Taiwan Semiconductor Q1 Net Profit Surges 58% Year-Over-Year, Gross Margin Historically Breaks 66%, CapEx Hits $11.1 Billion | Earnings Insights

More news coming soon

Taiwan Semiconductor's first-quarter 2026 results comprehensively exceeded market expectations, with net profit, gross margin, and operating margin all significantly surpassing analyst forecasts, marking a substantial strengthening of profitability.

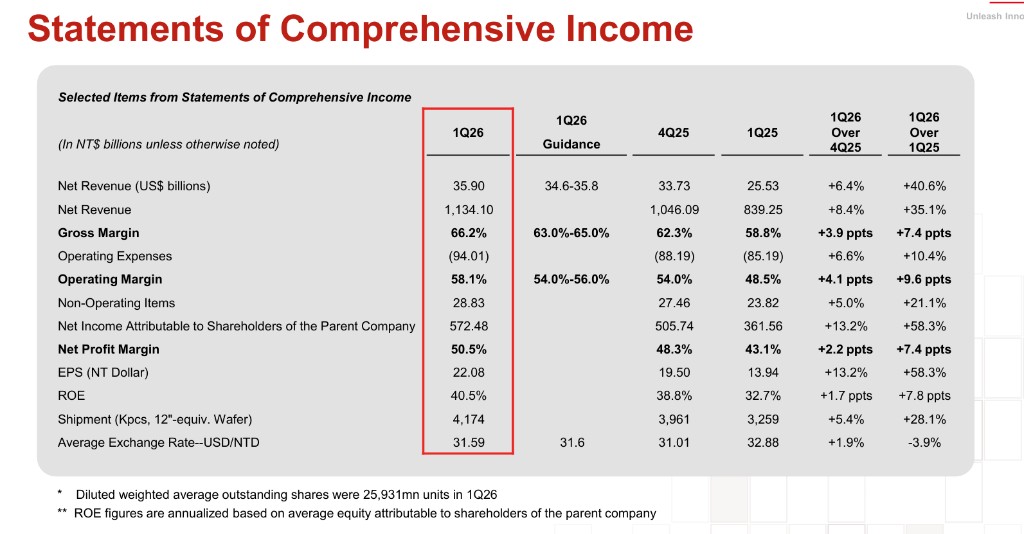

On the 16th, Taiwan Semiconductor released its Q1 2026 earnings report: net profit reached NT$572.5 billion, a 58% year-over-year increase, approximately 6% higher than the estimated NT$542.4 billion; revenue stood at NT$1.134 trillion, up 35% year-over-year, exceeding the estimated NT$1.12 trillion; operating profit was NT$659.0 billion, also surpassing the estimated NT$623.8 billion.

Gross margin was the standout highlight of the quarter. Taiwan Semiconductor's gross margin rose to 66.2%, expanding nearly 4 percentage points from the previous quarter's 62.3%, far exceeding the market estimate of 64.5%; operating profit margin also climbed to 58.1%, above the estimated 55.6% and the previous quarter's 54.0%, reflecting continued improvement in the profit structure. The company announced that capital expenditure for the first quarter amounted to $11.1 billion.

This performance is expected to ease market concerns over whether the deteriorating situation in the Middle East would dampen demand for AI data centers and smart devices like iPhones. Previously, the Middle East conflict had already pressured global shipping routes and energy prices, prompting investors to closely monitor signs to assess whether such impacts could spill over into tech giants' capital expenditure plans. Following the earnings release, Taiwan Semiconductor's US after-hours stock price rose nearly 2%.

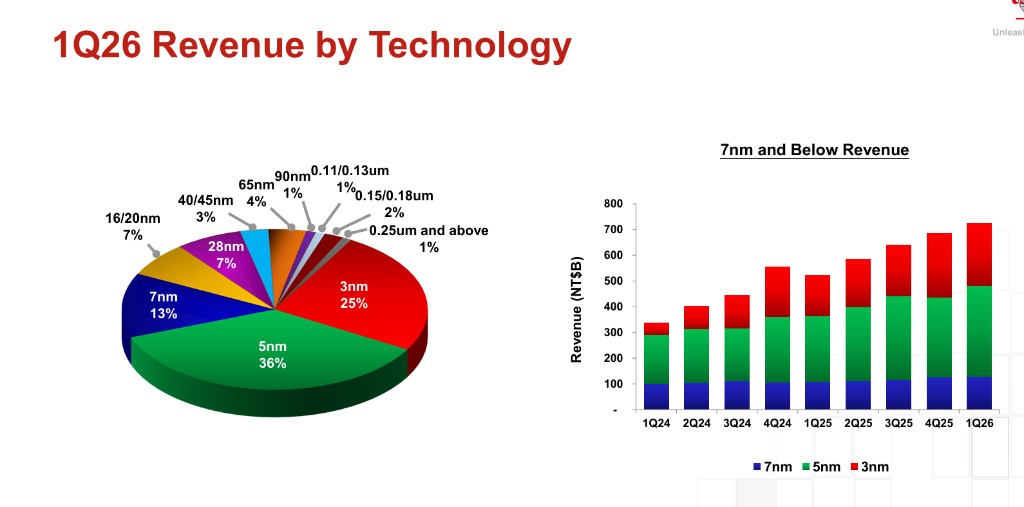

Advanced Process Nodes Contribute Over Half of Revenue; 3nm Demand Remains Robust

From the perspective of process technology, advanced nodes remain the core engine driving Taiwan Semiconductor's revenue. The 5nm process accounted for the highest share at 36%; the 3nm process followed closely at 25%. Together, processes at 5nm and below contributed over 60% of revenue, showing an accelerating growth trend—quarterly absolute revenue from 7nm and below processes nearly doubled from Q1 2024 to Q1 2026.

The 7nm process accounted for 13% this quarter, while 16/20nm and 28nm processes each accounted for 7%. Mature processes (0.15/0.18 microns) made up 4%, with other nodes collectively accounting for approximately 14%. Overall, the migration toward 3nm and below continues to outpace market expectations, aligning closely with the urgent global demand for extreme computing power driven by artificial intelligence (AI) chips.

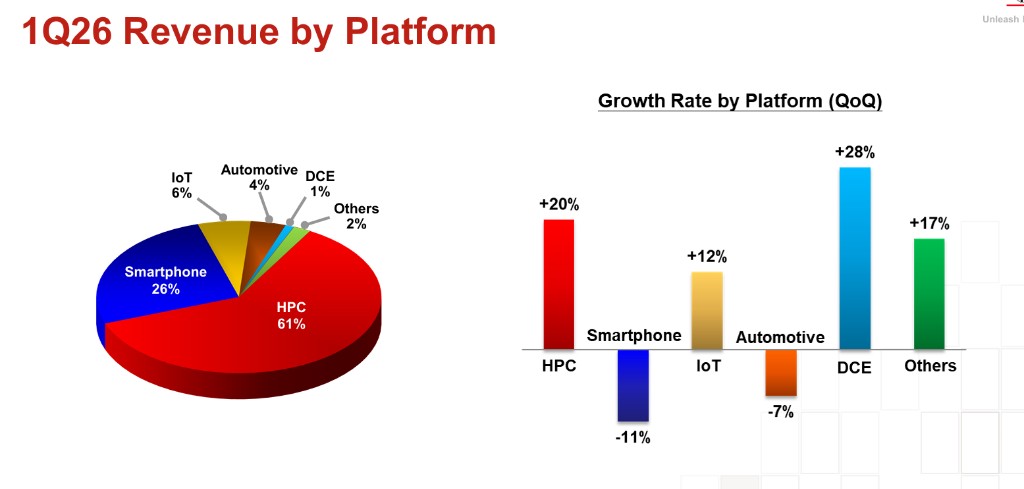

HPC Platform Stands Alone, Contributing Over 60% of Revenue

Breaking down revenue by end-application platform, the High-Performance Computing (HPC) platform accounted for a dominant 61% of revenue this quarter, solidifying its position as Taiwan Semiconductor's largest revenue source. This reflects a clear trend of increasing concentration in recent years, mirroring the industry reality of sustained large-scale wafer starts by global cloud providers and AI accelerator chipmakers (GPU/TPU/ASIC).

