Food Delivery War Cools Down, Meituan Back on Track: Losses Narrow Sharply Beyond Expectations, AOV and Market Share Rebound

Meituan's Q1 performance exceeded expectations, with net losses narrowing significantly to RMB 4.97 billion. The price war in food delivery has cooled, leading to significant improvements in the efficiency of instant delivery services, while average order value (AOV) and market share have both rebounded. Morgan Stanley and UBS have reiterated their bullish stance, believing the company's strategy has shifted from "burning cash" to profit expansion. They expect the food delivery business to reach break-even in Q2, marking the full onset of normalized profitability

Meituan's Q1 performance thoroughly defeated Wall Street's pessimistic expectations, serving as a crucial signal that the company is emerging from the quagmire of price wars and moving towards normalized profitability.

As noted in a Wallstreetcn article, on June 1, Meituan released its latest financial report, showing Q1 2026 revenue of RMB 91 billion and an adjusted net loss of RMB 4.97 billion, compared to a loss of RMB 15.1 billion in Q4 2025. Affected by intensifying competition, the Core Local Commerce segment turned from profit to loss, with marketing expenses surging 51.1% to RMB 23 billion. New Business revenue increased by 21.3%, with losses narrowing.

On June 2, according to Zhuifeng Trading Desk, Morgan Stanley and UBS pointed out in their latest research reports that core financial data sent a clear signal: the brutal food delivery price war is cooling down, and the company's profitability is returning to normal faster than expected.

Meanwhile, Meituan's overall losses narrowed significantly in Q1. The unit economics (UE) of the instant delivery business improved markedly, while the food delivery average order value (AOV) and market share both stabilized. This indicates that Meituan is pulling itself out of the "burning cash for growth" trap, with its core logic shifting from concerns over cash burn to margin expansion and efficiency improvements in new businesses.

Based on this strong performance, both Morgan Stanley and UBS reiterated their bullish stance: Morgan Stanley maintained its "Overweight" rating and HKD 120 target price, while UBS maintained its "Buy" rating and HKD 128 target price. Both investment banks agreed that Meituan's food delivery business is expected to reach break-even in Q2, fully opening the path to normalized profitability.

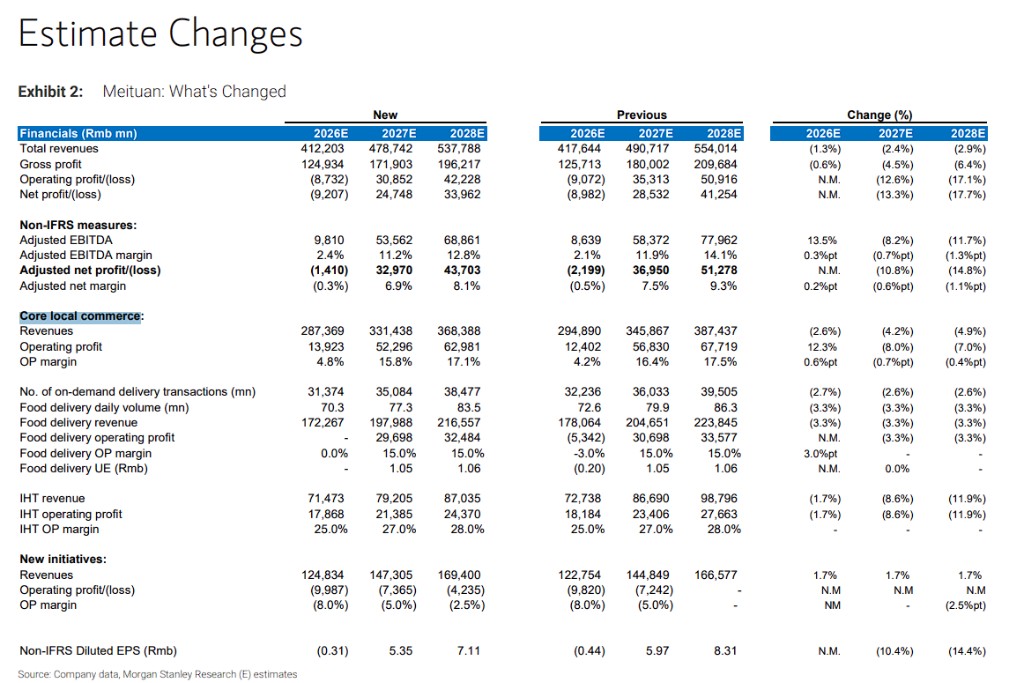

Morgan Stanley: Loss Narrowing Faster Than Expected, Raises CLC Profit Forecast, Maintains HKD 120 Target Price

In its latest research report, Morgan Stanley maintained Meituan's rating at Overweight and its target price at HKD 120 (implying an 18x expected P/E ratio for 2027). It raised its operating profit forecast for the Core Local Commerce (CLC) segment for 2026 by 12% to reflect that the narrowing of food delivery UE losses was faster than anticipated.

- Core Drivers of Q1 Performance Beat

Morgan Stanley pointed out that the biggest positive surprise in Q1 came from the narrowing losses in the instant delivery business. CLC operating loss was RMB 2.03 billion, significantly better than Morgan Stanley's estimate of a RMB 4.268 billion loss and the market consensus expectation of a RMB 4.376 billion loss, beating estimates by 33.3%. The overall CLC operating margin was -3.2%, an improvement of 24 percentage points year-over-year.

- Food Delivery UE: Potential to Reach Break-Even in Q2

Morgan Stanley expects CLC operating profit to turn positive to approximately RMB 3 billion in Q2 (including membership investments). The overall loss in the instant delivery business is expected to narrow further to about RMB 437 million (with food delivery generating a profit of about RMB 313 million, while Shangou/instant retail incurs a loss of about RMB 750 million).

Management revealed that food delivery UE achieved profitability in April and May, with June's trend depending on the intensity of the 618 promotional activities. Morgan Stanley believes that Meituan's UE advantage in food delivery over Alibaba expanded further to approximately RMB 3 per order in Q1 (up from RMB 2 in Q4), indicating that the competitive landscape has basically stabilized. Meituan's market share in orders with an AOV above RMB 30 remained at 70%, with an estimated comprehensive GTV share of around 60%.

- In-Store, Hotel & Travel (IHT): Competitive Pressure Persists, Margins Basically Stable

Morgan Stanley expects IHT GTV and revenue growth in Q2 to be similar to Q1, at approximately 11% and 9% respectively, with operating profit around RMB 4.3 billion and operating margin stable quarter-on-quarter at 25%. On the regulatory front, stronger policy support is expected to help Meituan further increase its market share in high-star hotels, but the in-store dining business still faces competitive pressure from Douyin's continued increase in subsidies. Morgan Stanley expects margins to remain basically stable in the second half of the year but will continue to monitor changes in the competitive landscape.

- New Businesses: Losses Slightly Expand, Keeta Internationalization Focuses on Profitability

Morgan Stanley expects the operating loss of New Businesses to expand slightly to about RMB 2.4 billion in Q2 (from RMB 2.1 billion in Q1), mainly driven by the expansion of Xiaoxiang Supermarket (now present in 55 cities) and continued investment in Keeta. The Hong Kong business has achieved sustained profitability, and UE improvement in Saudi Arabia has accelerated significantly, with break-even expected at some point in 2026 and full profitability in fiscal year 2027. Morgan Stanley noted that Meituan will continue to prioritize profitability improvements in Keeta's international business over market expansion.

