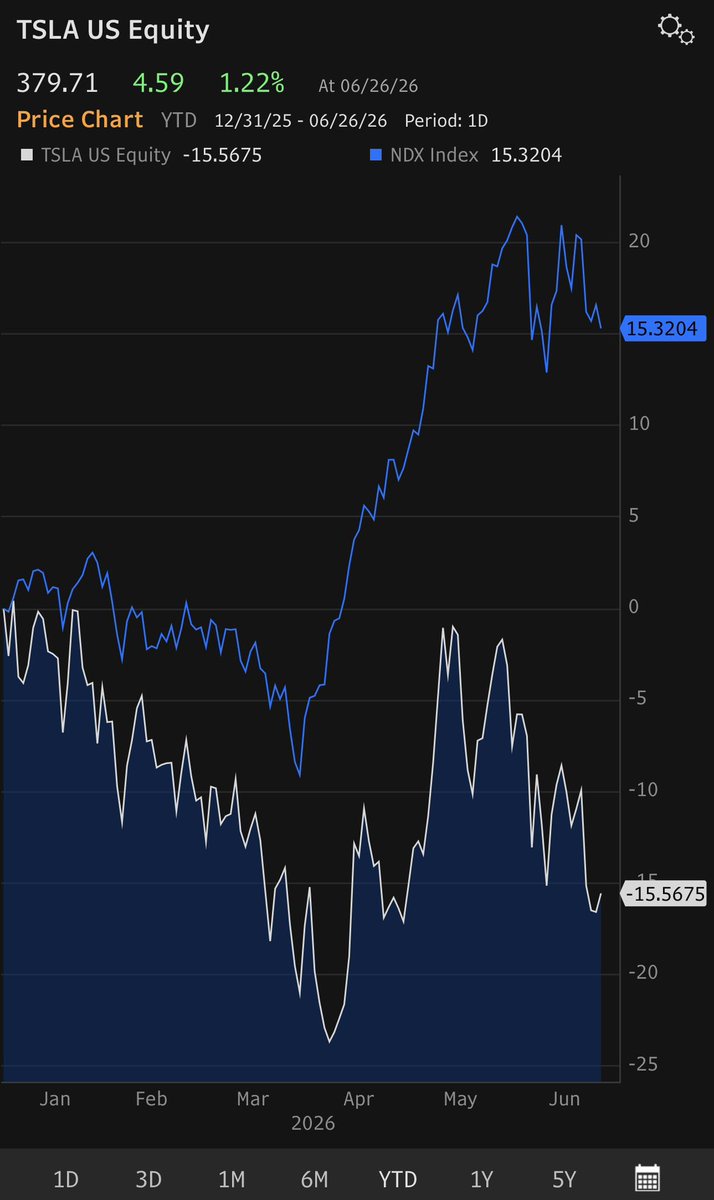

$Tesla(TSLA.US) -15% year-to-date (vs NDX +16%) as TSLA’s rollout of unsupervised autonomous driving continues to sputter. TSLA bull Dan Ives continues to predict that TSLA is on its way to $600 with numerous catalysts. We remain skeptical with TSLA’s unsupervised autonomy fleet (no safety monitors) seemingly stalled at around 40 vehicles until efficacy improves. Many TSLA bulls erroneously count supervised autonomous vehicles (which employ safety monitors in the front seat) in their TSLA fleet numbers which is misleading.