The smartphone platform ranked second with a 26% share, maintaining relative stability driven by flagship model inventory cycles. The IoT platform accounted for 6%, the automotive electronics platform for 4%, and DCE plus others combined for just 3%. Together, HPC and Smartphone platforms contributed approximately 87% of revenue. This highly concentrated structure indicates that Taiwan Semiconductor's revenue growth is deeply tied to the global AI investment wave.

Profitability Reaches New Heights as Scale Effects and Product Mix Converge

Gross margin expanded dramatically from 58.8% in Q1 2025 to 66.2%, a cumulative improvement of 7.4 percentage points. This was driven by multiple factors: continuous improvement in advanced process yields, full capacity utilization spreading fixed costs, premium pricing effects from advanced product mixes, and favorable short-term movements in the New Taiwan Dollar versus the US Dollar exchange rate (average rate of 31.59 this quarter versus 32.88 a year ago, an appreciation of approximately 3.9%).

Operating expenses totaled NT$94.01 billion, up 6.6% sequentially, but benefiting from high revenue growth, the operating expense ratio continued to decline, pushing operating profit margin to a record high of 58.1%. Notably, non-operating income contributed NT$28.83 billion this quarter, up 21.1% year-over-year, providing additional support to net profit.

Strong Cash Flow Further Strengthens Balance Sheet

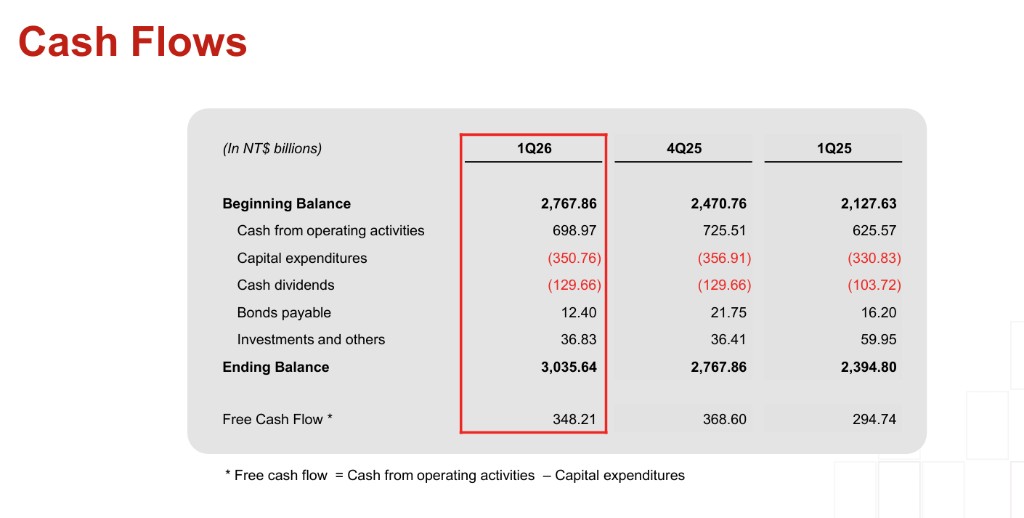

Regarding the balance sheet, as of the end of March 2026, Taiwan Semiconductor's cash and securities balance reached NT$338.36 billion, representing 39.0% of total assets, up from the previous quarter. Total assets expanded to NT$866.095 billion, more than 21% higher than a year ago; shareholders' equity increased to NT$593.239 billion, while the debt-to-asset ratio fell to 31.5%, indicating continued optimization of the financial structure.

In terms of cash flow, operating cash inflow for the quarter was NT$69.897 billion, capital expenditure was NT$35.076 billion, resulting in free cash flow of NT$34.821 billion, up 18.1% year-over-year. Cash dividends paid amounted to NT$12.966 billion, with an ending cash balance (excluding securities) of NT$303.564 billion. The board has approved a cash dividend of NT$6.00 per share for Q4 2025, scheduled for distribution on July 9, 2026, continuing to return value to shareholders.

More news coming soon……