Intel 4Q25

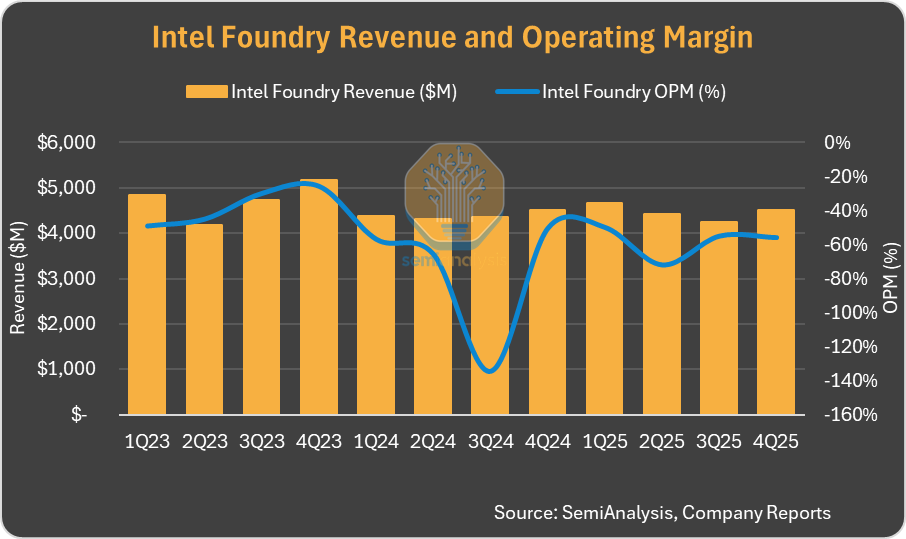

+ve: Demand outstripping supply, PL momentum, 18AP PDK 1.0 in customers' hands, 14A 0.5 PDK test chips ongoing, ASIC traction ($1B run-rate) and advanced packaging momentum, spending on Intel7/3/18A capacity expansion in '26 (good news for semicaps), yields alone could add much capacity without capex-ve: supply tightness could cap rev; low yields, market share risk in PC and DC and 14A customer commitment (yet to come)Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments