Mizuho Securities: CPUs & GPUs

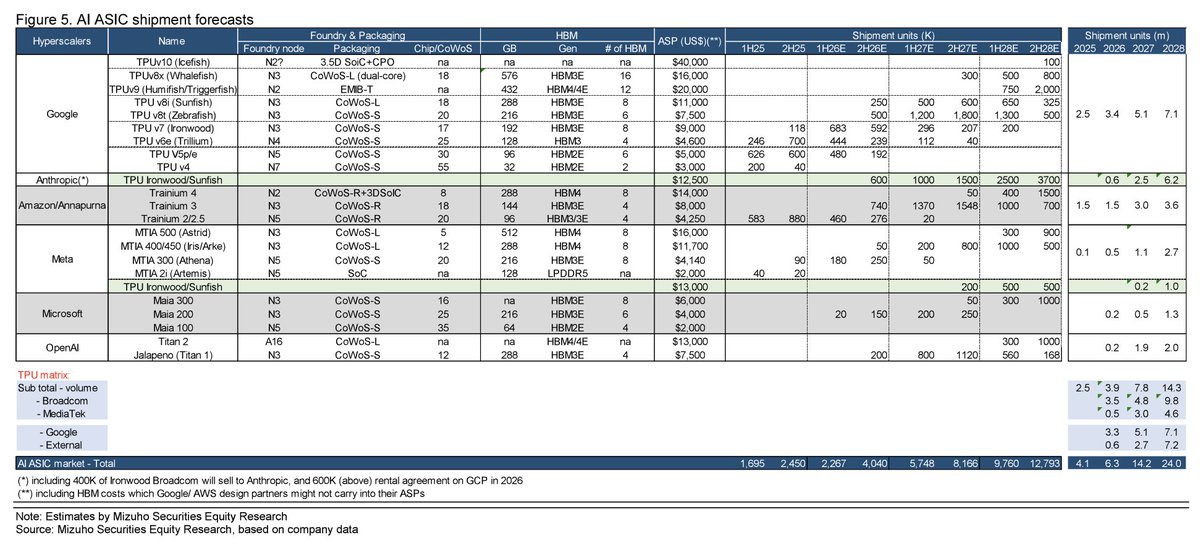

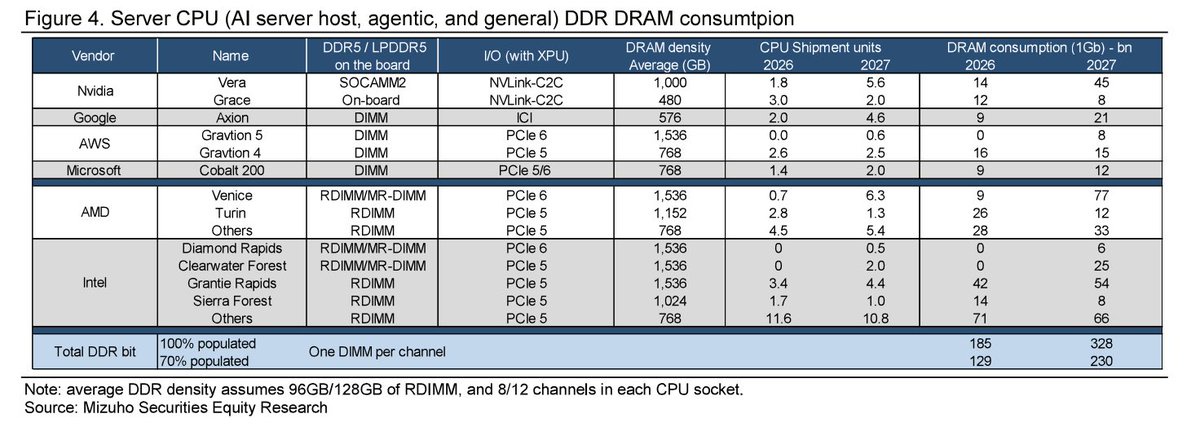

Market Forecasts & Growth> Shipment Growth: Industry server CPU shipments are forecasted to reach 35 million units in 2026 and grow to 50 million units by 2027, representing a 40% year-over-year increase. > Long-Term TAM: The long-term Total Addressable Market (TAM) estimate for 2030 has been raised to $170 billion (up from the previous $107 billion forecast), driven by higher CPU-to-GPU ratio assumptions for AI inference servers. > CPU-to-GPU Ratios: The CPU-to-GPU ratio on AI servers is accelerating and is expected to approach 1:1 by the end of 2027 or 2028.Supply Chain & Technical Bottlenecks> DRAM Constraints: A critical bottleneck exists in DDR5/LPDDR5 supply, with a projected fulfillment ratio of only 70% over the next 12–18 months. > Demand vs. Supply Gap: Based on current models, the 2027 demand for DDR5/LPDDR5X (over 300 billion 1Gb equivalents) significantly exceeds the projected supply (220–250 billion 1Gb equivalents). > Potential Risks: The shortage of key materials—DRAM, substrates, and passives—is expected to persist through 2027 and could pose downside risks to downstream server assemblers, potentially leading to lower server rack output. Key Player Insights (2027 Forecasts)> Nvidia: Expected to reach 5.0–6.0 million units for the Vera CPU, including 2.0–3.0 million units specifically for agentic AI stack racks. > Google: Axion CPU production is projected to increase more than 2x year-over-year, aligning with the growth trajectory of TPU units. > AMD: The N2 Venice CPU is forecasted to exceed 6.0 million units.GPUs/ASICsMarket Growth Projections> Rapid Expansion: The total AI ASIC market is projected to grow from 4.1 million units in 2025 to 24.0 million units by 2028. > Volume Drivers: The growth is driven by substantial increases in deployment by major hyperscalers including Google, Amazon (Annapurna), Meta, Microsoft, and OpenAI. > External Demand: The market for external (non-Google) AI ASIC units is expected to surge from 0.6 million in 2025 to 7.2 million by 2028. Key Hyperscaler Activity> Google (TPU): Continues to be a dominant player, with total shipment units increasing from 2.5 million in 2025 to 7.1 million by 2028. > Anthropic: Significant ramp-up is forecasted for their "TPU Ironwood/Sunfish" chips, moving from 0.6 million units in 2026 to 6.2 million units by 2028. > Amazon/Annapurna: Shipments for the Trainium line are projected to double from 1.5 million in 2025 to 3.6 million by 2028. > Meta: Rapid scaling of MTIA chips is expected, growing from 0.1 million units in 2025 to 2.7 million units by 2028. Technical Trends> Advanced Packaging & Nodes: There is a heavy reliance on sophisticated packaging technologies like CoWoS-L and CoWoS-S, and advanced foundry nodes including N2, N3, N4, N5, and A16. > HBM Integration: Nearly all listed high-performance ASICs utilize High Bandwidth Memory (HBM), with a transition toward newer generations such as HBM3E and HBM4/4E to meet performance demands. > ASP Variance: Average Selling Prices (ASP) range significantly, from approximately $2,000 for entry-level models to as high as $40,000 for top-tier specialized chips like the TPUv10.$DRAM $EWY $Micron Tech(MU.US) $Alphabet(GOOGL.US) $Amkor Tech(AMKR.US) $Taiwan Semiconductor(TSM.US) $ASE $NVIDIA(NVDA.US) $AMD(AMD.US) $Broadcom(AVGO.US) $Marvell Tech(MRVL.US) $Intel(INTC.US) $Microsoft(MSFT.US) $Meta Platforms(META.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments