After the Shanghai Composite Index falls below 4,000 points, where will it go? Xingzheng Strategy: Keep a close eye on TSMC's July financial report and North American cloud manufacturers' Capex

The research report from Industrial Securities points out that although the Shanghai Composite Index has fallen below 4,000 points, raising concerns, there have been positive changes in core adjustment factors such as overseas liquidity, sentiment, and the global AI industry narrative. Market congestion indicators show that short-term sentiment has bottomed out, and this round of adjustment may be nearing its end, with a new round of upward momentum building. It is recommended to closely monitor TSMC's financial report in July and the Capex of North American cloud providers to grasp the subsequent trends

According to Zhitong Finance APP, Industrial Securities released a research report stating that the market experienced significant fluctuations this week. After being dragged down by the "de-leveraging" in the US, Japan, and South Korea at the beginning of the week, market sentiment recovered on Thursday following global AI industry developments. However, on Friday, the AI hardware sector saw a substantial pullback, and the Shanghai Composite Index fell below 4,000 points, leading some investors to have considerable concerns about the future market, especially the technology sector. However, at this current point and position, combined with recent changes, there are some positive signals accumulating behind the large fluctuations. The adjustments triggered by liquidity and industrial narratives may be nearing an end, and some key changes that will consolidate a new round of consensus are brewing.

With the recent key changes and positive signals validating the two core factors that previously affected market adjustments—overseas liquidity and sentiment, as well as the global AI industry narrative—there is no need for excessive concern about the future market. The momentum for a new round of upward movement is accumulating and brewing amid the fluctuations.

The main viewpoints of Industrial Securities are as follows:

1. Behind the large fluctuations: Positive signals are accumulating

The market experienced significant fluctuations this week. After being dragged down by the "de-leveraging" in the US, Japan, and South Korea at the beginning of the week, market sentiment recovered on Thursday following global AI industry developments. However, on Friday, the AI hardware sector saw a substantial pullback, and the Shanghai Composite Index fell below 4,000 points, leading some investors to have considerable concerns about the future market, especially the technology sector.

However, at this current point and position, combined with recent changes, there are some positive signals accumulating behind the large fluctuations. The adjustments triggered by liquidity and industrial narratives may be nearing an end, and some key changes that will consolidate a new round of consensus are brewing.

