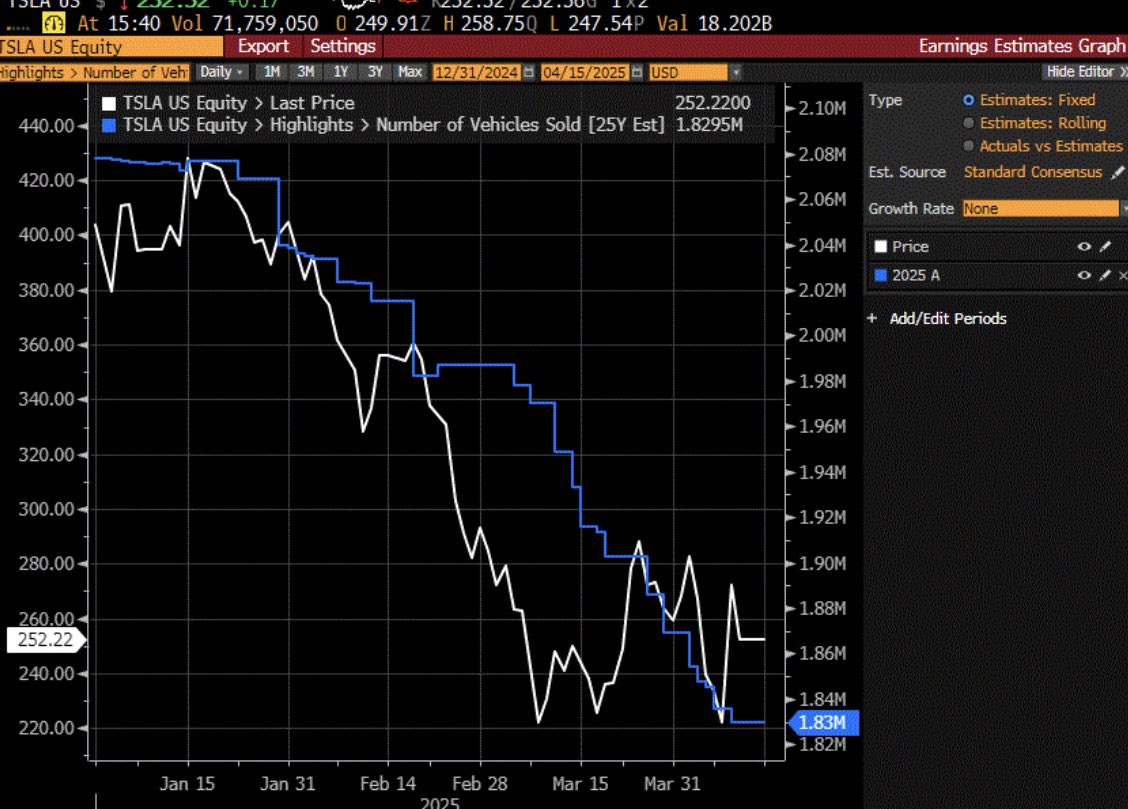

$Tesla(TSLA.US) WS 2Q ests are now below 2024/2Q ests (439K -1.2% YoY) but WS FY’25 ests still seem way too high (WS FY’25 1,829K +2.2% YoY), given the TSLA brand taint, lower odds the more affordable vehicle to be launched in 3Q will be a new form factor that expands TAM, and increased odds of recession caused by the tariffs uncertainty. My FY’25 TSLA delivs est is now 1,720K (-4% YoY) and my FY’25 Adj EPS is now $2.60 (vs WS $2.66).

