Liang Wenfeng Goes All In on IPO Subscription; Trillion-Yuan CXMT Snapped Up

On July 16, 2026, domestic memory chip leader CXMT launched its IPO, raising RMB 57.9 billion and setting a new record for the STAR Market. Public funds subscribed enthusiastically, while shareholders such as Hefei State-owned Assets and Alibaba anticipate substantial paper gains. Meanwhile, the memory sector diverged, with heavyweight stock TWSC hitting the limit down. CXMT’s performance turnaround has attracted market attention, but employee share lock-ups will last for more than three years

On July 16, 2026, the A-share memory sector witnessed an extremely divided scene.

On one hand, memory leader TWSC hit the limit down at the open, with 1.1 million lots of sell orders pressing on the board; despite its earnings increasing fifty-fold, it was still slammed by sellers. On the other hand, domestic memory leader CXMT began its new share subscription on the same day. With a fundraising amount of RMB 57.9 billion, it can be said that the largest IPO of the year in the A-share market, and the third largest in history, has arrived, breaking the STAR Market IPO fundraising record and leaving behind the historical peak of RMB 53.2 billion held by SMIC.

A total of 93 public fund companies participated in the initial inquiry for CXMT, managing a combined 5,419 valid quoted allocation objects. The proposed total subscription volume reached 679.7793 billion shares, accounting for approximately 54.9% of the total valid proposed subscriptions. Top-tier funds were almost all involved—E Fund, Southern Asset Management, ICBC Credit Suisse Asset Management, Fullgoal Fund, Guotai Junan Securities, and China Asset Management each submitted applications exceeding 40 billion shares.