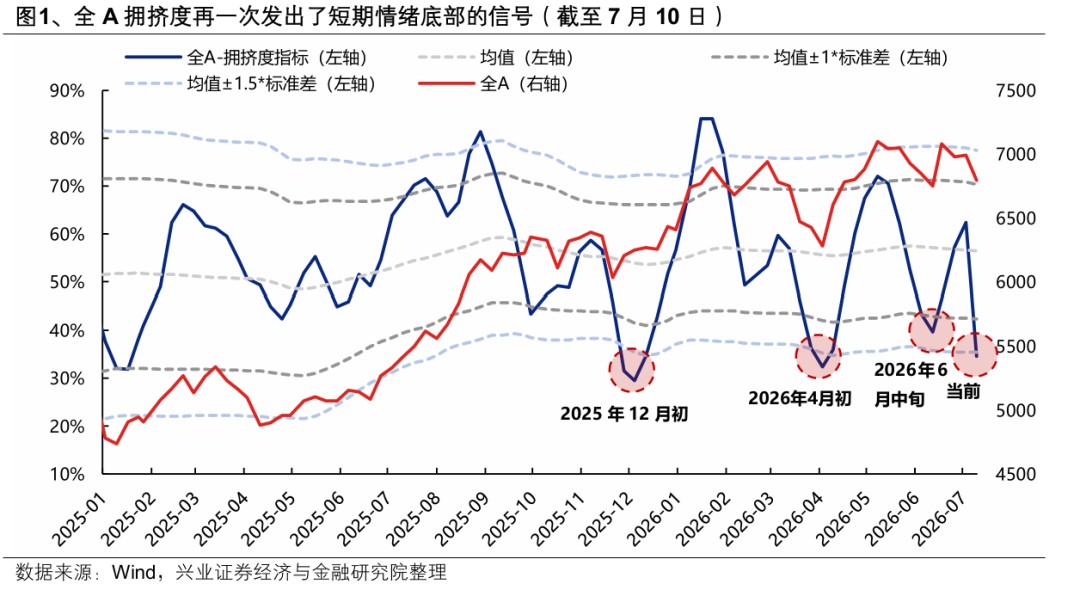

Firstly, for the overall market, the tracked crowding indicators have once again signaled a short-term emotional bottom. After adjustments dragged down by external factors and a reshuffling of holdings, the current crowding in the entire A-share market has fallen back to the bottom range of -1.5 standard deviations. Historically, significant bottom layout opportunities have emerged at similar crowding levels in early December 2025, early April 2026, and mid-June 2026.

Secondly, regarding the core factor that triggered this round of adjustments—the AI industry narrative—recent developments and performance validations from leading companies have, to some extent, corrected and reversed previous concerns. The core worries about AI in the market were primarily twofold: the peak demand for computing power and the slow commercialization realization. Recent advancements from leading companies have sufficiently addressed the biggest doubts in the market over the past few weeks:

