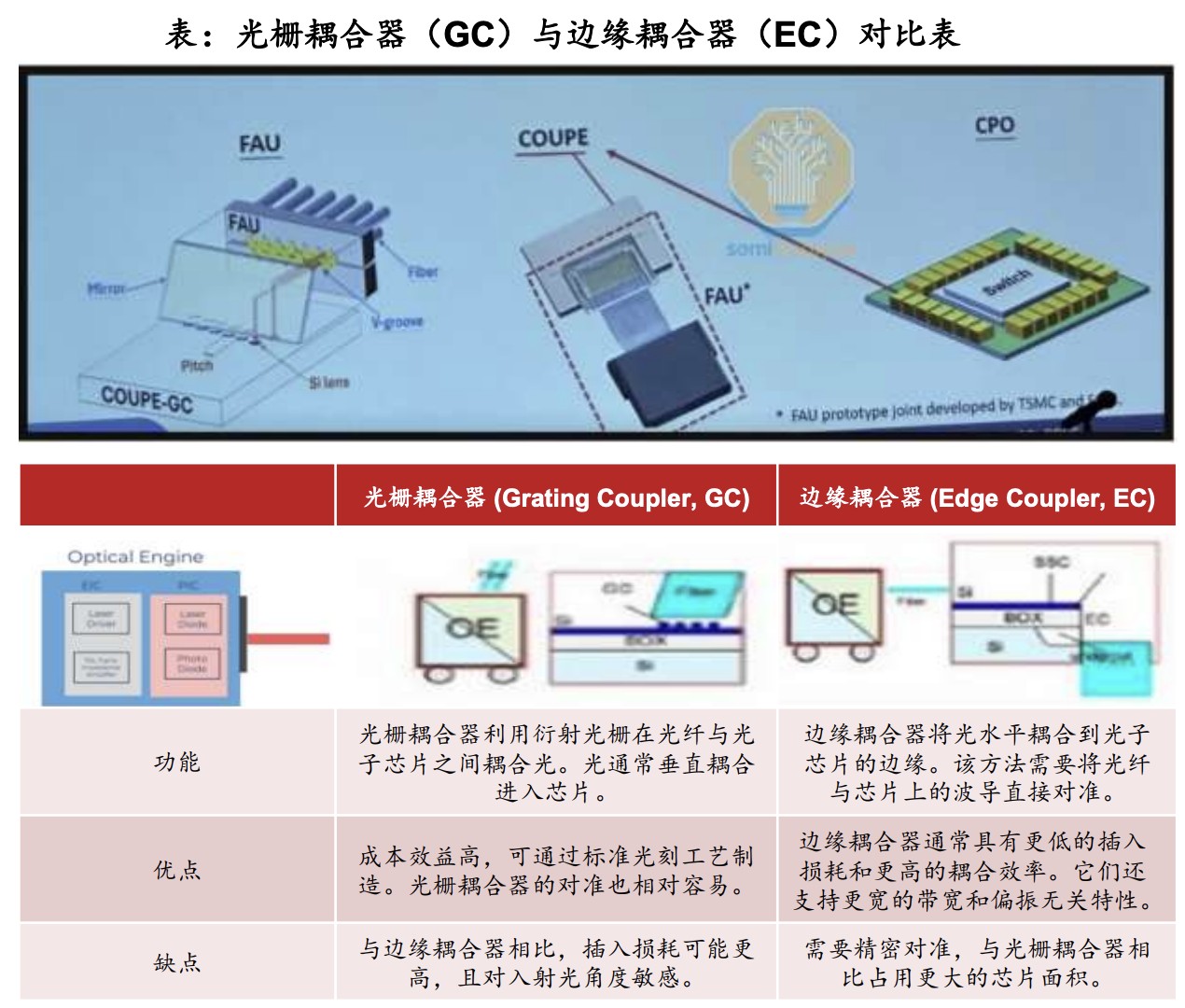

Optical Fiber Coupling: CPO systems require optical fibers to align with waveguides on the chip with sub-micron precision, and this must be performed within the heat-generating environment of the switch chassis, making it much more difficult than in pluggable module scenarios. Edge coupling is the current mainstream solution, relying on microlenses for focusing and waveguide tapers for efficient coupling.

