MicrosoftAlphabet-C handed in their assignments at the same time, and Alphabet-C made a stunning comeback and earned a big profit.

不懼微軟挑戰,谷歌廣告、雲業務雙狂飆。微軟總體依然穩健,但 AI 並未如預期發力。

本季度最有看點、最受關注的一個財報日來了。

谷歌和微軟在 AI 業務上的強強對決還在持續,而這次,兩家巨頭的季度財報甚至都放在了同一天發佈。

過去一個季度,谷歌和微軟之間的 “戰鬥” 可以説是非常焦灼。谷歌 IO、微軟 Build 等年度大會先後登場,兩家公司關於 AI 的模型更新、產品發佈應接不暇。但大家都好奇的是,AI 是否給真正給它們帶來了用户和收益,兩家公司誰的表現又更勝一籌?

下面,讓我們在它們最新的季度財報中去找答案。

不懼微軟挑戰,谷歌廣告、雲業務雙狂飆

在微軟大舉進軍 AI 之後,市場都為之前的 AI 霸主谷歌捏了一把汗。畢竟微軟現在搜索、生產力工具、雲業務上發起的猛攻都指向谷歌的要害。今年一季度,谷歌的營業利潤、每股收益等關鍵指標也均不達標,出現了明顯的下降。

但這次,谷歌完全頂住了壓力,不僅各項指標遠超出市場預期,廣告業務似乎完全擺脱頹勢重回穩定增長區間,雲業務的強勢增長也讓人眼前一亮。

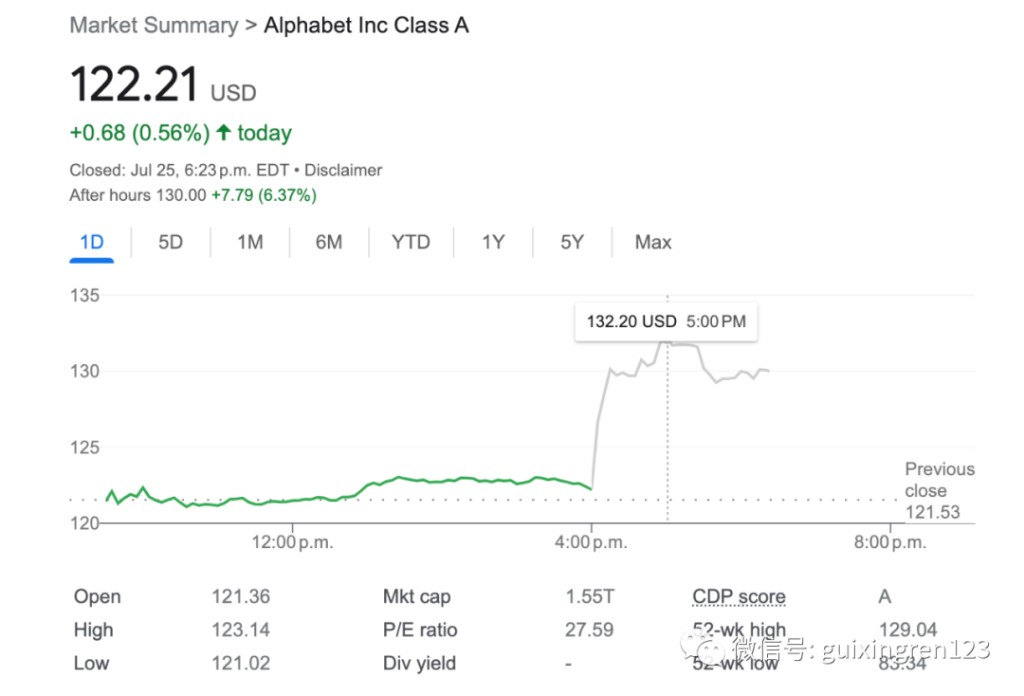

谷歌二季度實現營收 746.04 億美元,同比增長 7%,遠遠超出市場預期 4.4% 的增長和 727.7 億美元的營收預期。雖然增速還沒有回到兩位數,但已經遠好於上季度 3% 的同比增長。

從盈利指標來看,二季度稀釋後每股收益為 1.44 美元,同比增長 19%,高出市場 9.1% 的增長預期,而上一季度這一指標同比下降了 4.9%;營業利潤 218.38 億美元,同比增長近 12.3%,遠高出市場預期的 2.6%,而上一季度同比下降 13.3%。

從分項業務來看,谷歌本季度也一掃上季度的陰霾、大獲全勝。

其中廣告、搜索、地圖、YouTube、硬件、安卓、Chrome 和 Google Play 在內的谷歌服務錄得662.85 億美元收入,同比增長約 5.5%,其中,廣告板塊的表現尤為亮眼,不僅止住了兩個季度的連跌,搜索業務和 YouTube 的增長都超出了預期。

二季度整體廣告創收 581.43 億美元,同比增長 3.3%,高出市場 2.1% 的預期。谷歌搜索及其他相關業務收入為 426.28 億美元,同比增長約 4.8%,比上一季度的 1.9% 增長加速不少。YouTube 在連續幾個季度讓市場失望之後,本季度增長 4.4%,遠高出分析師 1% 的低增長預期,創收 76.65 億美元。

除了廣告外,大家尤為關注的第二增長曲線的雲業務也繼續延續了高增長的勢頭,並未遭受市場預期的來自 AWS 和微軟雲的猛烈衝擊。

二季度谷歌雲營收 80.31 億美元,同比增長約 28%,跟一季度增速持平,高出了市場 24.8% 的預期,並未出現增長明顯放緩的趨勢。值得注意的是,在上一季度谷歌雲取得歷史上首次盈利之後,本季度雲業務繼續保持盈利,錄得3.95 億美元的利潤,較上一季度的 1.91 億美元翻倍,而去年同期虧損還高達 5.9 億美元。

谷歌本季度的亮眼財報表現也直接體現在了股價上。今日美股盤後,谷歌股價一度大漲超過 7%。

雖然關鍵業績指標喜人,但谷歌此次並沒有過多的談論 AI 以及 AI 給業務帶來的影響。在財報會上,跟 AI 相關的主要事項有兩方面。一是谷歌宣佈了一項高層人事變動,谷歌的首席財務官 Ruth Porat 將擔任首席投資官(CIO),在谷歌尋找新 CFO 的人選之前她將兼任兩份工作,作為 CIO 她將負責谷歌包括 AI、自動駕駛等創新部門在全球的投資。二是谷歌表示今年將持續加大在數據中心和服務器方面的投資,釋放了強勁的為 AI 服務的信號。

對 AI 的投入目前也並沒有大幅增加谷歌的業務支出。谷歌本季度的資本支出 68.9 億美元,遠低於市場預期的 80.1 億美元。

微軟總體依然穩健,但 AI 並未如預期發力

相較於隔壁一片歡欣鼓舞的谷歌,今年高歌猛進了半年多的微軟這次就顯得有點不温不火。

如果用一個字來評價微軟的業績表現,那 “穩” 字可能最合適不過。

本季度微軟的關鍵業績指標雖然不算驚豔,但也都高出了市場預期。微軟財報顯示,第四財季營收 562 億美元,同比增長 8%,雖然不及去年同期的兩位數增長,但仍然高於了 554.9 億美元的市場預期;淨利潤增長 20% 至 201 億美元,攤薄後每股收益 2.69 美元,同比增長 21%。

但從整個財年來看,微軟今年的表現稍微有些遜色。全年營收為 2119 億美元,同比增長 7%,但過去五個財年該指標均保持了兩位數的增長。

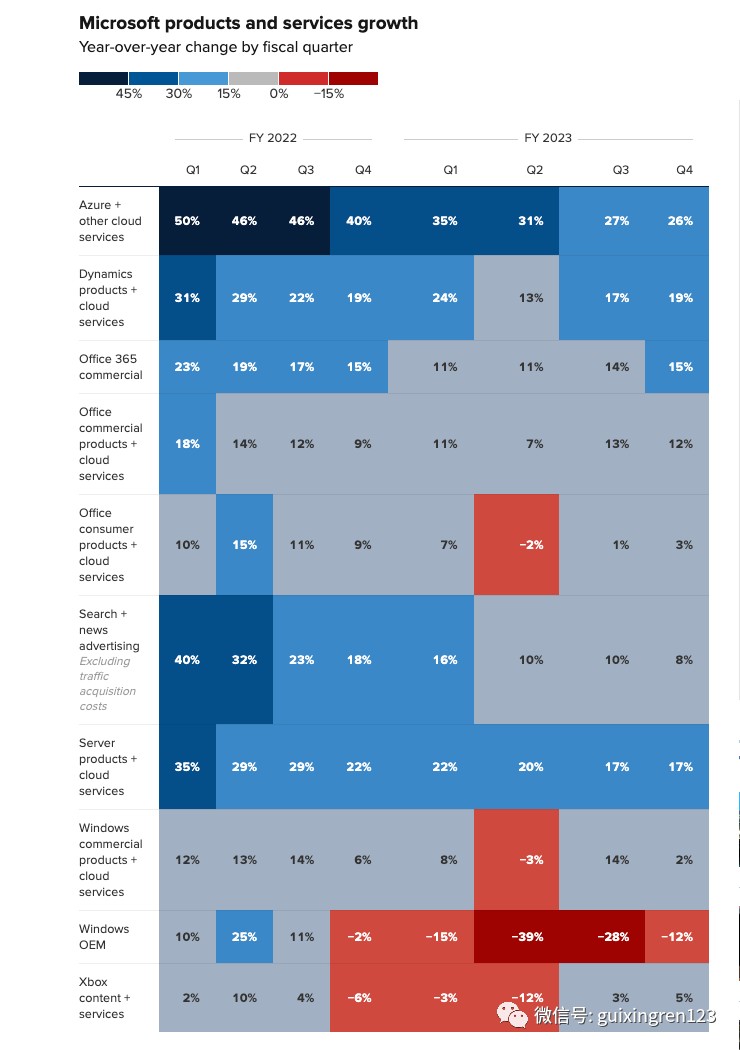

從分項業務來看,微軟的生產力和業務流程部門(包含 Office 生產力軟件、LinkedIn 和 Dynamics)實現了 182.9 億美元的收入,增長了 10%,超過了預期的 180.6 億美元,其中辦公室消費者產品和雲服務營收同比增長 3%,微軟 365 消費者訂閲數增長至 6700 萬,LinkedIn 營收同比增長 5%。

包括 Windows、設備、遊戲和搜索廣告的更多個人計算業務,營收為 139.1 億美元同比下降降約 4%。其中,Windows 操作系統營收同比下降 12%;硬件設備營收同比下降 20%;Windows 商業產品和雲服務營收同比增長 2%;搜索和新聞廣告服務營收同比增長 8%。

從中或許可以看到,Bing 搜索集成 AI 之後帶了比較明顯的增長,但 Windows 系統和 Office 層面 AI 對收入的拉動能力還並沒有顯現。

除了 AI 沒有預期般發力之外,此次微軟雲的表現也並沒有讓市場滿意。

雖然本季度微軟智能雲業務營收同比仍然增長了 15% 至 239.9 億美元,高於市場預期的 238 億美元。但 Azure 和其他雲服務業務僅增長 26%,而上一季度為 31%,這説明 Azure 已經連續幾個季度放緩,讓人擔心雲業務是否進入了增長乏力的階段。要知道,在疫情期間 Azure 曾連續保持了 50% 的高速增長。

在隨後的電話會上,微軟似乎也證明了這種擔憂。微軟預計 2024 財年第一季度 Azure 營收增長率將為 25% 至 26%,這也意味着雲業務增速將進一步放緩。此外,微軟也給出了略顯悲觀的業績指引,預計下一季度智能雲收入為 233-236 億美元,個人計算業務收入為 125-129 億美元,生產力和商業業務收入為 180-183 億美元,都不及市場預期。

不過,雲業務的增長不如預期強勁,但它對微軟的重要性正在明顯增加。在電話會上納德拉表示,微軟雲的年收入超過了 1100 億美元,其中 Azure 的收入首次佔總收入的 50% 以上。

在營收之外,大家尤其關注的還有微軟本季度由 AI 引起支出是否在大幅增加。事實也確實如此,微軟上一季度的支出為 89.4 億美元,高於市場預期的 78.5 億美元。在電話會上微軟表示,公司預計 2024 資本開支將在 2024 財年逐個季度增長,主要將用於數據中心、CPU 芯片、GPU 芯片和網絡設備方面,也和谷歌一樣釋放出出將持續加大 AI 投資的信號。

受到微軟雲業務增速放緩和低業績預期的影響,微軟股價在盤後一度跌超 3%。

雖然 AI 的投入還並沒有體現在本季度的業績之中,納德拉也明確表示將繼續加大 AI 投資戰略。他表示,微軟仍然專注於引領新的人工智能平台轉變,講幫助客户使用微軟雲從他們的數字支出中獲得最大價值,並提高運營槓桿。

總體來看,雖然上個季度是生成式 AI 的高潮期,但 AI 目前並沒有給谷歌、微軟帶來預期的回報。但從兩家公司的表態來看,加大 AI 投資的路線並不會改變。

可能真正的 AI 之戰還尚未拉開帷幕。

本文作者:Juny,來源:硅星人,原文標題:《微軟谷歌同時交作業,谷歌絕地反擊 “贏麻” 了》