Taiwan Semiconductor's Profits Surge 77%, Yet Stock Plummets as "Buy the Rumor, Sell the News" Plays Out Again!

Taiwan Semiconductor's Q2 results comprehensively beat Consensus Estimates, with AI demand remaining robust. However, with Taiwan Semiconductor's ADR already up approximately 77% year-to-date, the positive news was largely priced in. Following the earnings release, the stock fell nearly 4% in pre-market trading, validating the "buy the rumor, sell the news" dynamic once again. Amid high valuations, the market is no longer satisfied with merely "excellent" performance but demands "continuous Earnings Beat," a common challenge facing all AI leaders

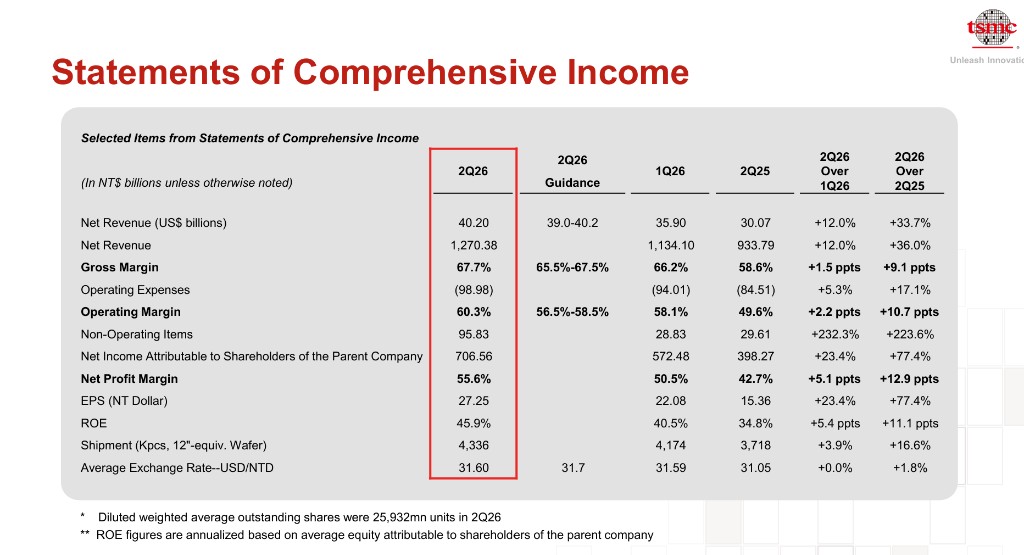

On July 16, Taiwan Semiconductor delivered a nearly flawless quarterly performance.

Data showed that the company's net profit for the second quarter increased by 77% year-over-year, with revenue, gross margin, operating profit margin, and third-quarter revenue guidance all exceeding market expectations. AI demand remained strong, and the contribution from advanced processes further increased, indicating that the global boom in AI computing power investment is continuing.

However, the impressive results did not translate into a stock price increase. Following the earnings announcement, Taiwan Semiconductor's ADR fell nearly 4% in pre-market trading, as the market once again enacted the "buy the rumor, sell the news" scenario—after the stock price cumulatively rose about 77% over the past year, some investors chose to take profits after the good news was realized.

For the market, the focus is no longer just on whether the performance is impressive enough, but on whether the company can continue to deliver results that exceed expectations against a backdrop of high valuations and high expectations. This is also a test currently faced by all leading AI companies.

Amid High Expectations, the Market Begins to Cash In

Although Taiwan Semiconductor's performance continues to break records, the focus for investors has shifted from just growth speed to whether valuations can continue to rise.

Ricky Ho, fund manager at Four Capital in Singapore, stated that market expectations for Taiwan Semiconductor are currently at "exceptionally high levels," and future stock price increases will increasingly depend on management consistently exceeding market expectations.

Meanwhile, discussions surrounding AI infrastructure investment continue. The market is watching whether the expanding capital expenditures of tech giants will ultimately yield sufficient returns. Additionally, SK Hynix's prediction that the supply shortage of AI memory chips like HBM will persist until after 2030 indicates that the AI industry's prosperity has not significantly cooled.

Profits Grow 77%, Advanced Process Share Increases Further

According to a previous article by Wallstreetcn, data released by Taiwan Semiconductor on Thursday showed that net profit for the second quarter ended June 2026 reached NT$706.6 billion (approximately $22 billion), a 77.4% year-over-year increase, higher than the analyst consensus estimate of NT$623.7 billion; revenue grew 36% year-over-year to approximately $40.2 billion, nearing the upper end of the company's previous guidance range of $39 billion to $40.2 billion.

Profitability also exceeded market expectations. The gross margin for the second quarter was 67.7%, higher than the market expectation of 67.1%; the operating profit margin reached 60.3%; and earnings per share were NT$27.25, higher than the FactSet consensus of NT$24.20.

Advanced processes remain the core of growth. Processes of 7nm and below accounted for 77% of wafer revenue, with 5nm accounting for 33%, 3nm for 30%, and 7nm for 11%. The 2nm process contributed to revenue for the first time this quarter, accounting for 3%.

Charles Shum, an analyst at Bloomberg Industry Research, stated that demand for AI server chips is sufficient to offset weakness in the smartphone and PC markets and is expected to support Taiwan Semiconductor in further raising product prices, pushing gross margins closer to the management target of 67.5%.

AI Demand Remains Strong, Q3 Guidance Continues to Exceed Expectations

Taiwan Semiconductor expects third-quarter 2026 revenue to fall between $44.6 billion and $45.8 billion, which is not only higher than the previous quarter but also exceeds the FactSet market consensus ($43.67 billion). Chairman and President C.C. Wei explicitly stated during the conference call that "AI-related demand remains very strong," providing strong support for performance growth.

As the core foundry for AI chip manufacturers such as Nvidia, Apple, and AMD, Taiwan Semiconductor's capital expenditure is closely watched by the market. The company reaffirmed that its 2026 capital expenditure will be close to the historical high of $56 billion, seen as an important indicator measuring the heat of global AI infrastructure investment. Wei also pointed out that even with the continued expansion of U.S. factories, capacity will still struggle to fully meet customer demand in the coming years.

In terms of capacity layout, Taiwan Semiconductor announced an additional investment of approximately $100 billion in Arizona, bringing the total committed investment in the region to approximately $265 billion, to further strengthen advanced process capabilities in the United States. Over the past year, Taiwan Semiconductor's ADR has cumulatively risen by about 77%, with its market capitalization approaching $2 trillion, making its performance a key barometer for observing the prosperity of the global AI industry chain.

Meanwhile, the market is also paying attention to how the company will handle competition from emerging technologies such as Intel's EMIB-T packaging, as well as the increasingly fierce industry rivalry in the advanced packaging sector. The competitive landscape in this area is becoming a new focal point of semiconductor contention, following process technology.