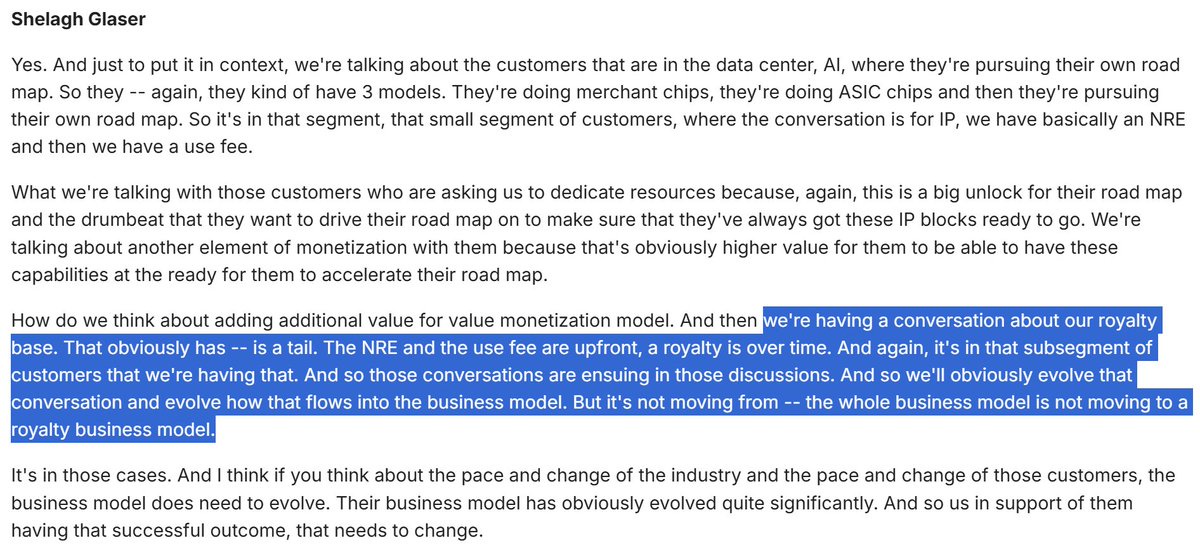

Synopsys' IP business in a challenging period currently. 25% of revenue and declined 8% in FY25 and FY26 will be muted as well. In a shift to its IP business model, SNPS is planning to charge royalties on custom chips of hyperscalers (been communicating this for some time) and seemed to have firmed up this plan. Also, SNPS is not assuming lost Intel Foundry 18A revenue not coming back in FY26 (ends in Oct '26). However, Intel could become a tailwind in FY27 with 18A-P. Earlier, SNPS predicted its IP business will return to long-term revenue CAGR (mid-teens) post-FY26.

Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.