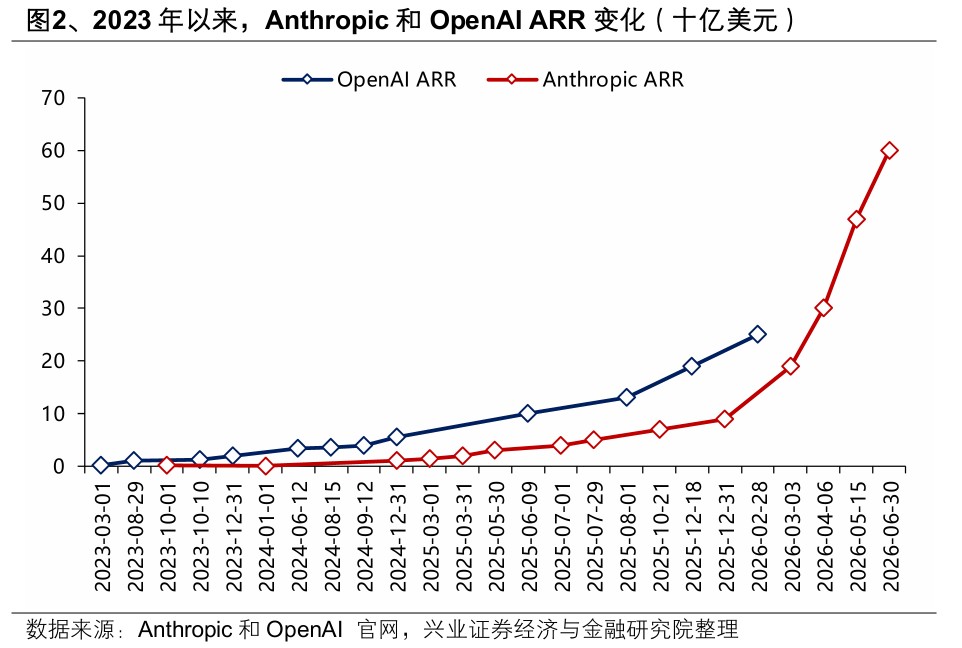

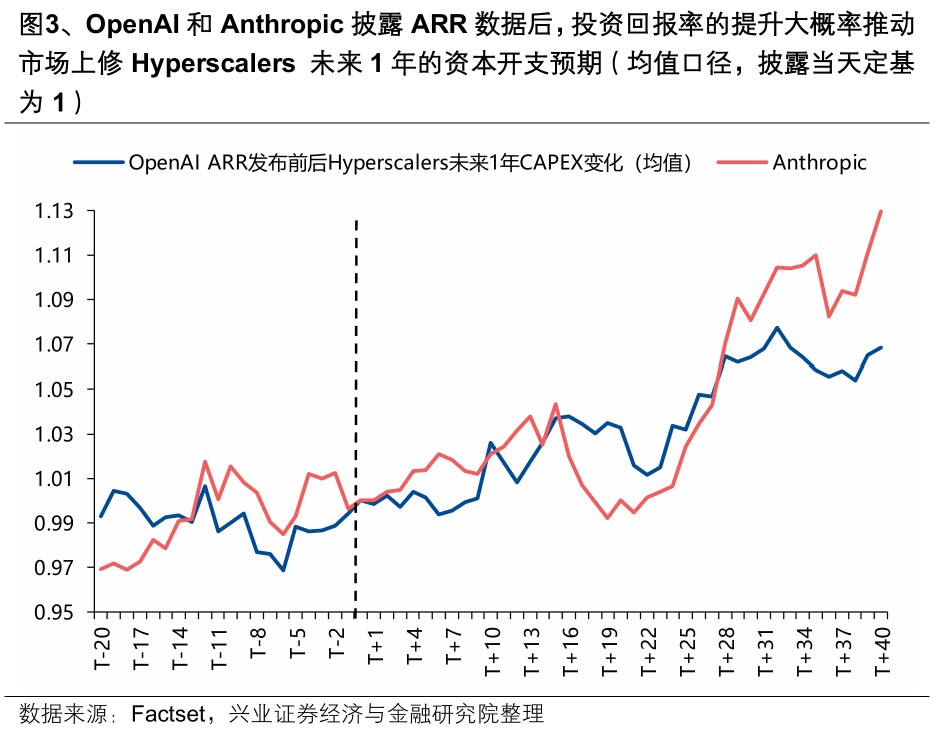

On the overseas front, firstly, major cloud companies still have a strong willingness to increase computing power, and secondly, the commercialization realization of model giants has exceeded expectations, with the foundation for the "spiral rise" of cloud companies' Capex and model vendors' ROI continuing. 1) Meta announced it will continue to invest in computing power; Broadcom received orders from Apple; Micron's expansion plans in the US continue to ramp up. 2) Anthropic's latest ARR surged from $9 billion at the end of 2025 to over $60 billion, proving to the market that the business model of large models is gradually becoming viable Under the background of high growth in model vendors' ARR, an increase in core cloud vendors' Capex is expected.

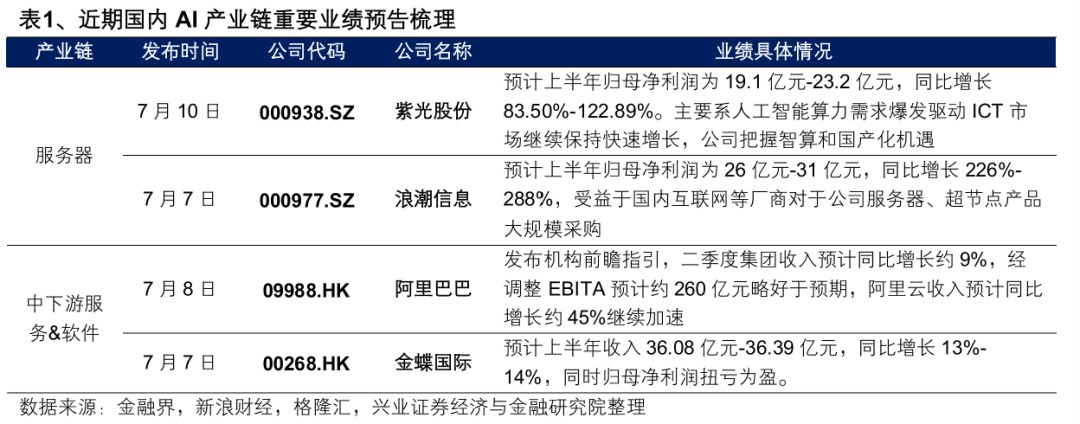

The same is true domestically, even exceeding market expectations, becoming the direction with the largest marginal change in recent narratives. First, Changxin's IPO is expected to drive domestic Capex into a new upward cycle; second, the performance of domestic computing power has already begun to materialize; third, domestic AI services and applications have started to generate profits. 1) After Changxin's IPO, it will enter an expansion cycle, driving orders for upstream domestic equipment, components, and materials, pushing domestic semiconductor Capex into a new upward cycle. After the improvement in the availability and confidence of domestic supply, the easing of GPU delivery constraints is also expected to accelerate the realization of domestic computing power performance; 2) The performance of some leading companies in the domestic AIDC chain has greatly exceeded market expectations, proving that under the prosperity of domestic computing power demand, the release of the domestic computing power chain has already begun, becoming a direction with significant expectation differences recently. 3) In Alibaba's latest forward guidance, cloud business revenue continues to grow rapidly, and the services and applications in the domestic AI mid-to-lower reaches have begun to realize performance.

