$Kimly(1D0.SG)

High Yield & Strong Cash Flow — What’s The Catch?🤔

Looking for a reliable dividend stock? Most Singaporean investors know this household name. A very familiar brand in heartland neighborhoods. Let us break down Kimly Limited (SGX: 1D0) using its latest FY2025 financials to see if it fits your portfolio.

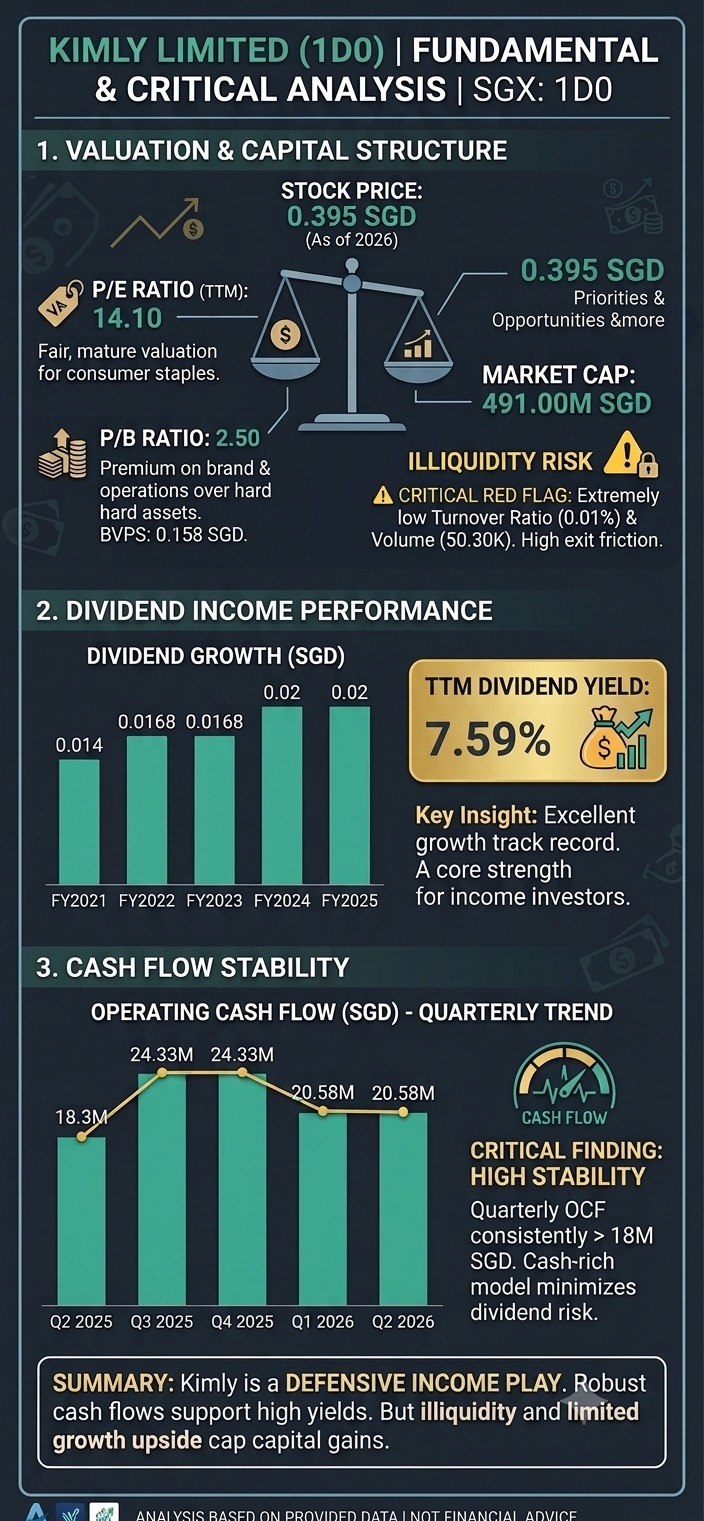

1️⃣Valuation & Liquidity

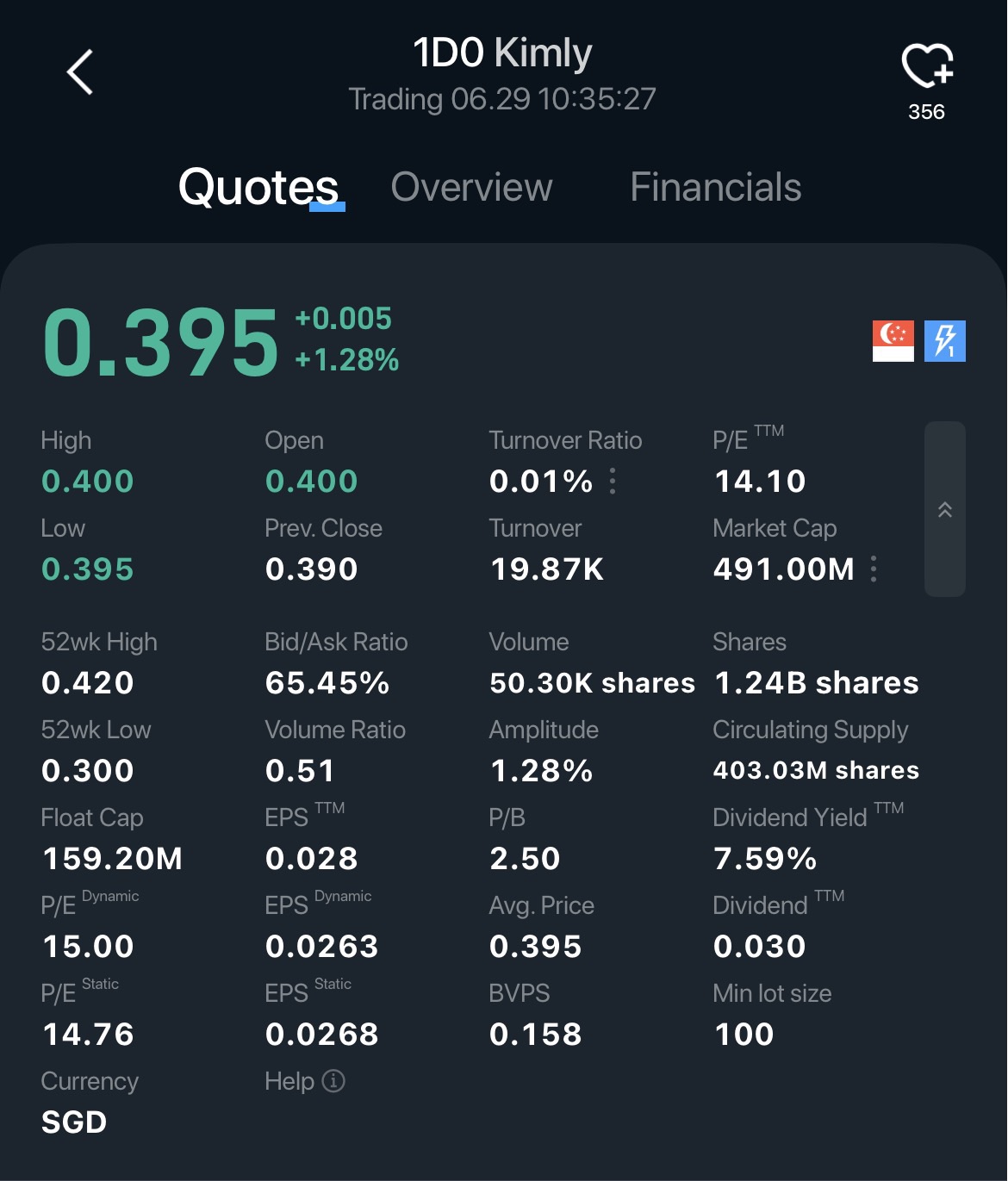

🟢 Fair valuation: Trading at trailing P/E ~14.1x, P/B ~2.5x — reasonable for a stable local F&B/coffee‑shop operator

⚠️ Key risk: Very low liquidity — turnover ratio ~0.01–0.04%, daily volume ~50K–180K shares. Exiting large positions may be difficult

2️⃣ Dividend Track Record

🟢 Steady growth: DPS rose from S$0.014 (FY2021) to S$0.020 (FY2025)

🟢 Current yield: ~4.7–5.0% (TTM)

3️⃣Cash Flow & Balance Sheet

🟢 Strong cash generation: Quarterly operating cash flow consistently above S$18M, peaking at ~S$24.3M; FY2025 OCF ~S$85.3M

🟢 Net cash position: ~S$63M, minimal debt (~S$5M) — fully covers CAPEX and dividends

🟢 Defensive model: Recurring rental + food retail income = stable payouts

🔷The Verdict

Kimly is a classic defensive income stock. Its robust cash flow and healthy balance sheet support consistent dividends.

However, its low liquidity and Singapore only focus mean it is ideal for passive income not quick capital gains.

Not financial advice. Do your DD.😉

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.