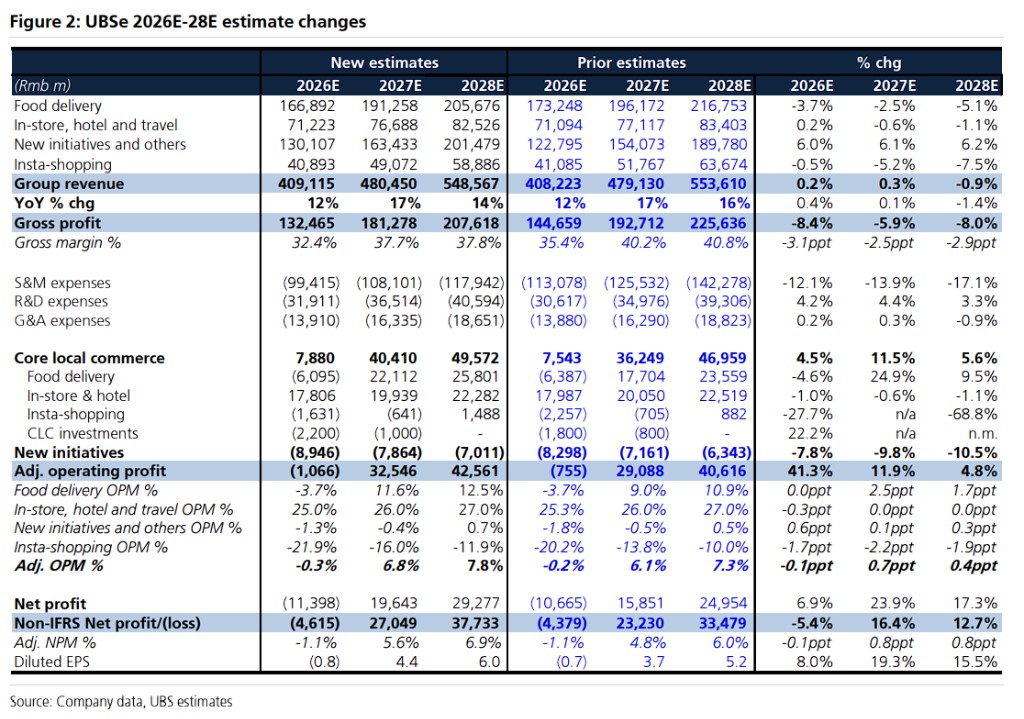

UBS: Clear Path to Normalized Profitability, Raises 2027-2028 Earnings Forecast, Target Price HKD 128

In its latest research report, UBS maintained Meituan's Buy rating and target price of HKD 128 (based on Sum-of-the-Parts valuation). Following the Q1 earnings release, it fine-tuned its 2026 forecasts and raised its earnings per share (EPS) forecasts for 2027-2028 by 15%-19%.

- Q1 Performance: Adjusted Operating Loss Significantly Better Than Expected

UBS pointed out that total revenue in Q1 increased by 5.6% year-over-year to RMB 91.039 billion, in line with expectations. The adjusted operating loss was RMB 4.146 billion, significantly better than the market consensus expectation of a RMB 7.047 billion loss, primarily due to significant improvements in the UE of instant retail (Shangou). The non-IFRS net loss was RMB 4.968 billion, better than the market consensus expectation of a RMB 6.719 billion loss, beating estimates by 26.1%.

- Food Delivery: AOV Rebounds, Share Stabilizes, UE Recovery Accelerates

UBS holds a positive view on the food delivery business. Food delivery order volume growth in Q1 was approximately +8% year-over-year. Revenue decreased by 7% year-over-year, an improvement from the -10% decline in Q4, mainly due to reduced subsidies.

Regarding competition, management stated that Meituan's market share relative to Alibaba in terms of order volume and GTV continues to improve, with food delivery order volume/GTV shares remaining above 55%/60%, and the share of orders with an AOV above RMB 30 staying at 70%.

UBS specifically noted that AOV has shown a more pronounced rebound since March, attributed to Meituan's stronger user stickiness and reduced user sensitivity to subsidies, thereby driving improved profitability in April and May. However, this may dip in June due to 618 promotional activities.

UBS expects the food delivery business to approach break-even in Q2 (compared to a loss of about RMB 0.9 per order in Q1), benefiting from favorable seasonal factors; however, UE may decline slightly in the second half of the year due to increased seasonal rider subsidies. UBS forecasts the full-year 2026 food delivery UE to be a loss of RMB 0.3 per order. Furthermore, if regulatory constraints on competition lead to further reduction in subsidies, there will be upside potential for UE.

- In-Store Business: Competitive Landscape Differentiating, Margins Remain Stable

UBS holds a neutral view on the in-store business. In-store GTV growth in Q1 was approximately +12% year-over-year, and revenue growth was about +8% (Q4 was +10%), with operating margin basically stable quarter-on-quarter at around 25%. The weak macro environment and the impact of Douyin's increased subsidies were partly offset by Meituan's reduction in subsidies for non-core categories. UBS believes that the differentiated competitive strategies between Meituan and Douyin in various categories are becoming increasingly apparent, with both sides focusing more on profitability rather than the previous intense competition. Looking ahead to Q2, UBS expects GTV/revenue growth to remain at +12%/+8%, with margins stable at 25%.

- CLC Overall: Operating Profit Expected to Turn Positive in Q2

UBS expects CLC revenue growth to accelerate to about +5% in Q2 (from +0.1% in Q1), with operating profit turning from a loss of RMB 2.03 billion in Q1 to a positive figure of approximately RMB 3.2 billion. This forecast includes about RMB 800 million in brand advertising and membership benefit investments (RMB 500 million in Q1) aimed at retaining core users.

- New Businesses: Keeta Efficiency Improves, Losses Narrow

UBS pointed out that the operating loss of New Businesses narrowed significantly quarter-on-quarter to RMB 2.116 billion in Q1 (from RMB 4.65 billion in Q4), mainly benefiting from improved operational efficiency at Keeta. Looking ahead to Q2, UBS expects the loss in New Businesses to expand slightly to about RMB 2.4 billion, primarily driven by initial losses from entering new markets.