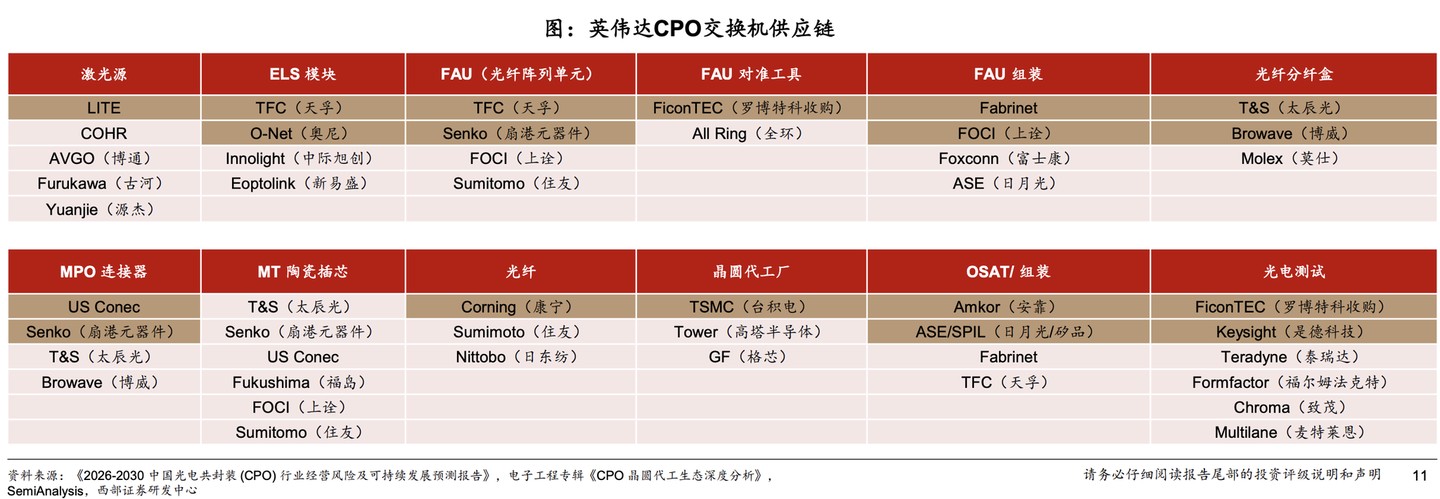

Highly Fragmented Supply Chain, Focus on Core Segments with Clear Divisions of Labor

The current fragmentation of the CPO supply chain is one of the core obstacles hindering its commercialization acceleration.

From the supply chain map of NVIDIA's CPO switches, laser sources, ELS modules, FAUs, MPO connectors, wafer foundries, OSAT packaging, and optical-electrical testing all involve multiple suppliers. However, foundries with complete optoelectronic integration capabilities, specialized high-precision optical-electrical testing equipment suppliers, and standardized packaging material suppliers are still quite scarce.

On the Scale-up side, the supply-side constraints faced by CPO are more prominent. Since NVLink and other vertical expansion networks belong to proprietary closed systems, leading manufacturers have vertical integration capabilities to drive CPO implementation. The urgency for commercialization is higher, but yield and capacity bottlenecks on the supply side are equally critical.

On the Scale-out side, the improvement in power consumption and cost provided by CPO is relatively limited (total power consumption optimized by only 2% and total cost optimized by only 3% in a three-layer network architecture), and the pace of commercialization is relatively steady.

Investors are advised to prioritize two directions:

First, segments with clear divisions of labor that have already participated in joint R&D with CPO switch manufacturers or have order expectations, including high-power CW light sources, FAUs, and ELS modules;

Second, segments with elastic incremental potential compared to pluggable optical modules, including CPO coupling/testing equipment, polarization-maintaining fibers, advanced packaging (PIC and EIC packaging), ASIC chip and OE packaging, and fiber distribution boxes.