A discussion on investment perspectives:

On X, I saw the following perspective:

I asked GPT to analyze and evaluate this perspective. The reason is that I have been looking at investment opportunities in the U.S. power market but have yet to make a decision. This is a long-term investment path. I also carefully read this:

Systematic Evaluation of the Perspective

| Dimension | Supporting Arguments | Key Risks | Overall Judgment |

|---|---|---|---|

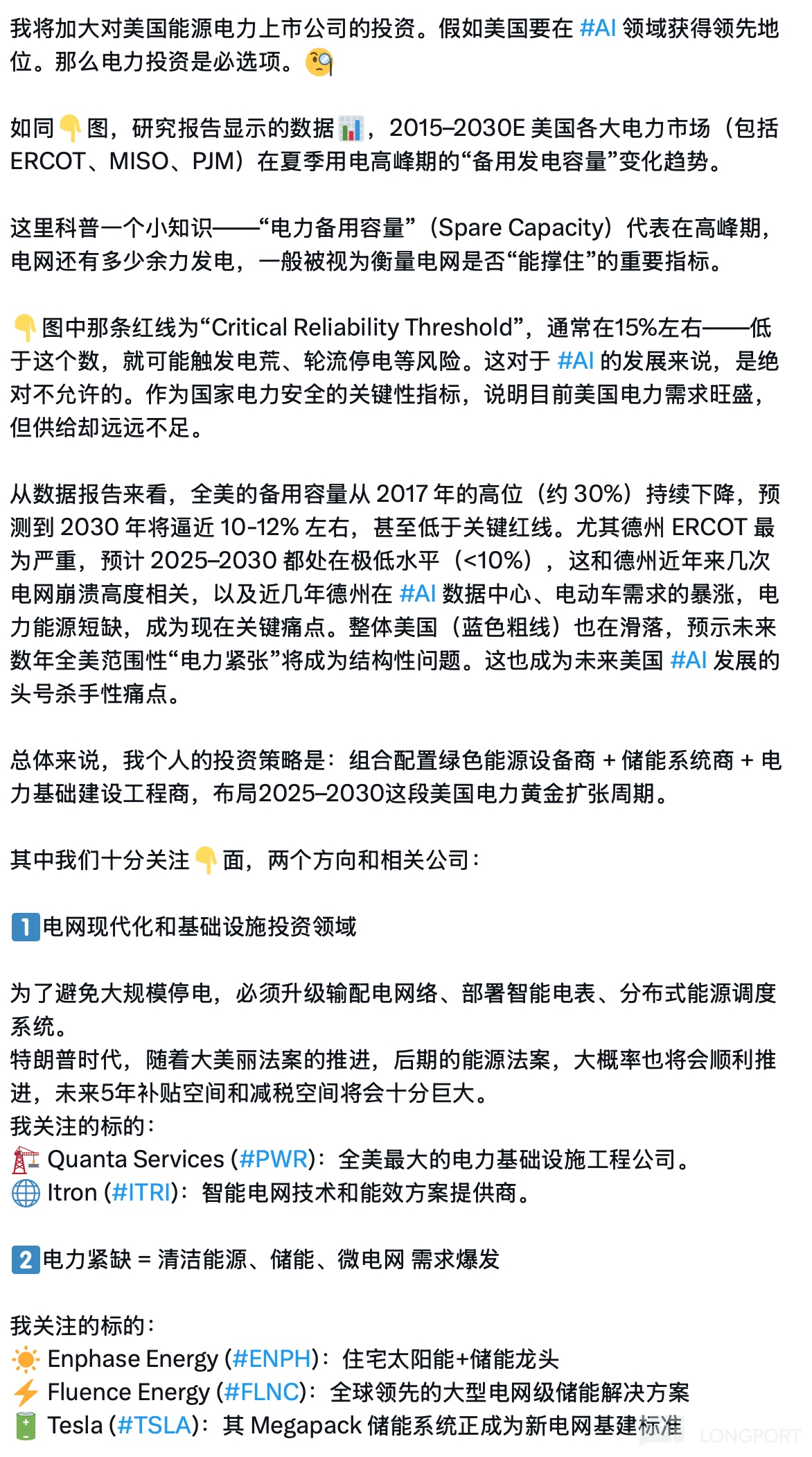

| Power Shortage and AI Electricity Demand | • DOE estimates data centers will consume 6.7–12% of U.S. electricity by 2028 (2023: 4.4%) (reuters.com) • Under PJM's "low new-build" scenario, reserve margins will drop from 23% in 2023 to 5–8% by 2030 (utilitydive.com) • ERCOT's latest CDR report shows summer reserve margins may only reach 10–12% by 2030 (below the 13.75% reliability threshold) (ercot.com) | • Model assumptions vary widely; if energy storage/demand response accelerates, the gap could be partially mitigated • Data center locations may shift to low-electricity-cost states, easing local tensions | Supply-demand gaps are highly likely, but regional differences require careful market selection |

| Policy and Capital Expenditure | • EEI estimates U.S. grid upgrades will cost up to $1.5 trillion by 2030 (ainvest.com) • Federal IIJA, IRA, and the anticipated "Energy Independence Act" provide tax credits and loan guarantees | • Post-election policy continuity is uncertain; local environmental reviews and grid connection approvals often face delays | Strong subsidy-driven growth, but project timelines may be volatile |

| Company Fundamentals | PWR: Q1 2025 revenue +24%, raised full-year guidance (prnewswire.com, ainvest.com) ITRI: AMI (smart meters) continue to win bids in ERCOT and PJM; ENPH / FLNC / TSLA Megapack: Strong order books, margins above industry average | • High-interest cycles pressure valuations; • Energy storage margins fluctuate with lithium prices; • TSLA, ENPH valuations already price in high growth | High-quality assets, but dynamic valuation and interest rate sensitivity must be assessed |

Investment Recommendations

1 | Select Sectors Strategically: "Generation—Grid—Storage" Three-Tier Allocation