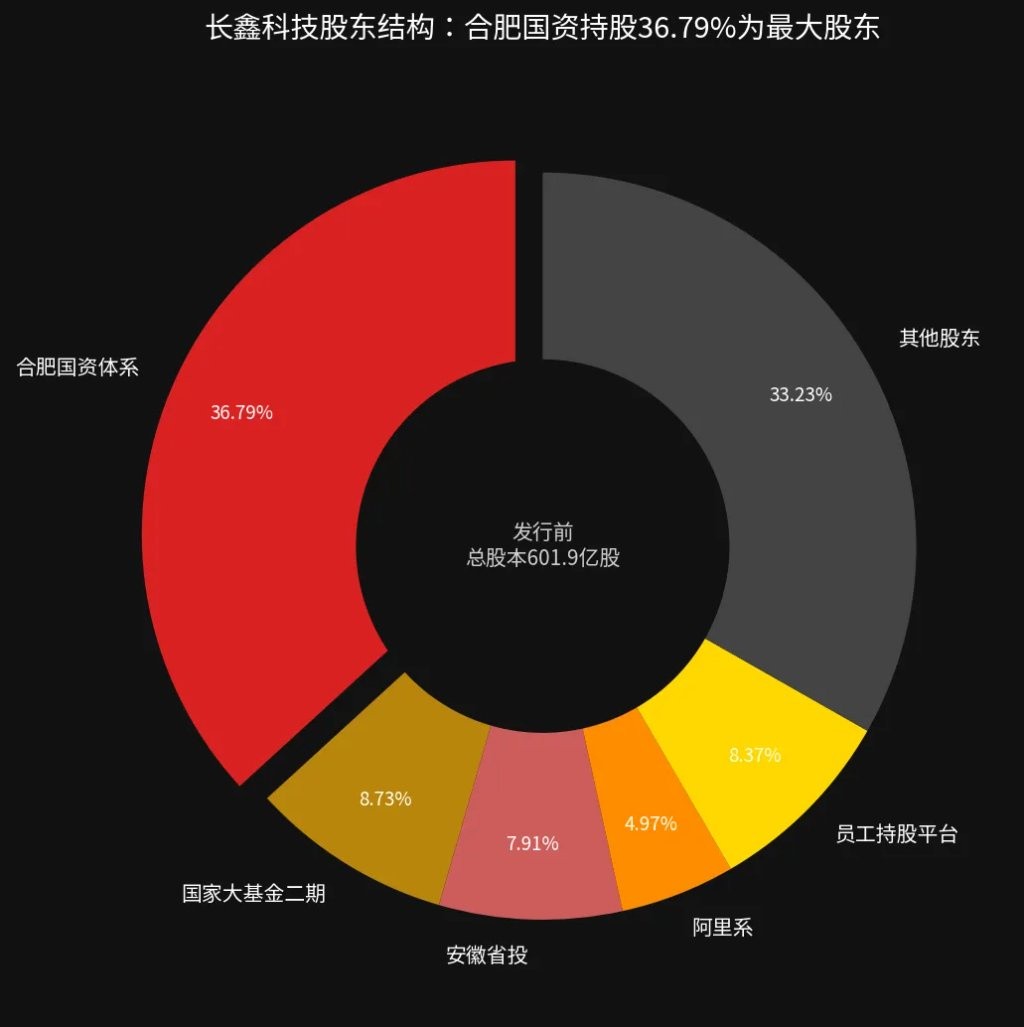

As a trillion-yuan giant enters the market, people cannot help but associate it with huge wealth effects. Among them, the biggest winner is Hefei State-owned Assets. After penetrating the equity structure, Hefei State-owned Assets holds approximately 36.79% of CXMT’s shares. If calculated based on a market capitalization of RMB 2 trillion, starting from the initial investment of RMB 14.4 billion in Phase I in 2016, plus cumulative investments totaling RMB 30 billion over the subsequent decade, its paper profit exceeds RMB 700 billion. Even calculated at the lowest market capitalization of RMB 580 billion, its paper profit remains close to RMB 200 billion. In addition, Alibaba is the biggest winner among external shareholders in this round, with a combined shareholding of 4.97%. If calculated at the lowest market capitalization, the paper profit exceeds RMB 20 billion, approaching RMB 100 billion at the highest market capitalization.

Among CXMT’s 19,000 employees, more than 35% hold shares. Although listing is expected to create thousands of multi-millionaires in batches, the lock-up period for these shares is more than three years, released in tranches. To secure this wealth, one must see how long this memory cycle can last.

Regardless, CXMT’s comeback story is inspiring enough: from no profits to earning RMB 300 million daily, from a massive loss of RMB 36.6 billion to a net profit of over RMB 50 billion in half a year, and tearing a crack in the dominance of the three international memory giants. CXMT completed in one year what takes other companies ten years. This is a story about ambition, patience, and confidence.

Memory Stumbles, CXMT Takes the Stage

On the morning of July 16, memory leader TWSC opened with another limit-down, bringing its market capitalization back to RMB 135.2 billion. However, its performance was not poor: revenue in the first half ranged from RMB 16 billion to RMB 18 billion, a year-on-year increase of more than three times; net profit attributable to shareholders ranged from RMB 5.7 billion to RMB 6.5 billion. While it was losing money in the same period last year, this year it increased fifty-fold.

But the market did not buy it. Breaking it down, it earned RMB 3.346 billion in the first quarter, but in the second quarter, it dropped by 6% to 30% quarter-on-quarter. As a typical cyclical sector, the market never looks at “how much was earned,” but rather “whether more can be earned next.” Once growth slows, capital votes with its feet.

TWSC is not an isolated case. The entire memory sector has been falling recently.

On the same day, CXMT began new share subscription on the STAR Market. The issue price was RMB 8.66 per share, with 500 shares per lot, requiring a payment of RMB 4,330 if allocated. Although the unit price does not seem high, the large scale makes it significant: an initial issuance of 6.688 billion shares raised a total of RMB 57.9 billion. If the over-allotment option is fully exercised, it could raise RMB 66.6 billion, breaking the STAR Market IPO record.

A listing valuation of RMB 580 billion is not small for the A-share market, but it is not terrifying either. What is truly surprising is another number: on July 15, perpetual contracts for CXMT quietly appeared on Hyperliquid, a decentralized trading platform. The price surged to around USD 8, equivalent to approximately RMB 54. Multiplying this price by the total share capital, overseas capital implied a market capitalization of RMB 3.5 trillion for CXMT.

It is not to say that overseas capital is necessarily right, but this price difference itself indicates one thing: there is a serious divergence in the market’s pricing of CXMT.