Therefore, with the recent key changes and positive signals validating the two core factors that previously affected market adjustments—overseas liquidity and sentiment drag, and the global AI industry narrative—there is no need to overly worry about the subsequent market; the momentum for a new round of increases is accumulating and brewing amid fluctuations.

II. Behind the Big Fluctuations: What is the Market Waiting For?

However, the biggest impression the market gives recently is still one of rotation and speculation, with the intensity of tracked industry rotations rising to a relatively high level this year. On one hand, the core focus of the market—AI computing power hardware—is gradually coalescing into a new round of consensus, but it remains highly volatile; on the other hand, some low-performing sectors have also seen phase-specific recoveries, but the sustainability of the market is relatively limited.

The core reason for the current market state is that AI computing power hardware is undoubtedly the largest consensus in the market, but funds are rotating and oscillating while waiting for clearer right-side validation signals, and the arrival of such signals is not far off. The core validations to focus on in the future are: First, before July 15, potential performance catalysts for leading companies. July 15 is the deadline for A-share listed companies to disclose performance forecasts. Pay attention to the peak disclosure period in the following days to see if there are any technology leaders whose performance can better consolidate market consensus and validate the prosperity trend.

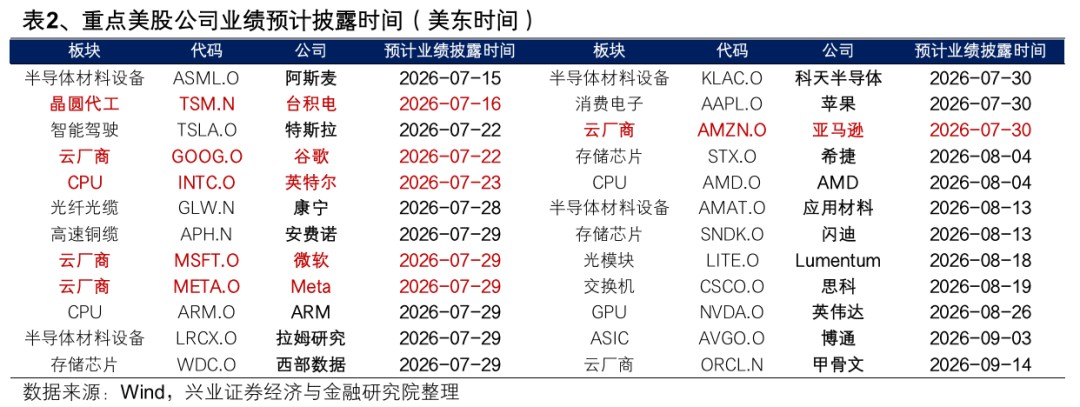

Second, on July 13, Taiwan Semiconductor will announce June revenue, and on July 16, it will announce the second-quarter financial report and subsequent guidance. As an upstream player in the computing power industry chain, changes in global demand will be directly reflected in its financial report data and guidance. The announced order situation, capital expenditure planning, and capacity deployment guidance will help the market more clearly assess the sustainability of future global AI computing power demand.

Third, and most critically, the capital expenditure guidance from the four major cloud providers in North America in late July. This is undoubtedly the current core focus of the market, validating the sustainability of global computing power demand and the prosperity of AI computing hardware leaders. The mainstream view still believes that capital expenditure will continue to be revised upward, and clarity will come after further communication between cloud providers and the market. The earliest is Google's financial report on July 22.

Subsequently, as these right-side signals that validate the global computing power prosperity and the sustainability of AI hardware manufacturers' performance become clearer, it will help the market reduce volatility, choose direction, and select structure.