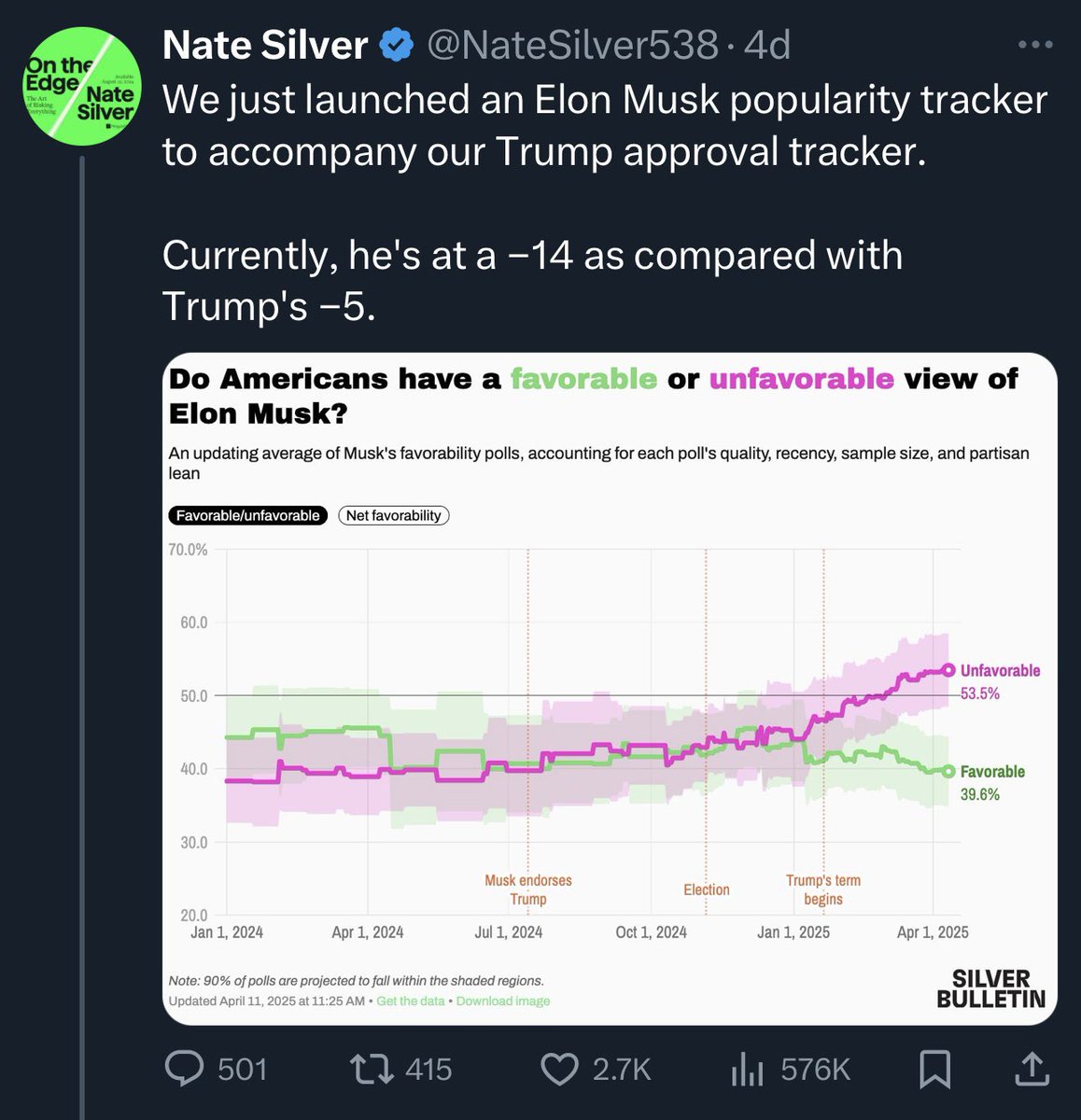

We doubt we will get much clarity on FY’25 deliveries and the more affordable model on next week’s TSLA earnings call, but we think odds favor the stock going lower after the call, given the normal WS cadence to wait until after earnings to update models, even after TSLA’s big 1Q delivs miss (337K vs 377K consensus). The Atlanta Fed GDP Now tracker now ests 1Q GDP growth at -2.4%. We note that Elon’s net favorability rating is now -14pp (from zero at the beginning of the year), while Trump’s unfavorably rating has ballooned to -8.5pp (from +12 at the beginning of 2025) as a result of his proposed record tariffs.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.