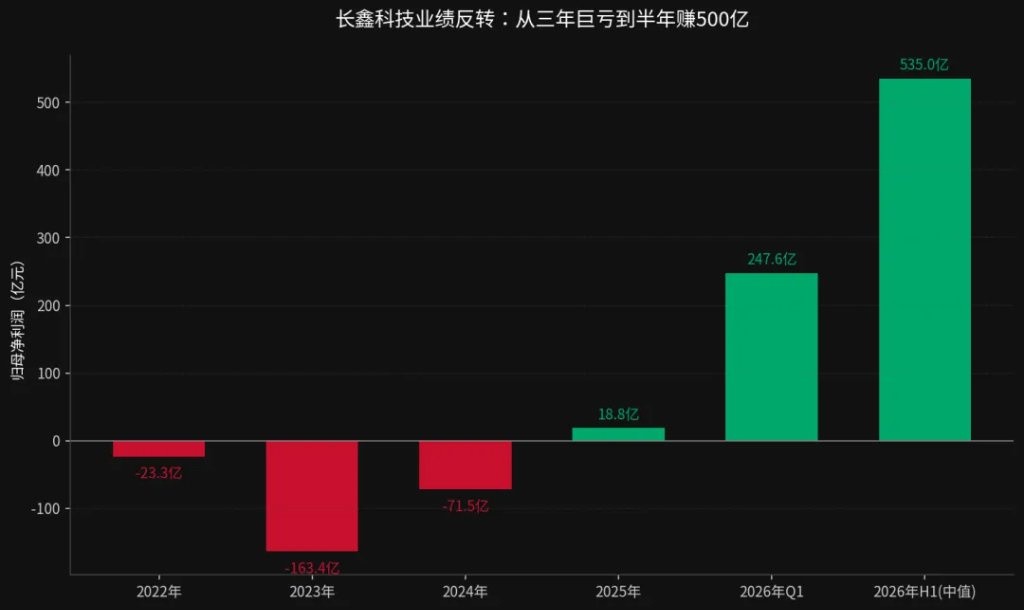

Where does the divergence come from? Looking at the financial data makes it clear. From its establishment in 2016 to 2024, CXMT suffered losses for many consecutive years, accumulating a deficit of RMB 36.65 billion. In 2025, the full-year net profit was RMB 1.875 billion, just crawling out of the quagmire of losses. But in 2026, the first quarter saw a stunning reversal: revenue reached RMB 50.8 billion, a year-on-year increase of 719%; net profit attributable to shareholders was RMB 24.762 billion, a year-on-year increase of nearly 17 times. The company expects first-half revenue of RMB 110 billion to RMB 120 billion, and net profit of RMB 50 billion to RMB 57 billion, averaging nearly RMB 300 million in net profit per day.

Losing over RMB 30 billion in three years and earning back over RMB 50 billion in half a year. This level of volatility is rare in the history of the A-share market.

The question is: valuing based on dynamic earnings assumes that profitability can be sustained. Memory is a strongly cyclical industry, with good times and bad times alternating. How much of CXMT’s current windfall profits are due to its own capabilities, and how much are due to the cycle?

Chairman Zhu Yiming said during an online roadshow on July 15 that, starting with the first self-developed DDR4 chip in 2019, CXMT has been engaged in leapfrog R&D. Now, DDR5 and LPDDR5/5X are in mass production, and the fourth-generation process platform has also been successfully implemented. The funds raised from the listing will mainly be used for technological R&D and capacity expansion.

Indeed, mainland China was basically blank in the DRAM field previously, with Samsung, SK Hynix, and Micron occupying more than 90% of the global market. CXMT is the only mainland enterprise to have successfully produced DRAM. The step from 0 to 1 indeed took many years to achieve.

However, producing it is different from producing it cheaply and well. The competitive logic of memory chips is simple: whoever has more advanced processes, higher yields, and larger capacity makes money. CXMT’s current process nodes still lag behind the three giants, but relying on huge domestic market demand and policy dividends for domestic substitution, it managed to capture significant profits during the upcycle.

This issuance attracted strategic placements from “national team” investors such as the National Social Security Fund and Basic Old-Age Insurance Fund, as well as a batch of enterprises in the industrial chain. The lock-up period starts at 12 months, with some extending up to 36 months.

In this round of applying for an IPO, institutions are truly scrambling.

Liang Wenfeng’s 153 Cards and Retail Investors’ Arithmetic

Among those scrambling the most fiercely, one person cannot be overlooked: Liang Wenfeng.

In the issuance announcement released by CXMT on July 14, the list of offline investors showed that 153 private equity products under High-Flyer Quant appeared together in the subscription list. The proposed subscription price for each product was RMB 8.78, with a maximum subscription quantity of 230 million shares per transaction. Most of High-Flyer’s products reported between 70 million and 140 million shares.

All 153 products, without exception, came to apply for an IPO.

High-Flyer Quant is currently one of the largest quantitative private equity firms in China, with assets under management exceeding RMB 70 billion. Its average return in 2025 was 56.55%, ranking second among quantitative private equity firms with over RMB 10 billion in AUM. Its actual controller is Liang Wenfeng, who holds 85% of Zhejiang Jiuzhang Assets and 85.15% of Ningbo High-Flyer Quant.

