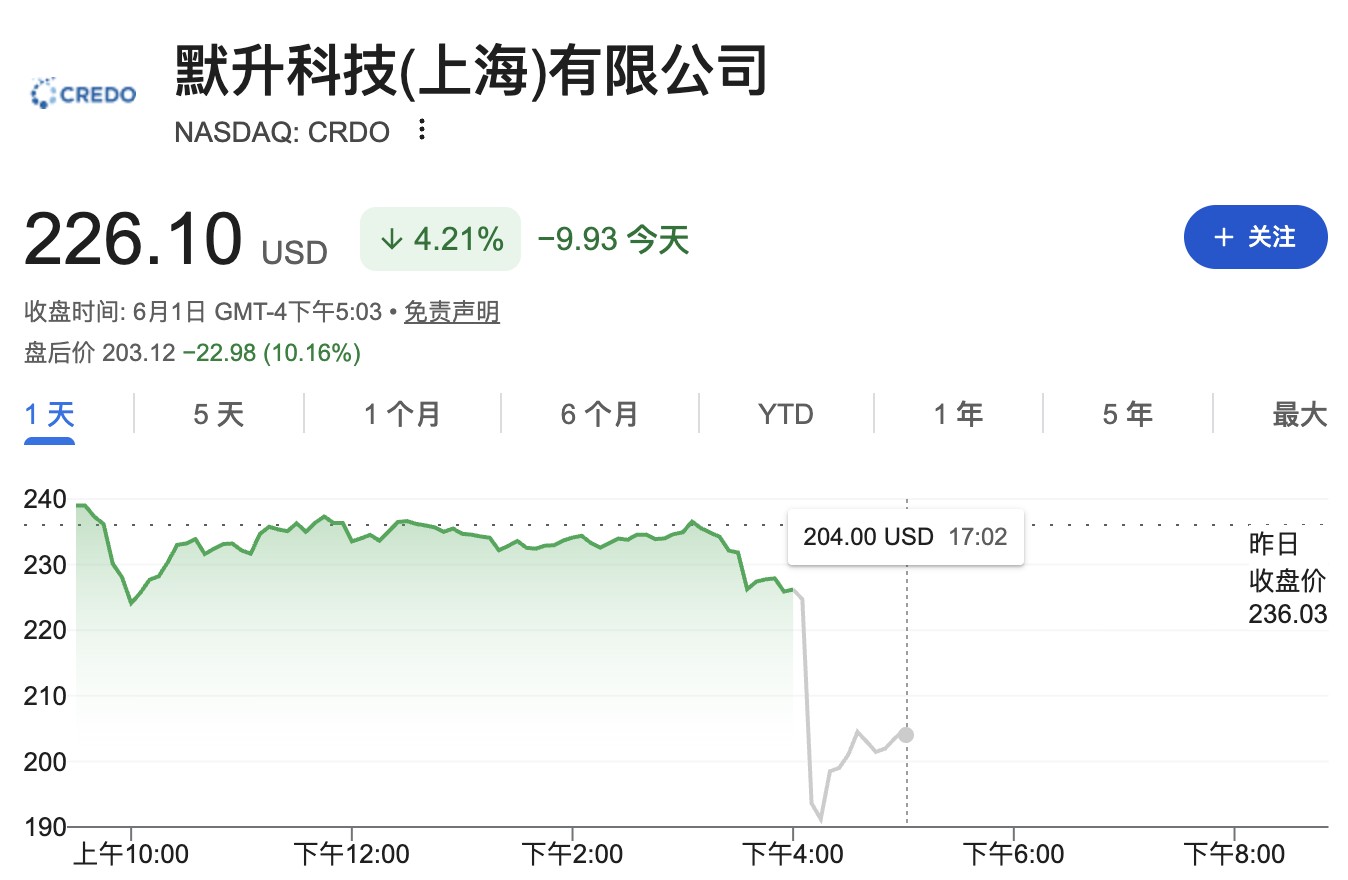

Optical Interconnect Giant Credo Beats Q4 Revenue, Profit, and Next-Quarter Guidance Expectations, Yet Stock Plunges Nearly 19% in After-Hours Trading

Credo released its fiscal 2026 Q4 results, with revenue of $437 million and non-GAAP diluted earnings per share of $1.16 both exceeding expectations. Full-year revenue more than tripled, and Q5 guidance surpassed analyst estimates. Despite strong fundamentals and benefits from AI demand, its stock plunged nearly 19% in after-hours trading, influenced by market sentiment or other factors

Credo Technology Group announced its fiscal 2026 fourth-quarter and full-year results for the period ended May 2, 2026. Both revenue and earnings surged significantly, with full-year revenue increasing more than threefold compared to the previous fiscal year, reflecting sustained strong demand for high-speed connectivity solutions driven by AI data center infrastructure construction.

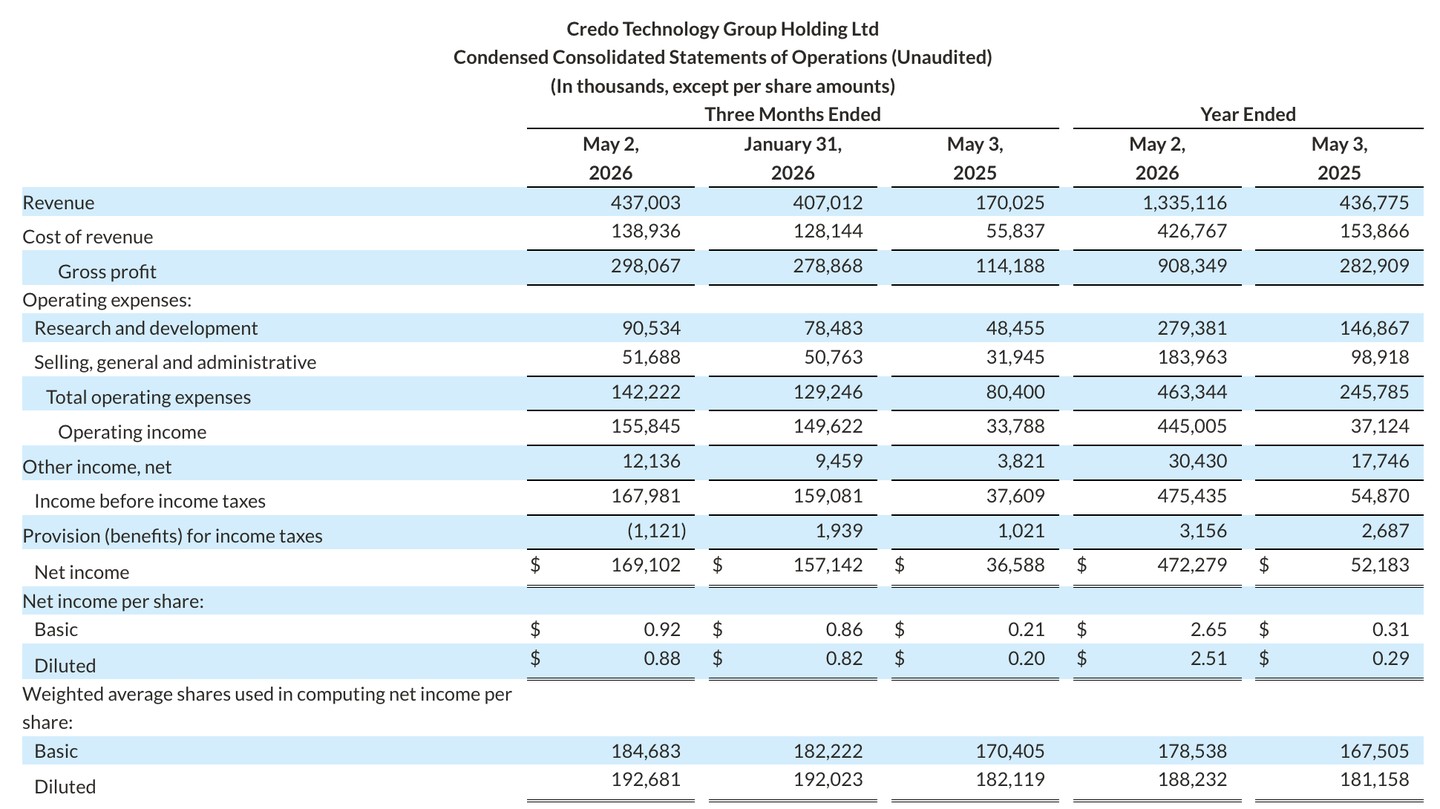

Fourth-quarter revenue reached $437 million, a year-over-year increase of 157% and a quarter-over-quarter increase of 7.4%, beating the analyst consensus estimate of $432.5 million. Non-GAAP diluted earnings per share (EPS) came in at $1.16, surpassing the expected $1.00.

The company also issued guidance for the first quarter of fiscal 2027, projecting revenue between $465 million and $475 million. The midpoint of this range represents an approximate 7.6% increase from the previous quarter and exceeds the analyst consensus estimate of $460.5 million.

CEO Bill Brennan stated that fiscal 2026 was another pivotal year for the company, with full-year revenue exceeding $1.3 billion and non-GAAP net income growing more than fivefold to $662 million. Entering fiscal 2027 with vertically integrated innovations, the company will continue to help customers accelerate cluster stabilization time, improve GPU utilization, enhance network reliability, and reduce overall infrastructure power consumption and operating costs.

Strong performance and positive forward guidance indicate that Credo continues to benefit from the rapid expansion of AI infrastructure, with no signs of slowing demand for the scaled deployment of its high-speed copper cable and optical interconnect products. Nevertheless, Credo's stock price plummeted by nearly 19% in after-hours trading.

Quarterly Revenue Hits New Record, Margins Remain High

Fourth-quarter revenue reached $437 million, up 157% year-over-year from $170 million in the same period last year, and up 7.4% from $407 million in the previous quarter, continuing a trajectory of accelerating sequential growth.

In terms of profitability, GAAP gross margin was 68.2%, and non-GAAP gross margin was 68.3%, slightly down from 68.5% (non-GAAP) in the previous quarter but remaining at a high level overall. GAAP net income was $169.1 million, and non-GAAP net income was $226.7 million, resulting in a non-GAAP net profit margin of 51.9%. GAAP diluted EPS was $0.88, while non-GAAP diluted EPS was $1.16, an increase from $1.07 in the previous quarter.

GAAP operating expenses for the fourth quarter were $142.2 million, up from $129.3 million in the previous quarter, primarily driven by one-time items including $9.3 million in acquisition and integration-related costs and $0.4 million in amortization of acquired intangible assets.

Cash and short-term investments at the end of the period totaled approximately $1.4 billion, a significant increase from approximately $431 million at the end of the previous fiscal year, indicating a robust financial position.

Full-Year Performance: Revenue Triples, Significant Profit Leverage Effect

For the full fiscal year 2026, Credo's revenue reached $1.3351 billion, an increase of approximately 206% from $436.8 million in the previous fiscal year, achieving nearly threefold growth.

Profit expansion was even more pronounced. Full-year GAAP net income jumped from $52.2 million in the previous fiscal year to $472.3 million; non-GAAP net income increased from $129.9 million to $661.5 million, a rise of over 400%. The full-year non-GAAP net profit margin increased substantially from 29.7% to 49.5%, demonstrating the significant leverage effect brought about by the rapid expansion in revenue scale.

From a balance sheet perspective, total assets reached $2.2956 billion as of May 2, 2026, a substantial increase from $809.3 million at the end of the previous fiscal year. Cash and cash equivalents rose from $236.3 million to $1.165 billion.

The balance sheet recorded new goodwill of $92.8 million and net intangible assets of $29.3 million, whereas both items were zero at the end of the previous fiscal year, reflecting the completion of an acquisition transaction by the company at the end of this fiscal year.

Fiscal 2027 Q1 Guidance: Growth Momentum Expected to Continue

The company expects revenue for the first quarter of fiscal 2027 (ending August 1, 2026) to be between $465 million and $475 million. Based on the midpoint of $470 million, this represents an approximate 7.6% increase from the fourth quarter's $437 million.

Regarding gross margins, GAAP gross margin is expected to be between 66.9% and 68.9%, and non-GAAP gross margin is expected to be between 67.0% and 69.0%. This range covers the actual levels of the fourth quarter, indicating management's confidence in margin stability.

In terms of operating expenses, GAAP operating expenses are projected to be between $167.6 million and $171.6 million, further rising from $142.2 million in the fourth quarter, partly reflecting the ongoing impact of acquisition integration costs. Non-GAAP operating expenses are expected to be between $86 million and $90 million, a slight increase from $81.7 million in the fourth quarter, indicating that the company continues to increase R&D and operational investments to support scale expansion.

Risk Disclosure and Disclaimer

Market involves risks; investment requires caution. This article does not constitute personal investment advice, nor does it take into account the specific investment objectives, financial status, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances. Investment decisions made based on this content are at the user's own risk.