| Tier | Key Segments & Stocks | Metrics to Watch | Suggested Allocation Weight * |

|---|---|---|---|

| Generation & Capacity Markets | Controllable/dispatchable natural gas & nuclear utilities (EXC, NEE), data center PPA developers | Capacity Payments, ROE | 30% |

| Grid Upgrades | PWR, MYR, ITRI (AMI) | Backlog/Gross Margin, Regulated Rate | 40% |

| Storage & Distributed Energy | ENPH, FLNC, TSLA Megapack, STEM | ASP, Order Cycle, Raw Material Hedging | 30% |

* Adjusted for thematic ETF weights; fine-tune based on risk tolerance.

2 | Prioritize ERCOT + PJM High-Demand Stocks

These regions face the clearest power shortages and highest data center concentration;

Regulatory mechanisms (capacity markets/scarcity pricing) offer higher marginal returns for generation and storage.

3 | Mitigate Three Key Risks

Interest Rates & Valuation Compression: Hedge against tail risks with utility bonds or convertibles.

Price Suppression Policies: Local freezes on electricity rates or solar buyback limits may pressure profits.

Supply Chains: Energy storage delivery hinges on battery cells and inverters; monitor FLNC/TSLA's LFP/NMC supply contracts.

Execution

| Action | Details |

|---|---|

| Entry Timing | Deploy initial capital in 2024 Q4–2025 H1, add on policy/grid approval tailwinds; increase leverage after Fed's first rate cut. |

| Valuation Anchors | Utilities: P/E & P/B (buy at <70% historical percentile); Engineering/equipment: EV/EBITDA (PWR☑ ≈11–12x is reasonable). |

| Exit Signals | Reserve margins rebound >18%, or load forecasts decline >5% for two consecutive quarters; or Fed Funds > prior peak for 2+ quarters. |

Conclusion

The "bottleneck conflict" between AI and electricity makes 2025–2030 a high-growth cycle for U.S. grid upgrades and energy storage.

A three-tier "generation—grid—storage" portfolio, focused on ERCOT/PJM high-shortage zones with dynamic interest rate and policy risk management, can deliver alpha. True alpha lies in:Securing EPC + O&M-integrated leaders early (e.g., PWR);

Capturing the 2026–2027 storage project acceleration window;

Tracking subsidy policies and capacity market reforms in real-time for timely adjustments.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.