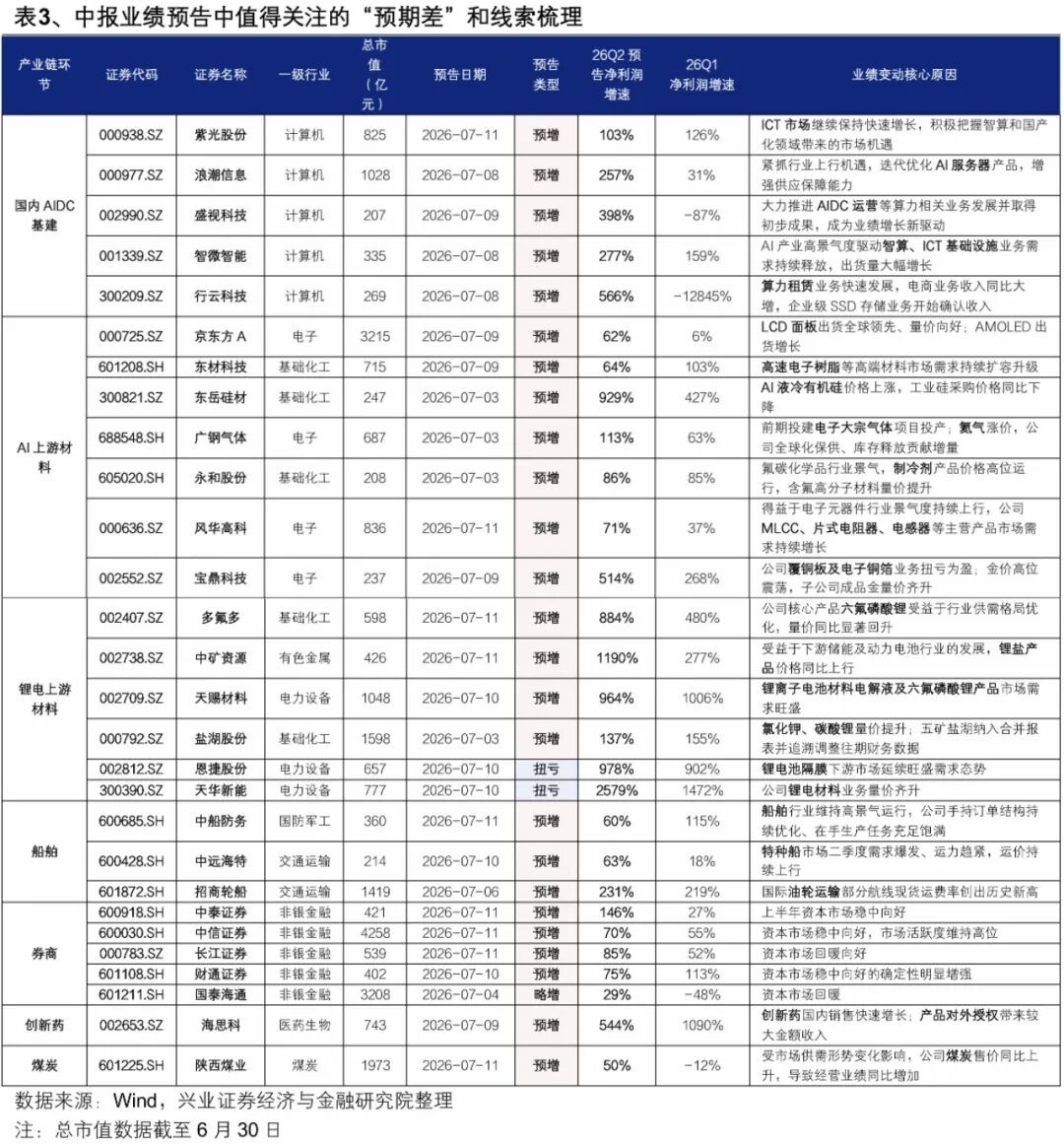

Three, clues worth paying attention to in the current mid-term performance forecasts

Before the arrival of the aforementioned core validations, the market may continue to revolve around some domestic prosperity clues for supplementary gains. The "expectation gap" and clues worth paying attention to in the current mid-term performance forecasts are:

AI-related demand remains the most important driving factor for the prosperity of listed companies, and the areas it drives are continuously spreading along the upstream and downstream: 1) The domestic AIDC infrastructure chain (servers, ICT infrastructure, computing power leasing, etc.) benefits from the expansion of domestic computing power demand and has begun to deliver performance, becoming the direction with the largest marginal changes and expectation gaps; 2) Capacity expansion drives price increases in upstream AI materials, releasing performance: MLCC, copper-clad laminates, electronic special gases, resins, panels, refrigerants, etc.

Other clues worth noting: 1) A large number of lithium battery materials (membranes, positive and negative electrode materials, electrolytes, lithium iron phosphate, lithium salts, etc.) companies are experiencing high growth and turning losses into profits; 2) Innovative drugs, shipping, brokerages, and coal are currently low-performing clues worth paying attention to.

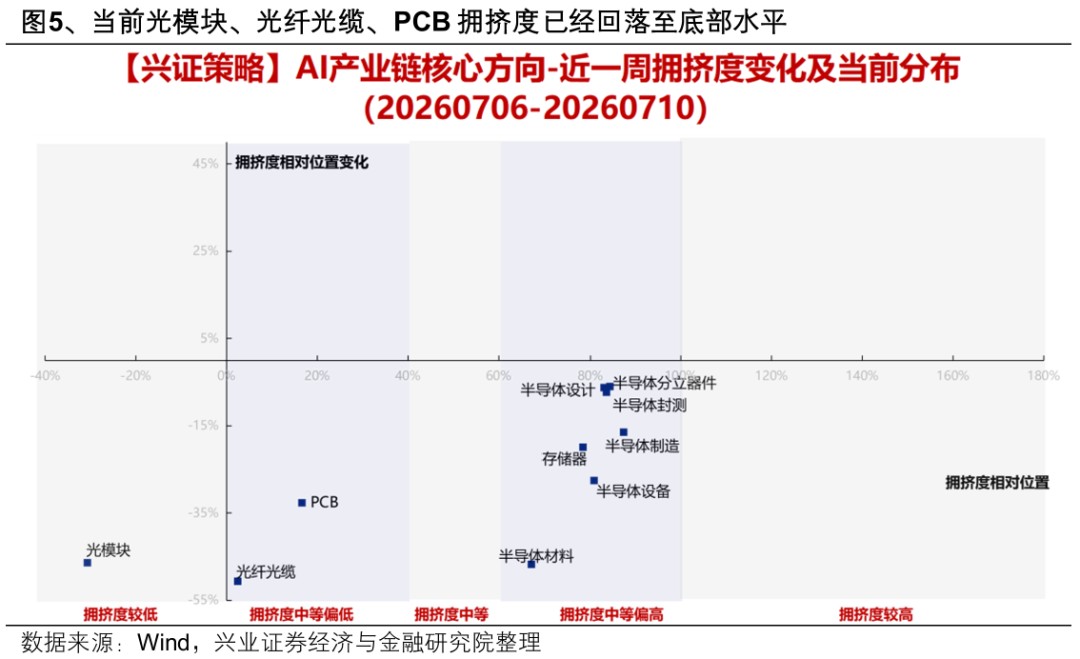

For AI computing hardware (optical communication, semiconductor industry chain) with strong prosperity consensus, although the disclosed mid-term performance forecasts can continue to validate the accelerating prosperity trend, the market is still waiting for core leaders' performance, as well as overseas financial reports, guidance, and other right-side signals. Internally, pay attention to the cost-effectiveness of the current North American computing power chain. On one hand, the congestion levels of optical modules, optical fibers, and PCBs have already fallen to bottom levels; on the other hand, the price comparison between A-share North American computing power chain leaders and domestic computing power chain leaders has accelerated to fall back to last June's levels

Risk Warning

Fluctuations in economic data, policy easing lower than expected, Federal Reserve interest rate cuts not meeting expectations, escalation of geopolitical tensions, etc