Li Wenfeng is usually low-key and rarely speaks publicly. But High-Flyer’s move this time was too conspicuous. Offline IPO subscription is different from retail online subscription; offline involves quoting prices and quantities first, and the allocation rate depends on whether the quote is within the valid range. Mobilizing all 153 products to subscribe to the same new stock is not a casual operation. This represents their clear judgment on CXMT’s pricing, and their willingness to bet real money.

Another name worth noting is Li Bin.

In the strategic placement list, NIO Power Technology (Hefei) Co., Ltd. was prominently listed, receiving an allocation of approximately RMB 158 million, with a lock-up period of 18 months. Also in the same batch were Shenzhen Sankuai Network Technology, ZTE Corporation, and Chery Intelligent Automotive Technology, each receiving the same allocation amount and having a lock-up period of 18 months. Alibaba Cloud Feitian Information Technology also received the same amount, but its lock-up period was 36 months, double that of NIO.

Why did NIO participate in CXMT’s strategic placement? Aside from NIO’s deep ties with Hefei, DRAM is used in almost all electronic devices—phones, servers, and cars. The demand for memory in smart cars is expanding rapidly. Autonomous driving requires processing massive amounts of sensor data, and in-car systems are becoming increasingly complex. From the perspective of supply chain security, binding with the domestic DRAM leader is a no-loss strategy.

Li Bin’s logic for this decision is probably simple: NIO sells hundreds of thousands of cars a year, and every car needs memory chips. Rather than being choked by Samsung and SK Hynix in the future, it is better to get on the same boat with CXMT now. An 18-month lock-up period is not long; it is a normal level for strategic investments.

For ordinary investors, subscribing to CXMT’s IPO has several layers.

First, let’s talk about the subscription itself. On the STAR Market, one lot is 500 shares, requiring a payment of RMB 4,330, which is not a high threshold. Due to the large issuance size, institutions estimate that the online allocation rate may reach 0.3% to 0.7%, significantly higher than that of general new stocks. If calculated based on institutions’ neutral expectation that the market capitalization will surge to RMB 3 trillion after listing, winning one lot could earn approximately RMB 20,000. If sentiment is hotter and the market capitalization reaches RMB 5 trillion, the profit per lot could reach RMB 33,000.

IPOs in the A-share market have indeed been profitable this year. In the first half, none of the 71 newly listed stocks broke the issue price on the first day, with an average increase of 233%, creating a five-year high. Semiconductors and high-end manufacturing are the sectors with the highest premiums. Muxi Shares rose 693% on the first day, earning RMB 360,000 per lot; Lianxun Instruments rose 875%, earning nearly RMB 360,000 per lot; Changjin Photonics was even more exaggerated, rising 1,510%.

But there is a fundamental problem here: the money earned from IPOs is essentially a “first-day liquidity premium,” not value discovery. You are earning the spread between the primary and secondary markets, which is a different matter from whether the company is good or worth the price.

Moreover, CXMT’s issue price of RMB 8.66 is nearly double the previous market estimate of RMB 4.41, indicating that the pricing is no longer cheap. An issue P/E ratio of 308 times means that if performance growth falls short of expectations, there will be significant room for valuation correction.

Next, let’s look at the memory industry itself. TWSC’s limit down despite excellent performance already clarifies one thing: the market’s pricing logic for the memory industry has changed. Previously, it was “when prosperity comes, everyone rises together”; now it is “you rise yours, I fall mine.” After CXMT’s listing, market capital will concentrate more on leaders, while small and medium-sized memory enterprises may instead suffer capital outflows.

Can CXMT’s listing save the memory industry? The answer is probably: It cannot save the industry, but it itself is likely to live very comfortably. Whether the memory industry can recover depends on the global supply and demand cycle, the capital expenditure rhythm of Samsung, SK Hynix, and Micron, the demand intensity of the mobile phone and server markets, and the driving effect of AI on HBM (High Bandwidth Memory).

These are not things that CXMT alone can decide. But for China’s memory industrial chain, the fact that CXMT has produced, mass-produced, profited from, and listed DRAM means that mainland enterprises finally have their own position in the global DRAM market. What remains to be seen is whether it can withstand the next downturn cycle.

Risk Warning and Disclaimer

The market carries risks; investment requires caution. This article does not constitute personal investment advice, nor does it take into account the specific investment objectives, financial status, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances. Investment based on this is at your own risk.