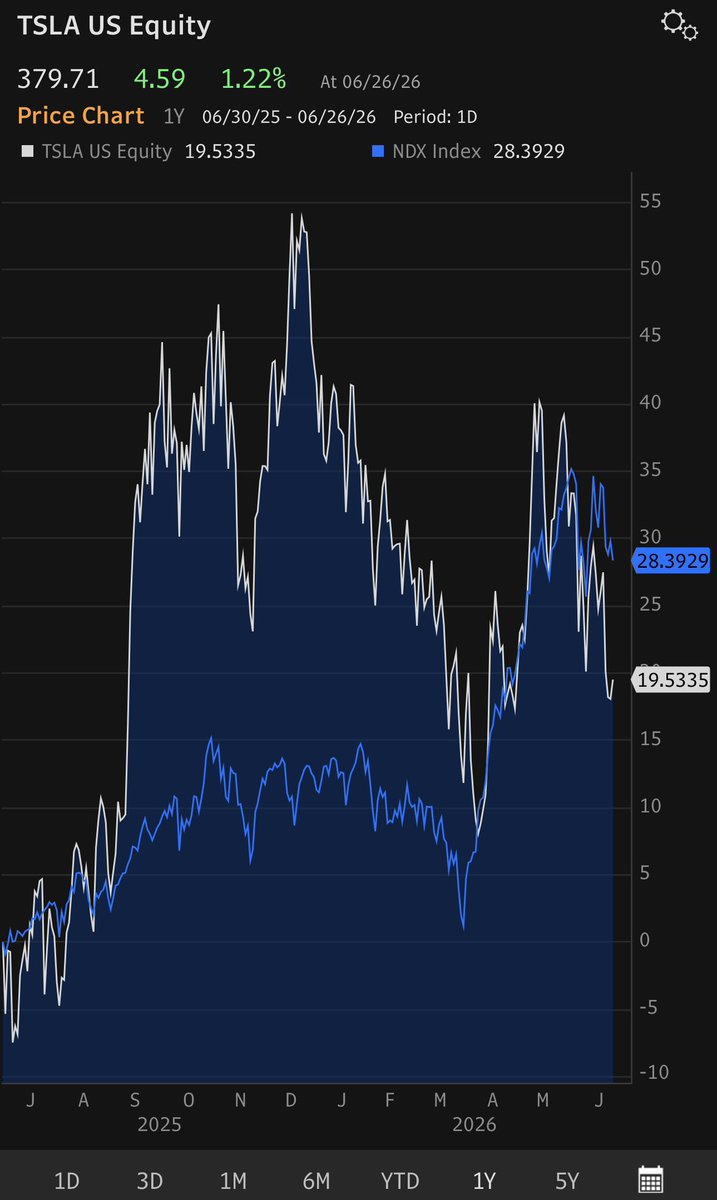

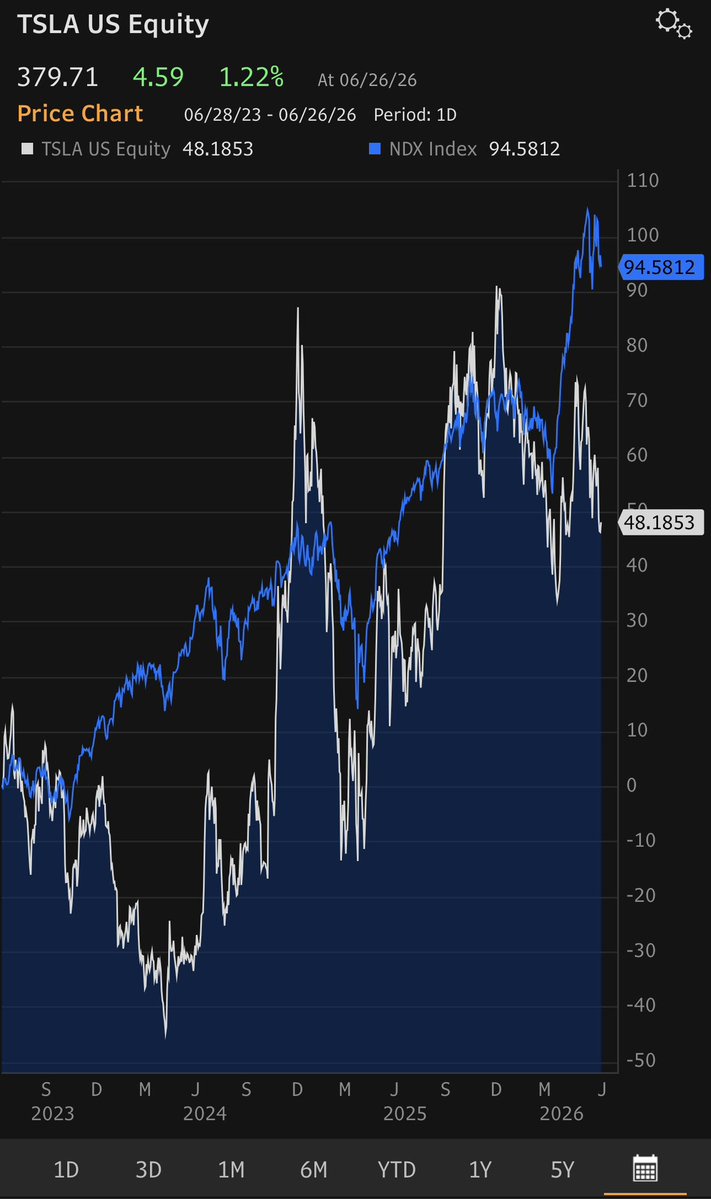

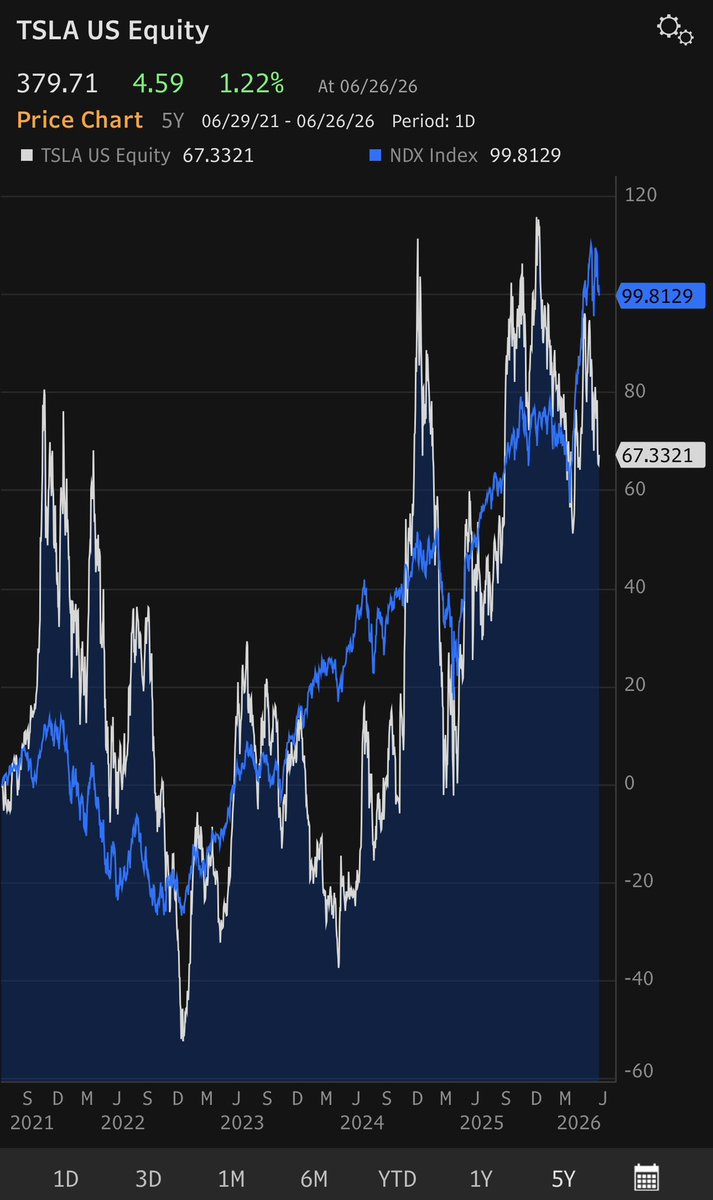

Earlier this month, the tragic accident outside Houston where a driver who said FSD was engaged plowed into a house killing the owner inside, combined with the absence of TSLA PR unleased a torrid of negative media headlines. We continue to battle with TSLA bulls on the shortsightedness of not investing in PR even as TSLA management accused the media of lying. This is akin to a dad blaming the school if his son didn’t make the football team even though his kid didn’t bother to try out. We expect TSLA to continue to underperform (1yr TSLA +19% vs NDX +28%, 3yr TSLA +48% vs NDX +95%, 5yr TSLA +67% vs NDX +99%) until TSLA can scale up its unsupervised autonomous fleet (no safety monitors) from the current 40 vehicles to areas representing 50% of the U.S. population as targeted by Elon Musk on July 23 2025 during Tesla’s Q2 2025 earnings call: (“I think we’ll probably have autonomous rides -hailing in probably half the population of the U.S. by the end of the year [2025]).” I expect TSLA to continue to underperform NDX until unsupervised autonomy scales. I don’t see that happening until FSD efficacy reaches 99.99% (1 intervention every 10,000 drives). Today TSLA FSD efficacy is probably 99% (1 intervention every 100 drives). TSLA bulls also seem to be latching onto the silly idea that $SpaceX(SPCX.US) with a market cap of $2 trillion will somehow use its expensive stock to buy TSLA with its $1.4 trillion market cap, despite potential massive dilution (we est ~25% dilution at existing market caps and multiples) and obvious governance questions.In 2Q we expect TSLA and other EV makers to benefit from stubbornly high gas prices which should boost EV deliveries. On Friday, TSLA IR posted its 2Q consensus delivery estimates which show a 2Q delivery gain of +6% YoY and FY 26 delivery gain of +1% YoY, which suggests TSLA deliveries could avoid a third consecutive year of decline. While bulls argue that TSLA is not just a car company, EVs still make up 72% of TSLA gross profits and it’s difficult to expect investors to accord a 200x P/E to a stock with earnings that are shrinking and its unsupervised autonomy rollout stalled.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.