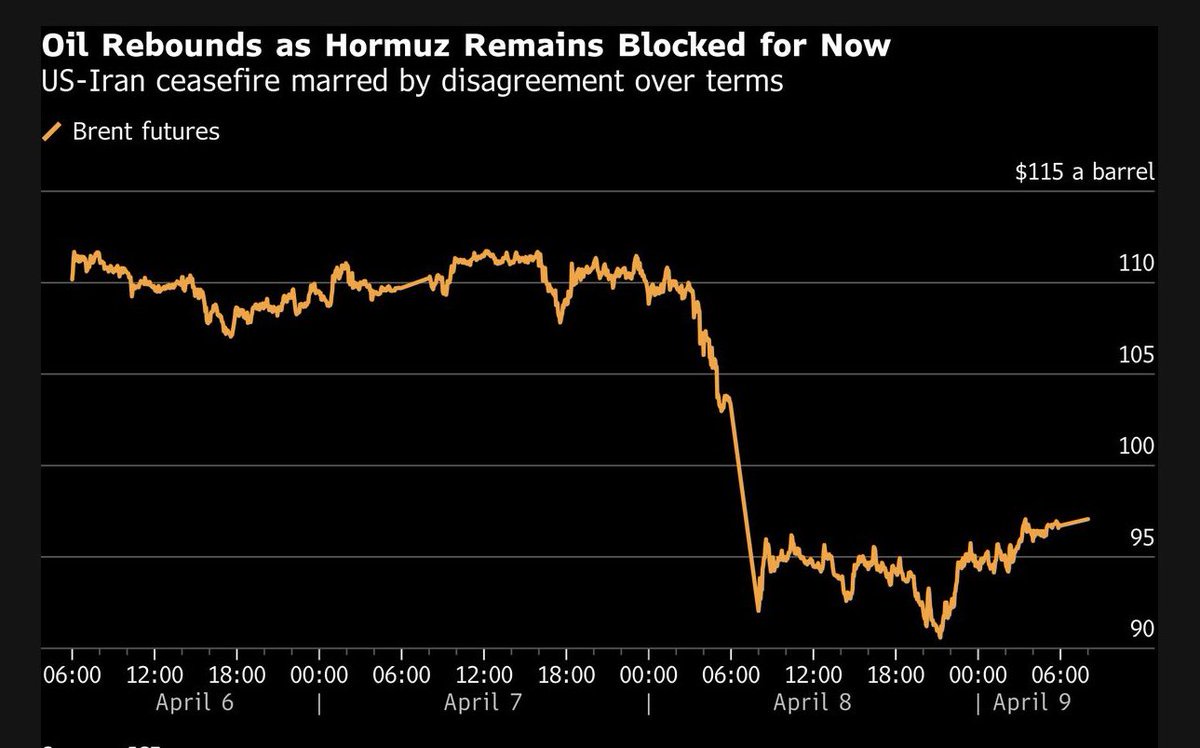

Highlights from today’s pre-mkt summary for Subscribers: Stocks fell modestly in pre-market trading while oil surged +4% to $98/barrel after a -13% drop Wednesday, as optimism faded over the fragile US-Iran ceasefire. Iran cited Israel’s ongoing attacks on Hezbollah targets in Lebanon as a breach, with the Strait of Hormuz remaining effectively closed and no tankers crossing since the truce began. Diplomatic talks are set for Saturday in Islamabad, Pakistan led by VP Vance. Gold and silver were essentially unchanged and Bitcoin edged lower. 10-year treasury yields dipped 1bp to 4.28%. February PCE inflation data is due Friday.

FOMC minutes revealed growing Fed concerns that the Iran conflict could stoke inflation, potentially requiring rate hikes. We continue to expect equities to reclaim new highs once the Middle East conflict resolves, oil retreats, and employment slows, paving the way for faster Fed cuts. 2026 S&P EPS estimates have risen to $323 (+17% YoY), implying a 21.0x P/E and 4.8% earnings yield, in line with the historic premiums vs 10-year treasury yields. We remain cautious on TSLA due to declining long-term earnings estimates, rising competition in unsupervised autonomy (from GOOG, AMZN, etc.), and potential selling pressure from a SpaceX IPO. No position in TSLA given its stretched valuation (2026 P/E 180x vs +35% long-term EPS growth ~5x PEG).

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.