Mizuho Securities: Optics

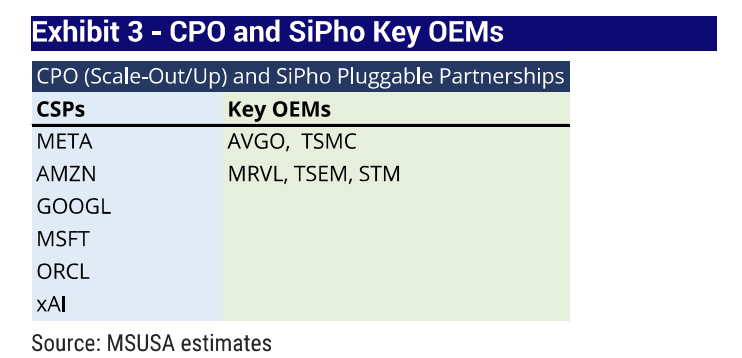

Market Trends & Technologies> Optical Circuit Switches (OCS): OCS is gaining traction among hyperscalers, with Google (GOOGL) leading adoption in its Jupiter Network and other hyperscalers like Amazon (AMZN) and Microsoft (MSFT) exploring its use. Lumentum (LITE) and Huber+Suhner (HUBN) are identified as key partners in this space. > Co-Packaged Optics (CPO) vs. Near-Packaged Optics (NPO): While interest in CPO continues to grow (with potential deliveries in 2028/29E), industry focus is shifting toward NPO in the near-term because it is easier to deploy and requires less co-integration than CPO, despite being less power-efficient. > Silicon Photonics (SiPho) & InP: The supply chain for SiPho remains constrained, with demand potentially outpacing foundry capacities at GFS and TSEM. A transition to 6-inch wafers is underway to help alleviate supply tightness by providing ~130% higher wafer area. > Micro-LED (uLED) Potential: uLED/ALC is emerging as a potential disruptor for networking, offering 20-30m reach at approximately 1/5th the cost of optical pluggables, with no InP supply constraints. Credo (CRDO) is noted as a key player in this space, targeting deliveries starting in 2027-28E. Company-Specific Updates (Lumentum & Credo)Lumentum (LITE):> Growth Drivers: Lumentum management noted that the "best is yet to come" as several major growth drivers—optical scale-up, optical scale-out, and optical circuit switches (OCS)—are just beginning to ramp up and are not yet fully reflected in their numbers.> 1.6T Transition: The company is seeing a significant tailwind from the transition to 1.6T transceivers, led by NVIDIA and Google, with 200-gig EMLs providing roughly double the average selling price (ASP) of previous generations.> Scale-Out Business: The partnership with NVIDIA for high-powered lasers in CPO switch platforms is a major focus, with expected incremental revenue of $50 million to $100 million in the fourth quarter of fiscal 2026 alone.Credo Technology (CRDO):> Market Outperformance: Credo has significantly outperformed larger rivals like NVIDIA and Broadcom in share price gains during 2026, largely due to its specialized role in high-speed, energy-efficient connectivity.> Optical Portfolio: Following its acquisition of DustPhotonics, Credo has strengthened its silicon photonics capabilities. The company expects its optical connectivity business to generate over $600 million in revenue in fiscal 2027, supported by a 1.6T networking transition.$Lumentum(LITE.US) $Credo Tech(CRDO.US) $Broadcom(AVGO.US) $NVIDIA(NVDA.US) $STMicroelectronics NV(STM.US) $Alphabet(GOOGL.US) $Meta Platforms(META.US) $Tower Semicon(TSEM.US) $Marvell Tech(MRVL.US) $Taiwan Semiconductor(TSM.US) $Microsoft(MSFT.US) $Amazon(AMZN.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments